Free PDF Download of CBSE Accountancy Multiple Choice Questions for Class 12 with Answers Chapter 7 Issue of Shares. Accountancy MCQs for Class 12 Chapter Wise with Answers PDF Download was Prepared Based on Latest Exam Pattern. Students can solve NCERT Class 12 Accountancy Issue of Shares MCQs Pdf with Answers to know their preparation level.

Issue of Shares Class 12 Accountancy MCQs Pdf

Select the Best Alternate and tally your answer with the Answers given at the end of the book :

(i) Meaning and Characteristics of a Company

1. A company has ……………

(A) Separate Legal Entity

(B) Perpetual Existence

(C) Limited Liability

(D) All of the Above

Answer

Answer: D

2. Shareholders are :

(A) Customers of the Company

(B) Owners of the Company

(C) Creditors of the Company

(D) None of these

Answer

Answer: B

3. Who are the real owners of a company?

(A) Government

(B) Board of Directors

(C) Equity shareholders

(D) Debentureholders

Answer

Answer: C

4. A Company is created by :

(A) Special act of the Parliament

(B) Companies Act

(C) Investors

(D) Members

Answer

Answer: B

5. An artificial person created by Law is called :

(A) Sole Tradership

(B) Partnership Firm

(C) Company

(D) All of the Above

Answer

Answer: C

6. The liability of members in a Company is :

(A) Limited

(B) Unlimited

(C) Stable

(D) Fluctuating

Answer

Answer: A

7. Liability of a shareholder is limited to ………………… of the shares allotted to him :

(A) Paid up Value

(B) Called up value

(C) Face value

(D) Reserve Price

Answer

Answer: C

8. Maximum number of members in a private company is :

(A) 7

(B) 200

(C) 20

(D) No Limit

Answer

Answer: B

(ii) Meaning, Nature and Types of Shares

9. Capital of a Company is divided in units which is called :

(A) Debenture

(B) Share

(C) Stock

(D) Bond

Answer

Answer: B

10. Shareholders receive from the company :

(A) Interest

(B) Commission

(C) Profit

(D) Dividend

Answer

Answer: D

11. Equity shares cannot be issued for the purpose of:

(A) Cash Receipts

(B) Purchase of assets

(C) Redemption of debentures

(D) Distribution of dividend

Answer

Answer: D

12. A Company may issue ……………….

(A) Equity Shares

(B) Preference Shares

(C) Equity and Preference both shares

(D) None of the Above

Answer

Answer: C

13. A company cannot issue :

(A) Redeemable Equity Shares

(B) Redeemable Preference Shares

(C) Redeemable Debentures

(D) Fully Convertible Debentures

Answer

Answer: A

14. To whom dividend is given at a fixed rate in a company?

(A) To equity shareholders

(B) To preference shareholders

(C) To debenture holders

(D) To promoters

Answer

Answer: B

15. Preference shareholders have

(A) Preferential right as to dividend only

(B) Preferential right in the management

(C) Preferential right as to repayment of capital at the time of liquidation of the company

(D) Preferential right as to dividend and repayment of capital at the time of liquidation of the Company

Answer

Answer: D

16. The shares on which there is no any pre-fixed rate of dividend is decided, but the rate of dividend is fluctuating every year according to the availability of profits, such share are called :

(A) Equity Share

(B) Non-cumulative preference share

(C) Non-convertible preference share

(D) Non-guaranteed preference share

Answer

Answer: A

17. Preference shares, in case the holders of these have a right to convert their preference shares into equity shares at their option according to the terms of issue, such shares are called :

(A) Cumulative Preference Share

(B) Non-cumulative Preference Share

(C) Convertible Preference Share

(D) Non-convertible Preference Share

Answer

Answer: C

18. A preference share which does not carry the right of sharing in surplus profits is called ……………

(A) Non-Cumulative Preference Share

(B) Non-participating Preference Share

(C) Irredeemable Preference Share

(D) Non-convertible Preference Share

Answer

Answer: B

19. Which shareholders have a right to receive the arrears of dividend from future profits :

(A) Redeemable Preference Shares

(B) Participating Preference Shares

(C) Cumulative Preference Shares

(D) Non-Cumulative Preference Shares

Answer

Answer: C

20. Which shareholders are returned their capital after some specified time :

(A) Redeemable Preference Shares

(B) Irredeemable Preference Shares

(C) Cumulative Preference Shares

(D) Participating Preference Shares

Answer

Answer: A

21. The following statements apply to equity/preference shareholders. Which one of them applies only to preference shareholders?

