TS Grewal Accountancy Class 12 Solutions Chapter 9 Issue of Debentures – Here are all the TS Grewal solutions for Class 12 Accountancy Chapter 9. This solution contains questions, answers, images, explanations of the complete Chapter 9 titled Issue of Debentures of Accountancy taught in Class 12. If you are a student of Class 12 who is using TS Grewal Textbook to study Accountancy, then you must come across Chapter 9 Issue of Debentures. After you have studied lesson, you must be looking for answers of its questions. Here you can get complete TS Grewal Solutions for Class 12 Accountancy Chapter 9 Issue of Debentures in one place.

TS Grewal Accountancy Class 12 Solutions Chapter 9 Issue of Debentures

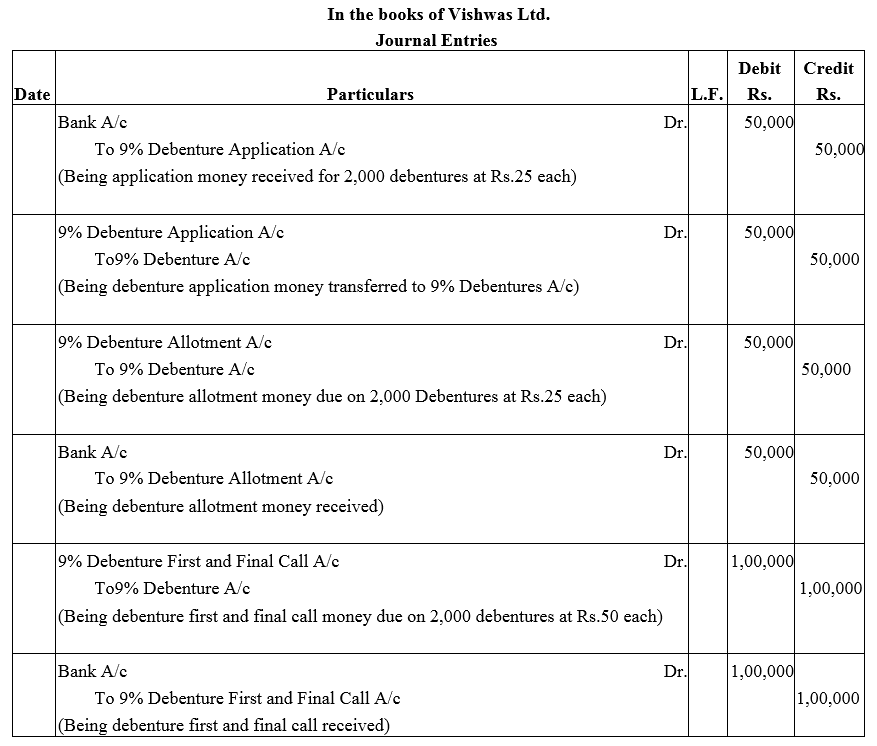

Question 1.

Vishwas Ltd. issued 2,000; 9% Debentures of ₹ 100 each payable as follows:

₹ 25 on application; ₹ 25 on allotment and ₹ 50 on first and final call.

Applications were received for all the debentures along with the application money did allotment was made. Call money was also received on the due date.

Pass necessary Journal entries in the books of the company.

Solution:

