Free PDF Download of CBSE Accountancy Multiple Choice Questions for Class 12 with Answers Chapter 2 Change in Profit Sharing Ratio among the Existing Partners. Accountancy MCQs for Class 12 Chapter Wise with Answers PDF Download was Prepared Based on Latest Exam Pattern. Students can solve NCERT Class 12 Accountancy Change in Profit Sharing Ratio among the Existing Partners MCQs Pdf with Answers to know their preparation level.

Change in Profit Sharing Ratio among the Existing Partners Class 12 Accountancy MCQs Pdf

Select the Best Alternate :

1. Sacrificing Ratio :

(A) New Ratio – Old Ratio

(B) Old Ratio – New Ratio

(C) Old Ratio – Gaining Ratio

(D) Gaining Ratio – Old Ratio

Answer

Answer: B

2. Gaining Ratio :

(A) New Ratio – Sacrificing Ratio

(B) Old Ratio – Sacrificing Ratio

(C) New Ratio – Old Ratio

(D) Old Ratio – New Ratio

Answer

Answer: C

3. A and B were partners in a firm sharing profit or loss equally. With effect from 1st April 2019 they agreed to share profits in the ratio of 4 : 3. Due to change in profit sharing ratio, A’s gain or sacrifice will be :

(A) Gain \(\frac{1}{14}\)

(B) Sacrifice \(\frac{1}{14}\)

(C) Gain \(\frac{4}{7}\)

(D) Sacrifice \(\frac{3}{7}\)

Answer

Answer: A

4. A and B were partners in a firm sharing profit or loss equally. With effect from 1st April, 2019 they agreed to share profits in the ratio of 4 : 3. Due to change in profit sharing ratio, B’s gain or sacrifice will be :

(A) Gain \(\frac{1}{14}\)

(B) Sacrifice \(\frac{1}{14}\)

(C) Gain \(\frac{4}{7}\)

(D) Sacrifice \(\frac{3}{7}\)

Answer

Answer: B

5. A and B were partners in a firm sharing profit or loss in the ratio of 3 : 5. With effect from 1st April, 2019, they agreed to share profits or losses equally. Due to change in profit sharing ratio, A’s gain or sacrifice will be :

Answer

Answer: B

6. A and B were partners in a firm sharing profits and losses in the ratio of 2 : 1. With effect from 1st January 2019 they agreed to share profits and losses equally. Individual partner’s gain or sacrifice due to change in the ratio will be :

Answer

Answer: B

7. A and B share profits and losses in the ratio of 3 : 2. With effect from 1st . January, 2019, they agreed to share profits equally. Sacrificing ratio and Gaining Ratio will be :

Answer

Answer: C

8. A and B were partners in a firm sharing profit or loss in the ratio of 3 : 1. With effect from Jan. 1, 2019 they agreed to share profit or loss in the ratio of 2 : 1. Due to change in profit-loss sharing ratio, B’s gain or sacrifice will be :

(A) Gain \(\frac{1}{12}\)

(B) Sacrifice \(\frac{1}{12}\)

(C) Gain \(\frac{1}{3}\)

(D) Sacrifice \(\frac{1}{3}\)

Answer

Answer: A

9. A, B and C were partners sharing profit or loss in the ratio of 7 : 3 : 2. From Jan. 1,2019 they decided to share profit or loss in the ratio of 8 : 4 : 3. Due to change in the profit-loss sharing ratio, B’s gain or sacrifice will be :

(A) Gain \(\frac{1}{60}\)

(B) Sacrifice \(\frac{1}{60}\)

(C) Gain \(\frac{2}{60}\)

(D) Sacrifice \(\frac{3}{60}\)

Answer

Answer: A

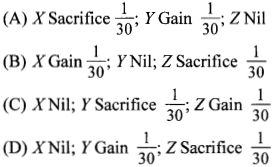

10. A y and Z are partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. The partners decide to share future profits and losses in the ratio of 3:2:1. Each partner’s gain or sacrifice due to change in the ratio will be :

Answer

Answer: D

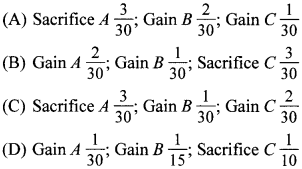

11. A, B and C were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. The partners decide to share future profits and losses in the ratio of 2:2:1. Each partner’s gain or sacrifice due to change in ratio will be :