(A) Shareholders risk the loss of investment

(B) Shareholders bear the risk of no dividends in the event of losses

(C) Shareholders usually have the right to vote

(D) Dividends are usually given at a set amount in every’ financial year.

Answer

Answer: D

22. Unless otherwise stated, a preference share is always deemed to be :

(A) Cumulative, participating and non-convertible

(B) Non-cumulative, non-participating and non-convertible

(C) Cumulative, non-participating and non-convertible

(D) Non-cumulative, participating and non-convertible

Answer

Answer: C

(iii) Meaning, Nature and Types of Share Capital

23. Nominal Share Capital is

(A) that part of authorised capital which is issued by the company

(B) the amount of capital which is actually applied by the prospective shareholders

(C) the amount of capital which is actually paid by the shareholders

(D) the maximum amount of share capital which a company is authorised to issue

Answer

Answer: D

24. The portion of the capital which can be called-up only on the winding up of the Company is called (CPT Dec. 2012)

(A) Authorised Capital

(B) Called up Capital

(C) Uncalled Capital

(D) Reserve Capital

Answer

Answer: D

25. Capital included in the Total of Balance Sheet of a Company is called :

(A) Issued Capital

(B) Subscribed Capital

(C) Called up Capital

(D) Authorised Capital

Answer

Answer: B

26 is transferred to Capital Reserve.

(A) Profit from sale of fixed assets

(B) Premium on issue of shares

(C) Profit on forfeiture of shares

(D) All of the Above

Answer

Answer: D

27. Reserve Capital is also known by :

(A) Capital Reserve

(B) Called up Capital

(C) Subscribed Capital

(D) None of the above

Answer

Answer: D

28. Reserve Capital is :

(A) Subscribed Capital

(B) Capital Reserve

(C) Uncalled Capital

(D) Part of the uncalled capital which may be called only at the time of liquidation of the Company

Answer

Answer: D

29. In the Balance Sheet of a company, under the heading share capital, at the last is shown :

(A) Authorised Share Capital

(B) Subscribed Share Capital

(C) Issued Share Capital

(D) Reserve Share Capital

Answer

Answer: B

30. Which of the following is not shown under the heading ‘Share Capital’ in a Balance Sheet:

(A) Subscribed Capital

(B) Issued Capital

(C) Reserve Capital

(D) Authorised Capital

Answer

Answer: C

31. Reserve Capital is a part of:

(A) Paid-up Capital

(B) Forfeited Share Capital

(C) Assets

(D) Capital to be called up only on liquidation of company

Answer

Answer: D

32. Which of the following statements is true? (C.S. Foundation, Dec. 2012)

(A) Authorised Capital = Issued Capital

(B) Authorised Capital > Issued Capital

(C) Paid up Capital > Issued Capital

(D) None of the above

Answer

Answer: B

33. Authorised Capital of a Company is mentioned in :

(A) Memorandum of Association

(B) Articles of Association

(C) Prospectus

(D) Statement in lieu of Prospectus

Answer

Answer: A

34. In case of private placement of shares, the lock in period is :

(A) 1 Year

(B) 2 Years

(C) 3 Years

(D) None of the above

Answer

Answer: C

35. In case of private placement of shares and company does not invite the general public for subscription of shares in that case, company instead of issuing prospectus :

(A) Prepares the statement in lieu of prospectus

(B) Prepares the Report

(C) Prepares the Budget

(D) Prepares the Asset side of Balance Sheet

Answer

Answer: A

36. In case of private placement of shares, to raise the amount of capital a company :

(A) invites the public through prospectus

(B) does not invite the public

(C) invites the public through advertisement

(D) invites the public through memorandum of association

Answer

Answer: B

37. Shares issued by a company to its employees or directors in consideration of ‘Intellectual Property Rights’ are called :

(A) Right Equity Shares

(B) Private Equity Shares

(C) Sweat Equity Shares

(D) Bonus Equity Shares

Answer

Answer: C

(iv) Issue and Allotment of Shares

38. A Company may issue the shares :

(A) By Private Placement of Shares

(B) By Public Subscription of Shares

(C) For Consideration other than cash

(D) By All of the Above

Answer

Answer: D

39. Public subscription of shares include :

(A) To Issue Prospectus

(B) To Receive Applications

(C) To Make Allotment

(D) All of the Above

Answer

Answer: D

40. Which of the following will define, when appropriation of a certain number of shares is made to an applicant in response to his application? (C.S. Foundation, Dec. 2012)

(A) Share allotment

(B) Share forfeiture

(C) Share trading

(D) Share Purchase

Answer

Answer: A

41. Issue of shares at a price lower than its face value is called :

(A) Issue at a Loss

(B) Issue at a Profit

(C) Issue at a Discount

(D) Issue at a Premium

Answer

Answer: C

42. According to Companies Act, Minimum Subscription has been fixed at ……….. of the issued amount.

(A) 25%

(B) 50%

(C) 90%

(D) 100%

Answer

Answer: C

43. One of the conditions, in addition to others, for allotment of shares is :

(A) Resolution in General Meeting

(B) Receiving Minimum Subscription

(C) Full Subscription by Public

(D) Full Payment on Application

Answer

Answer: B

44. Persons who start a company are called ……………….

(A) Shareholders

(B) Directors

(C) Promoters

(D) Auditors

Answer

Answer: C

45. Minimum subscription amount of 90% is related to which share capital :

(A) Authorised Capital

(B) Issued Capital

(C) Paid up Capital

(D) Reserve Capital

Answer

Answer: B

46. Share Application Account is in the nature of:

(A) Real Account

(B) Personal Account

(C) Nominal Account

(D) None of the above

Answer

Answer: B

47. As per SEBI Guidelines, Application money should not be less than ……………. of the issue price of each share.

(A) 10%

(B) 15%

(C) 25%

(D) 50%

Answer

Answer: C

48. 4,000 Equity Shares of ₹10 each were issued at 8% premium to the promoters of a company for their services. Which account will be debited?

(A) Share Capital Account

(B) Goodwill Account/Incorporation Cost Account

(C) Securities Premium Reserve Account

(D) Cash Account

Answer

Answer: B

49. If vendors are issued fully paid shares of ₹1,25,000 in consideration of net assets of ?1,50,000, the balance of ₹25,000 will be credited to :

(A) Statement of Profit & Loss

(B) Goodwill Account

(C) Security Premium Reserve Account

(D) Capital Reserve Account

Answer

Answer: C

50. Issue of shares at a price higher than its face value is called :

(A) Issue at a Profit

(B) Issue at a Premium

(C) Issue at a Discount

(D) Issue at a Loss

Answer

Answer: B

51. On issue of shares Premium is :

(A) Profit

(B) Income

(C) Revenue Receipt

(D) Capital Profit

Answer

Answer: D

52. Which of the following is not a capital profit?

(A) Profit prior to incorporation of the company

(B) Profit from the sale of fixed assets

(C) Premium on issue of shares

(D) Compensation received on the termination of a contract

Answer

Answer: D

53. Maximum limit of Premium on shares is:

(A) 5%

(B) 10%

(C) No Limit

(D) 100%

Answer

Answer: C

54. When a company issues shares at a premium, the amount of premium should be received by the company :

(A) Along with application money

(B) Along with allotment money

(C) Along with calls

(D) Along with any of the above

Answer

Answer: D

55. Amount of securities premium can be utilised for :

(A) Writing oil’the preliminary expenses of the company

(B) Issuing bonus shares to ihe shareholders of the company

(C) Buy-back of its own shares

(D) All of the above .