Answer

Answer: A

12. A, B and C were partners in a firm sharing profits and losses in the ratio of 4 : 3 : 2. The partners decide to share future profits and losses in the ratio of 2:2: 1. Each partner’s gain or sacrifice due to change in the ratio will be :

Answer

Answer: C

13. A, B and C were partners in a lirm sharing profits in 4 : 3 : 2 ratio. They decided to share future profits in 4 : 3 : 1 ratio. Sacrificing ratio and gaining ratio will be :

Answer

Answer: D

14. X, Y and Z were partners sharing profits in the ratio 2:3:4 with effect from 1st January, 2019 they agreed to share profits in the ratio 3:4:5. Each partner’s gain or sacrifice due to change in the ratio will be :

Answer

Answer: A

15. X, 7 and Z were in partnership sharing profits in the ratio 4 : 3 : 1. The partners agreed to share future profits in the ratio 5 : 4 : 3. Each partner’s gain or sacrifice due to change in ratio will be :

Answer

Answer: A

16. A, B and C are equal partners in the firm. It is now agreed that they will share the future profits in the ratio 5:3:2. Sacrificing ratio and gaining ratio of different partners will be :

Answer

Answer: C

17, The excess amount which the firm can get on selling its assets over and above the saleable value of its assets is called :

(A) Surplus

(B) Super profits

(C) Reserve

(D) Goodwill

Answer

Answer: D

18. Which of the following is NOT true in relation to goodwill?

(A) It is an intangible asset

(B) It is fictitious asset

(C) It has a realisable value

(D) None of the above

Answer

Answer: B

19. When Goodwill is not purchased goodwill account can :

(A) Never be raised in the books

(B) Be raised in the books

(C) Be partially raised in the books

(D) Be raised as per the agreement of the partners

Answer

Answer: A

20. The Goodwill of the firm is NOT affected by : (CPT; June 2011)

(A) Location of the firm

(B) Reputation of firm

(C) Better customer service

(D) None of the above

Answer

Answer: D

21. Capital employed by a partnership firm is ₹5,00,000. Its average profit is ₹60,000. The normal rate of return in similar type of business is 10%. What is the amount of super profits? (C.S. Foundation, Dec., 2012)

(A) ₹50,000

(B) ₹10,000

(C) ₹6,000

(D) ₹56,000

Answer

Answer: B

22. Weighted average method of calculating goodwill is used when : (CPT; June 2009)

(A) Profits are not equal

(B) Profits show a trend

(C) Profits are fluctuating

(D) None of the above

Answer

Answer: B

23. The profits earned by a business over the last 5 years are as follows : ₹12,000; ₹13,000; ₹14,000; ₹18,000 and ₹2,000 (loss). Based on 2 years purchase of the last 5 years profits, value of Goodwill will be :

(A) ₹23,600

(B) ₹22,000

(C) ₹1,10,000

(D) ₹1,18,000

Answer

Answer: B

24. The average profit of a business over the last five years amounted to ₹60,000. The normal commercial yield on capital invested in such a business is deemed to be 10% p.a. The net capital invested in the business is ₹5,00,000. Amount of goodwill, if it is based on 3 years purchase of last 5 years superprofits will be :

(A) ₹1,00.000

(B) ₹1,80,000

(C) ₹30.000

(D) ₹1,50,000

Answer

Answer: C

25. Under the capitalisation method, the formula for calculating the goodwill is : (CPT; Dec. 2011)

(A) Super profits multiplied by the rate of return

(B) Average profits multiplied by the rate of return

(C) Super profits divided by the rate of return

(D) Average profits divided by the rate of return

Answer

Answer: C

26. The net assets of a firm including fictitious assets of ₹5,000 are ₹85,000. The net liabilities of the firm are ₹30,000. The normal rate of return is 10% and the average profits of the firm are ₹8,000. Calculate the goodwill as per capitalisation of super profits.