Answer

Answer: D

56. For whal purpose securities premium reserve account cannot be utilized? (CPT; Dec. 2010)

(A) Amortization of preliminary expenses

(B) Distribution of dividend

(C) Issue of fully paid bonus shares

(D) Buy Back of own shares

Answer

Answer: B

57. Premium on the issue of shares should be shown :

(A) On the Assets side of balance sheet

(B) On the Equity & Liabilities side of balance sheet

(C) In profit & loss Statement

(D) None of the Above

Answer

Answer: B

58. A Company issued 50,000 shares of ₹20 each at 5% premium. ₹10 were payable on application and balance on allotment. What will be the allotment amount?

(A) ₹5,00,000

(B) ₹4,75,000

(C) ₹5,50,000

(D) ₹5,25,000

Answer

Answer: C

59. Interest on calls in arrears is charged according to Table F at:

(A) 6% p.a.

(B) 10% p.a.

(C) 5% p.a.

(D) 12% p.a.

Answer

Answer: B

60. Amount of Calls in Arrears is shown in the Balance Sheet

(A) as deduction from issued capital

(B) as deduction from subscribed capital

(C) as addition to subscribed capital

(D) on the assets side

Answer

Answer: B

61. As per Table F, the Company is required to pay …………. interest on the amount of calls in advance

(A) 12% p.a.

(B) 5% p.a.

(C) 10% p.a.

(D) 6% p.a.

Answer

Answer: A

62. Amount of Calls in Advance is

(A) Added to Share Capital

(B) Deducted from Share Capital

(C) Shown on the Assets side

(D) Shown on the Equity & Liabilities side

Answer

Answer: D

63. Following amounts were payable on issue of shares by a Company : ₹3 on application, ₹3 on allotment. ₹2 on lirst call and ₹2 on final call. X holding 500 shares paid only application and allotment money whereas Y holding 400 shares did not pay final call. Amount of calls in arrear will be :

(A) ₹3,800

(B) ₹2,800

(C) ₹1,800

(D) ₹6,200

Answer

Answer: B

64. The subscribed capital of a company is ?80,00,000 and the nominal value of the share is ? 100 each. There were no calls in arrear till the final call was made. The final call made was paid on,77,500 shares only. The balance in the calls in arrear amounted to ?62,500. Calculate the final call on share.

(A) ₹7

(B) ₹20

(C) ₹22

(D) ₹25

Answer

Answer: D

65. A shareholder holding 600 shares paid the amount of call @ ₹5 per share on 1st November 2018 whereas the call was due on 1st March 2019. Interest on calls in advance as per Table F will be :

(A) ₹45

(B) ₹60

(C) ₹50

(D) ₹120

Answer

Answer: D

66. From which account, expenses on issue of shares will be written off first of all:

(A) Statement of Profit and Loss

(B) Miscellaneous Expenditure Account

(C) Share Issue Expenses Account

(D) Securities Premium Reserve Account

Answer

Answer: D

67. Pro-rata allotment of shares is made when there is :

(A) Under subscription

(B) Oversubscription

(C) Equal subscription

(D) As and when desired by directors

Answer

Answer: B

68. Authorised capital of a Company is div ided into 5,00,000 shares of ₹10 each. It issued 3,00,000 shares. Public applied for 3,60,000 shares. Amount of issued capital will be :

(A) ₹30,00,000

(B) ₹36,00,000

(C) ₹50,00,000

(D) ₹6,00,000

Answer

Answer: A

69. A Company invited applications for 1,00,000 shares and it received applications for 1,50,000 shares. Applications for 30,000 shares were rejected and the remaining were allotted shares on prorata basis. How many shares an applicant for 3,000 shares will be allotted :

(A) 2,500 Shares

(B) 3,600 Shares

(C) 4,500 Shares

(D) 2,000 Shares

Answer

Answer: A

70. E Ltd. had allotted 10,000 shares to the applicants of 14,000 shares on pro-rata basis. The amount payable on application was ₹2. F applied for 420 shares. The number of shares allotted and the amount carried forward for adjustment against allotment money due from F will be : (C.F. Foundation, June 2013)

(A) 60 shares; ₹120

(B) 340 shares; ₹160

(C) 320 shares, ₹200

(D) 300 shares; ₹240

Answer

Answer: D

71. If applicants for 80,000 shares were allotted 60,000 shares on prorata basis, the shareholder who was allotted 1,200 shares must have applied for :

(A) 900 Shares

(B) 3,600 Shares

(C) 1,600 Shares

(D) 4,800 Shares

Answer

Answer: C

72. A Company offered 50,000 shares of ?10 each at par payable as to ?3 on applications, ?5 on allotment and the balance on final call. Applications were received for 60,000 shares and the allotment was made pro-rata. The excess application money was to be adjusted on allotment and call. How much amount will be transferred from Share Application A/c to Share Allotment A/c?

(A) ₹1,80,000

(B) ₹30,000

(C) ₹1,50,000

(D) ₹50,000

Answer

Answer: B

73. A company issued 4,000 equity shares of ₹10 each at par payable as under : On application ₹3; on allotment ₹2; on first call ₹4 and on final call ₹1 per share.

Applications were received for 13,000 shares. Applications for 3,000 shares were rejected and pro-rata allotment was made to the applicants for 10,000 shares. How much amount will be received in cash on first call? Excess application money is adjusted towards amount due on allotment and calls.

(A) ₹6,000

(B) Nil

(C) ₹16,000

(D) ₹10,000

Answer

Answer: A

74. A company issued 4,000 equity shares of ₹10 each at par payable as under : On application ₹3; on allotment ₹2; on first call ₹4 and on final call ?1 per share.

Applications were received for 10,000 shares. Allotment was made pro-rata. How much amount will be received in cash on allotment?

(A) ₹8,000

(B) ₹12,000

(C) Nil

(D) None

Answer

Answer: C

75. A company issued 5.000 equity shares of ₹100 each at par payable as to :

₹40 on application; ?50 on allotment and ₹10 on call.

Applications were received for 8,000 shares. Allotment was made on pro-rata. How much amount will be received in cash on allotment?

(A) ₹2,50,000

(B) ₹1,20,000

(C) ₹1,30,000

(D) ₹50,000

Answer

Answer: C

76. A Company purchased a building for ₹3,60,000 and issued as payment equity shares at 20% premium. Journal Entry will be :

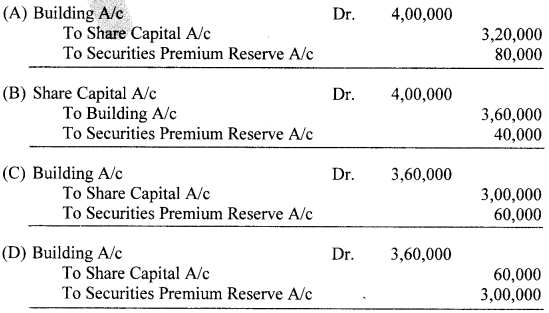

Answer

Answer: C

77. A Company purchased a Building for ₹12,00,000 out of which ₹2,00,000 were paid in cash. Balance amount was paid by issue of equity shares of ₹10 each at 25% premium. How many shares will be issued by the Company :

(A) 1,00,000 Shares

(B) 80,000 Shares

(C) 1,20,000 Shares

(D) 96,000 Shares

Answer

Answer: B

78. If shares of ₹4,00,000 are issued for purchase of assets of ₹5,00,000, ₹1,00,000 will be treated as ……………………. :

(A) Discount

(B) Premium

(C) Profit

(D) Loss

Answer

Answer: B

79. A Building was purchased for ₹9,00,000 and payment was made in ? 100 shares at 20% premium. Securities Premium Reserve A/c will be ……………….

(A) Debited by ₹1,50,000

(B) Credited by ₹1,50,000

(C) Debited by ₹1,80,000

(D) Credited by ₹1,80,000

Answer

Answer: B

80. A company purchased machinery for ₹1,80,000 and in consideration issued shares at 20% premium. What will be the face value of shares issued :