(A) ₹20,000

(B) ₹30,000

(C) ₹25,000

(D) None of these

Answer

Answer: B

27. Total Capital employed in the firm is ₹8,00,000, reasonable rate of return is 15% and Profit for the year is ₹12,00,000. The value of goodwill of the firm as per capitalization method would be : (C.S. Foundation, June 2013)

(A) ₹82,00,000

(B) ₹12,00,000

(C) ₹72,00,000

(D) ₹42,00,000

Answer

Answer: C

28. The average capital employed of a firm is ?4,00,000 and the normal rate of return is 15%. The average profit of the firm is ?80,000 per annum. If the . remuneration of the partners is estimated to be ? 10,000 per annum, then on the basis of two years purchase of super-profit, the value of the Goodwill will be :

(A) ₹10,000

(B) ₹20,000

(C) ₹60,000

(D) ₹80,000

Answer

Answer: B

29. A firm earns ₹1,10,000. The normal rate of return is 10%. The assets of the firm amounted to ₹11,00,000 and liabilities to ₹1,00,000. Value of goodwill by capitalisation of Average Actual Profits will be : (C.S. Foundation Dec., 2012)

(A) ₹2,00,000

(B) ₹10,000

(C) ₹5,000

(D) ₹1,00,000

Answer

Answer: D

30. Capital invested in a firm is ₹5,00,000. Normal rate of return is 10%. Average profits of the firm are ₹64,000 (after an abnormal loss of ?4,000). Value of goodwill at four times the super profits will be :

(A) ₹72,000

(B) ₹40,000

(C) ₹2,40,000

(D) ₹1,80,000

Answer

Answer: A

31. P and Q were partners sharing profits and losses in the ratio of 3 : 2. They decided that with effect from 1st January, 2019 they would share profits and losses in the ratio of 5 : 3. Goodwill is valued at ? 1,28,000. In adjustment entry :

(A) Cr. P by ₹3,200; Dr. Q by ₹3,200

(B) Cr. P by ₹37,000; Dr. Q by ₹37,000

(C) Dr. P by ₹37,000; Cr. Q by ₹37,000

(D) Dr. P by ₹3,200 Cr. Q by ₹3,200

Answer

Answer: D

32. A, B and C are partners sharing profits in the ratio of 4 : 3 : 2 decided to share profits equally. Goodwill of the firm is valued at ? 10,800. In adjusting entry for goodwill :

(A) A’s Capital A/c Cr. by ₹4,800; B’s Capital A/c Cr. by ₹3,600; C’s Capital A/c Cr. by ₹2,400.

(B) A’s Capital A/c Cr. by ₹3,600; B’s Capital A/c Cr. by ₹3,600; C’s Capital A/c Cr. by ₹3,600.

(C) A’s Capital A/c Dr. by ₹1,200; C’s Capital A/c Cr. by ₹1,200;

(D) A’s Capital A/c Cr. by ₹1,200; C’s Capital A/c Dr. by ₹1,200

Answer

Answer: D

33. A, B and C were partners sharing profits and losses in the ratio of 7 : 3 : 2. From 1st January, 2019 they decided to share profits and losses in the ratio of 8:4:3. Goodwill is ₹1,20,000. In Adjustment entry for goodwill:

(A) Cr. A by ₹6,000; Dr. B by ?2,000; Dr. C by ₹4,000

(B) Dr. A by ₹6,000; Cr. B by ?2,000; Cr. C by ₹4000

(C) Cr. A by ₹6,000; Dr. B by ?4,000; Dr. C by ₹2,000

(D) Dr. A by ₹6,000; Cr. B by ?4,000; Cr. C by ₹2,000

Answer

Answer: A

34. P, Q and R were partners in a firm sharing profis in 5 : 3 : 2 ratio. They decided to share the future profits in 2 : 3 : 5. For this purpose the goodwill of the firm was valued at ₹1,20,000. In adjustment entry for the treatment of goodwill due to change in the profit sharing ratio :

(A) Cr. P by ₹24,000; Dr. R by ₹24,000

(B) Cr. P by ₹60,000; Dr. R by ₹60,000

(C) Cr. P by ₹36,000; Dr. R by ₹36,000

(D) Dr. P by ₹36,000; Cr. R by ₹36,000

Answer

Answer: C

35. A, B and C are partners in a firm sharing profits in the ratio of 3 : 4 : 1. They decided to share profits equally w.e.f. 1 st April, 2019. On that date the Profit and Loss Account showed the credit balance of ?96,000. Instead of closing the Profit and Loss Account, it was decided to record an adjustment entry reflecting the change in profit sharing ratio. In the journal entry :