(A) ₹1,50,000

(B) ₹1,44,000

(C) ₹1,80,000

(D) ₹2,16,000

Answer

Answer: A

(v) Forfeiture of Shares

81. Forfeiture of shares results in the reduction of:

(A) Subscribed Capital

(B) Authorised Capital

(C) Reserve Capital

(D) Fixed Assets

Answer

Answer: A

82. Which one of the following items is not a part of subscribed capital?

(A) Equity Shares

(B) Preference Shares

(C) Forfeited Shares

(D) Bonus Shares

Answer

Answer: C

83. At the time of forfeiture of shares the share capital account is debited with (CPT, June 2011)

(A) Face value

(B) Called up value

(C) Paid up value

(D) Issued value

Answer

Answer: B

84. Voluntary return of shares for concellation by the shareholders is called

(A) Cancellation of shares

(B) Forfeiture

(C) Surrender of shares

(D) None of these

Answer

Answer: C

85. If the Premium on the forfeited shares has already been received, then Securities Premium A/c should be : (CPT, June 2011)

(A) Credited

(B) Debited

(C) No treatment

(D) None of these

Answer

Answer: C

86. Balance of share forfeiture account is shown in the balance sheet under the head …………… (CPT, Dec. 2010)

(A) Share Capital Account

(B) Reserve and Surplus

(C) Current Liabilities and Provisions

(D) Unsecured Loans

Answer

Answer: A

87. On an equity share of ₹10 the company has called up ₹8 but ₹6 have been received by the company is forfeited, the capital account should be debited by:

(A) ₹10

(B) ₹8

(C) ₹6

(D) ₹2

Answer

Answer: B

88. If a share of ₹10 issued at a premium of ₹3 on which the full amount has been called and ₹8 (including premium) paid is forfeited the capital account should be debited with:

(A) ₹5

(B) ₹8

(C) ₹10

(D) ₹13

Answer

Answer: C

89. If a share of ₹10 issued at a premium of n on which ₹9 (including premium) have been called and ₹7 including premium is paid is forfeited, the capital account should be debited by :

(A) ₹10

(B) ₹7

(C) ₹8

(D) ₹9

Answer

Answer: C

90. 600 shares of ₹10 each were forfeited for non-payment of ₹2 per share on first call and ₹5 per share on final call. Share Forfeiture Account will be credited with:

(A) ₹1,200

(B) ₹1,800

(C) ₹3,000

(D) ₹4,200

Answer

Answer: B

91. 800 shares of ₹10 each issued at 20% premium were forfeited for non-payment of allotment money of ₹5 (including premium) and first & final of 73 per share. Share Forfeiture Account will be credited with :

(A) ₹1,600

(B) ₹2,400

(C) ₹3,200

(D) ₹4,800

Answer

Answer: C

92. 800 shares of ₹10 each issued at 30% premium (to be paid on allotment) were forfeited for non-payment of ₹2 per share on first call and 72 per share on final call. Share Forfeiture Account will be credited with :

(A) ₹2,400

(B) ₹4,800

(C) ₹3,200

(D) ₹7,200

Answer

Answer: B

93. A Company forfeited 300 shares of ₹10 each, ₹8 per share called up, on which A had paid application and allotment money of ₹6 per share. Share Forfeiture Account will be credited with :

(A) ₹600

(B) ₹1,800

(C) ₹1,200

(D) ₹2,400

Answer

Answer: B

94. On 300 equity shares of ₹10 the company has called up ₹8 but ₹6 have been received by the company are forfeited, the forfeiture account should be credited by :

(A) ₹2,400

(B) ₹1,200

(C) ₹1,800

(D) ₹600

Answer

Answer: C

95. If 400 shares of ₹10 issued at a premium of ₹3 on which the full amount has been called and ₹8 (including premium) have been received are forfeited, the forfeiture account should be credited with :

(A) ₹3,200

(B) ₹2,000

(C) ₹1,200

(D) ₹2,800

Answer

Answer: B

96. If 500 shares of ₹10 issued at a premium of ₹1 on which ₹9 (including premium) have been called and ₹7 including premium have been paid are forfeited, the forfeiture account should be credited by :

(A) ₹3,000

(B) ₹3,500

(C) ₹4,000

(D) ₹4,500

Answer

Answer: A

97. A Company forfeited the following shares :

200 shares of ₹10 each; called up ₹9 per share, paid-up ₹7 per share. Journal Entry for forfeiture will be) :

Answer

Answer: C

98. X Ltd. forfeited 500 shares of ₹10 each, ₹7 called up, issued at a premium of ₹2 per share to be paid at the time of allotment for non-payment of first call of X2 per share. Entry on forfeiture will be :

Answer

Answer: D

99. The amount of discount on reissue of forfeited shares cannot exceed : (CPTDec., 2012)

(A) 5% of the face value

(B) 10% of the face value

(C) The amount received on forfeited shares

(D) The amount not received on forfeited shares

Answer

Answer: C

100. Discount allowed on re-issue of forfeited shares is debited to :

(A) Share Capital A/c

(B) Share forfeiture A/c

(C) Statement of Profit & Loss

(D) General Reserve A/c

Answer

Answer: B

101. The balance of the forfeited shares account after re-issue of forfeited shares is transferred to :

(A) Statement of Profit & Loss

(B) Share Capital A/c

(C) Capital Reserve A/c

(D) General Reserve A/c

Answer

Answer: C

102. A Ltd. forfeited 500 shares of ₹10 each fully called up for non-payment of final call of ₹3 per share 300 of these shares were reissued at ?9 per share, fully paid up. What is the amount to be transferred to Capital Reserve Account?

(A) ₹3,500

(B) ₹2,100

(C) ₹3,200

(D) ₹1,800

Answer

Answer: D

103. L Ltd. forfeited 400 shares of ₹10 each, ₹7 called up, for non-payment of first call of ₹2 per share. Out of these, 300 shares were reissued for ₹6 per share as ₹7 paid up. What is the amount to be transferred to Capital Reserve Account?

(A) ₹1,700

(B) ₹1,200

(C) ₹2,100

(D) ₹300

Answer

Answer: B

104.400 shares of ₹10, on which ?8 has been called and ?5 has been paid, are forfeited. Out of these, 300 shares are re-issued for ?9 as fully paid. What is the amount to be transferred to. Capital Reserve Account?

(A) ₹1,200

(B) ₹1,600

(C) ₹2,000

(D) ₹1,700

Answer

Answer: A

105. R Ltd. forfeited 600 shares of ₹100 each ₹70 called up on which Mahesh has paid application and allotment money of ₹50 per share. Of these, 400 shares were re-issued to Naresh as fully paid-up for ₹110 per share. What is the amount to be transferred to Capital Reserve?

(A) ₹30,000

(B) ₹36,000

(C) ₹24,000

(D) ₹20,000

Answer

Answer: D

106. Madhu Ltd. forfeited 800 shares of ₹10 each issued at 10% premium to Shyam (₹9 called up) on which he did not pay ₹3 of allotment (including premium) and first call of ₹2. Out of these, 600 shares were re-issued to Ram as fully paid up for ₹9 per share. What is to amount to be transferred to capital Reserve?

(A) ₹2,400

(B) ₹1,800

(C) ₹3,000

(D) ₹3,600

Answer

Answer: A

107. If a share of 7 100 on which 760 has been paid, is forfeited, it can be re-issued at the minimum price of:

(A) ₹60

(B) ₹100

(C) ₹40

(D) ₹140

Answer

Answer: C

108. A Company forfeited 1,000 shares of ₹10 each fully called, on which ₹6,000 has been paid. Out of these 800 shares were reissued upon payment of ₹6,600. What is the amount to be transferred to Capital Reserve?

(A) ₹4,800

(B) ₹6,000

(C) ₹4,600

(D) ₹3,400

Answer

Answer: D

109. A company forfeited 700 shares of 710 each, on which only 75 per share was paid. Of these, 200 shares were reissued at 79 per share. Amount from Share Forfeiture Account to Capital Reserve Account will be transferred :

(A) ₹800

(B) ₹200

(C) ₹3,500

(D) ₹2,500

Answer

Answer: A

110. 300 equity shares of ₹10 each were issued at ₹5 per share premium. Only ₹4 per share on application has been paid on these shares. These shares were forfeited. Later on out of these, 200 shares were reissued at ₹12 per share as fully paid. What will be amount of Capital Reserve?

(A) ₹500

(B) ₹1,200

(C) ₹200

(D) ₹800

Answer

Answer: D

111. 700 shares of ₹10 each were reissued as ₹9 paid up for ₹7 per share. Entry for reissue will be :

Answer

Answer: C

112. A Ltd. forfeited 2,000 shares of ₹10 each fully called up for non-payment of final call of ₹2 per share. 1,200 of these shares were reissued at 7₹7 per share, fully paid up. What is the amount to be transferred to Capital Reserve Account?