(A) Dr. A by ₹4,000; Dr. B by ₹16,000; Cr. C by ₹20,000

(B) Cr. A by ₹4,000; Cr. B by ₹16,000; Dr. C by ₹20,000

(C) Cr. A by ₹16,000; Cr. B by ₹4,000; Dr. C by ₹20,000

(D) Dr. A by ₹16,000; Dr. B by ₹4,000; Cr. C by ₹20,000

Answer

Answer: B

36. A, B and C are partner sharing profits in the ratio of 1 : 2 : 3. On 1-4-2019 they decided to share the profits equally. On the date there was a credit balance of ? 1,20,000 in their Profit and Loss Account and a balance of ? 1,80,000 in General Reserve Account. Instead of closing the General Reserve Account and Profit and Loss Account, it is decided to record an adjustment entry for the same. In the necessary adjustment entry to give effect to the above arrangement:

(A) Dr. A by ₹50,000; Cr. B by ₹50,000

(B) Cr. A by ₹50,000; Dr. B by ₹50,000

(C) Dr. A by ₹50,000; Cr. Cby ₹50,000

(D) Cr. A by ₹50,000; Dr. Cby ₹50,000

Answer

Answer: C

37. X, Y and Z are partners in a firm sharing profits in the ratio 4 : 3 : 2. Their Balance Sheet as at 31-3-2019 showed a debit balance of Profit & Loss A/c ₹1,80,000. From 1-4-2019 they will share profits equally. In the necessary journal entry to give effect to the above arrangement when A Y and Z decided not to close the Profit & Loss Acccount:

(A) Dr. X by ₹20,000; Cr. Z by ₹20,000

(B) Cr. X by ₹20,000; Dr. Z by ₹20,000

(C) Dr. X by ₹40,000; Cr. Z by ₹40,000

(D) Cr. X by ₹40,000; Dr. Z by ₹40,000

Answer

Answer: A

38. Aran and Varan are partners sharing profits in the ratio of 4 : 3. Their Balance Sheet showed a balance of ? 5 6,000 in the General Reserve Account and a debit balance of ? 14,000 in Profit and Loss Account. They now decided to share the future profits equally. Instead of closing the General Reserve Account and Profit and Loss Account, it is decided to pass an adjustment entry for the same. In adjustment entry :

(A) Dr. Aran by ₹3,000; Cr. Varan by ₹3,000

(B) Dr. Aran by ₹5,000; Cr. Varan by ₹5,000

(C) Cr. Aran by ₹5,000; Dr. Varan by ₹5,000

(D) Cr. Aran by ₹3,000; Dr. Varan by ₹3,000

Answer

Answer: D

39. X, Y and Z are partners in a firm sharing profits in the ratio of 3 : 2 : 1. They decided to share future profits equally. The Profit and Loss Account showed a Credit balance of ₹60,000 and a General Reserve of ₹30,000. If these are not to be shown in balance sheet, in the journal entry :

(A) Cr. X by ₹15,000: Dr. Z by ₹15,000

(B) Dr. X by ₹15,000; Cr. Z by ₹15,000

(C) Cr. X by ₹45,000; Cr. Y by ₹30,000; Cr. Z by ₹15,000

(D) Cr. X by ₹30,000; Cr. Y by ₹30,000; Cr. Z by ₹30,000

Answer

Answer: C

40. X Y and Z are partners sharing profits and losses in the ratio 5 : 3 : 2. They decide to share the future profits in the ratio 3 : 2 : 1. Workmen compensation reserve appearing in the balance sheet on the date if no information is available for the same will be :

(A) Distributed to the partners in old profit sharing ratio

(B) Distributed to the partners in new profit sharing ratio

(C) Distributed to the partners in capital ratio

(D) Carried forward to new balance sheet without any adjustment

Answer

Answer: A

41. Any change in the relationship of existing partners which results in an end of the existing agreement and enforces making of a new agreement is called (C.B.S.E. Sample Paper, 2015)

(A) Revaluation of partnership.

(B) Reconstitution of partnership.

(C) Realization of partnership.

(D) None of the above.

Answer

Answer: B

We hope the given Accountancy MCQs for Class 12 with Answers Chapter 2 Change in Profit Sharing Ratio among the Existing Partners will help you. If you have any query regarding CBSE Class 12 Accountancy Change in Profit Sharing Ratio among the Existing Partners MCQs Pdf, drop a comment below and we will get back to you at the earliest.