(A) ₹7,600

(B) ₹1,200

(C) ₹12,400

(D) ₹6,000

Answer

Answer: D

113. Using information given in Q. 112 what is the net balance in Share Forfeiture Account:

(A) ₹9,600

(B) ₹6,400

(C) ₹16,000

(D) ₹2,800

Answer

Answer: B

114. 6 Ltd. forfeited 300 shares of ₹100 each, ₹70 called up, for non-payment of first call of ₹20 per share. Out of these, 200 shares were reissued for 760 per share as ₹70 paid up. What is the amount to be transferred to Capital Reserve Account?

(A) ₹13,000

(B) ₹8,000

(C) ₹2,000

(D) ₹7,000

Answer

Answer: B

115. 2,000 shares of ₹10, on which ₹7 has been called and ₹5 has been paid, are forfeited. Out of these, 1,500 shares are re-issued for ₹9 as fully paid. What is the amount to be transferred to Capital Reserve Account?

(A) ₹6,000

(B) ₹7,500

(C) ₹10,000

(D) ₹8,500

Answer

Answer: A

116. X Ltd. forfeited 400 shares of ₹20 each ₹15 called up on which application and allotment money of ₹11 per share has been received. Of these, 100 shares were re-issued as fully paid-up for ₹24 per share. What is the amount to be transferred to Capital Reserve?

(A) ₹1,500

(B) ₹4,400

(C) ₹1,100

(D) ₹3,500

Answer

Answer: C

117. z Ltd. forfeited 300 shares of ₹10 each issued at 20% premium (₹9 called up) on which ₹4 of allotment (including premium) and first call of ₹2 has not been received. Out of these, 100 shares were re-issued as fully paid up for ₹9 per share. What is to amount to be transferred to capital Reserve?

(A) ₹400

(B) ₹300

(C) ₹500

(D) ₹600

Answer

Answer: A

118. Using information given in Q. 117, what is the net balance left in Share Forfeiture Account:

(A) ₹1,400

(B) ₹1,500

(C) ₹900

(D) ₹1,000

Answer

Answer: D

119. P Ltd. forfeited 150 shares of ₹10 each, issued at a premium of ₹2, for non-payment of the final call of ₹3. Out of these, 100 shares were re-issued at ₹11 per share. How much amount would be transferred to capital reserve? (C.S. Foundation, Dec. 2012)

(A) ₹700

(B) ₹500

(C) ₹1,200

(D) ₹300

Answer

Answer: A

120. XY Limited issued 2,50,000 equity shares of ₹10 each at a premium of ₹10 each payable as ₹2.5 on application, ₹4 on allotment and balance on the first and final call. Applications were received for 5,00,000 equity shares but the company allotted to them only 2,50,000 shares. Excess money was applied towards amount due on allotment. Last call on 500 shares was not received and shares were forfeited after due notice. This is a case of: (C.S. Foundation, June 2013)

(A) Over subscription

(B) Pro-rata allotment

(C) Forfeiture of Shares

(D) All of the above

Answer

Answer: D

121. Metacaf Ltd. issued 50,000 shares of ₹100 each payable ₹20 on application (on 1st May 2012); ₹30 on allotment (on 1st January 2013); ₹20 on first call (on 1st July 2013) and the balance on final call (on 1st February 2014). Shankar, a shareholder holding 5,000 shares did not pay the first call on the due date. The second call was made and Shankar paid the first call amount along with the second call. All sums due were received.

Total amount received on 1st February was : (C.B.S.E. Sample Paper, 2015)

(A) ₹15,00,000

(B) ₹16,00,000

(C) ₹10,00,000

(D) ₹11,00,000

Answer

Answer: B

We hope the given Accountancy MCQs for Class 12 with Answers Chapter 7 Issue of Shares will help you. If you have any query regarding CBSE Class 12 Accountancy Issue of Shares MCQs Pdf, drop a comment below and we will get back to you at the earliest.