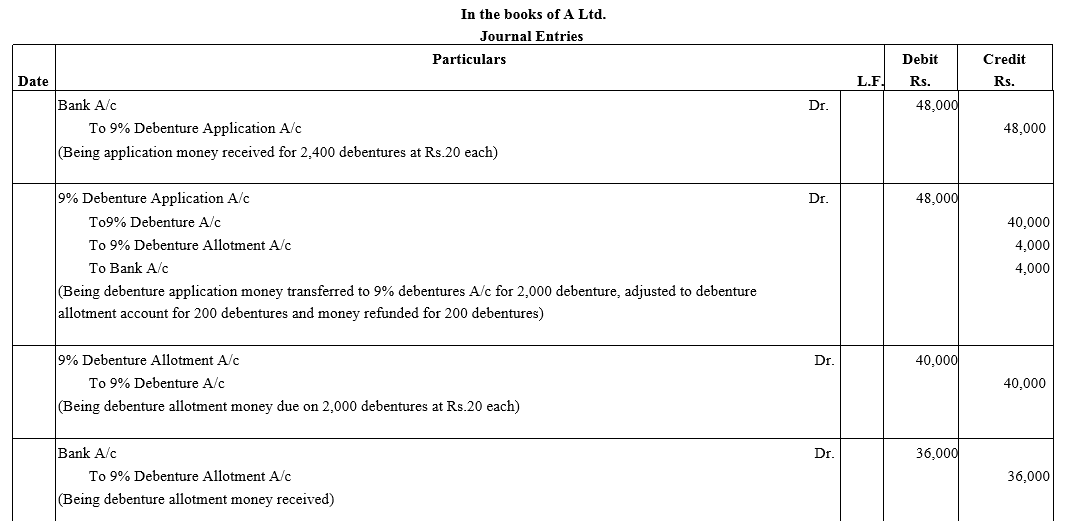

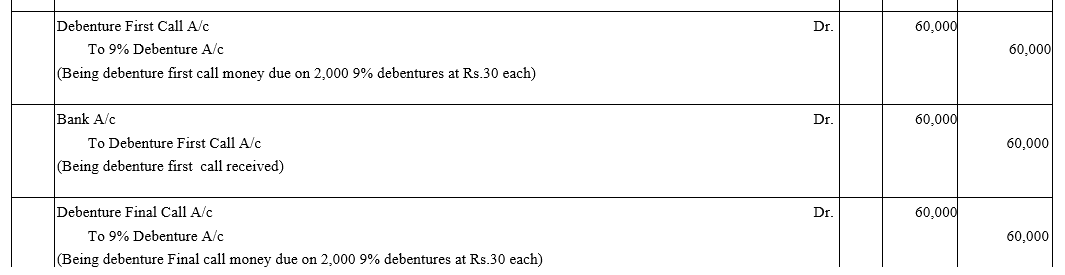

Question 2.

A Ltd. issued 2,000; 9% Debentures of ₹ 100 each on the following terms:

₹ 20 on applications ; ₹ 20 on allotment ; ₹ 30 on first call ; ₹ 30 on final call.

The public applied for 2,400 debentures. Applications for 1,800 debentures were accepted in full. Applications for 400 debentures were allotted 200 debentures and applications for 200 debentures were rejected. Pass necessary Journal entries.

Solution:

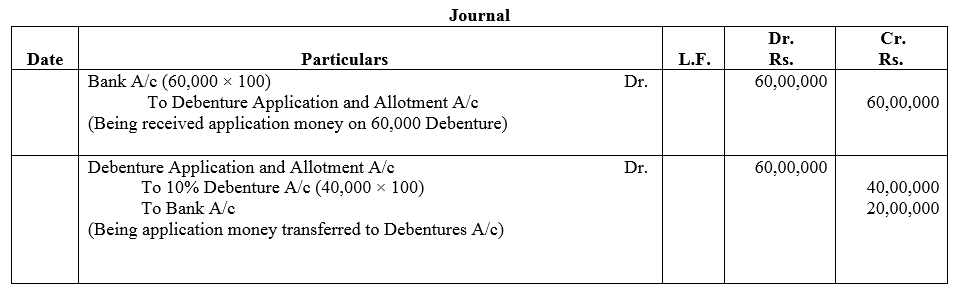

Question 3.

ABC Ltd. issued 40,000; 10% Debentures of ₹ 100 each at par for cash payable in full along with the application. Applications were received for 60,000 debentures. Debentures were allotted and excess application money was refunded. Pass Journal entries in the books of the company.

Solution:

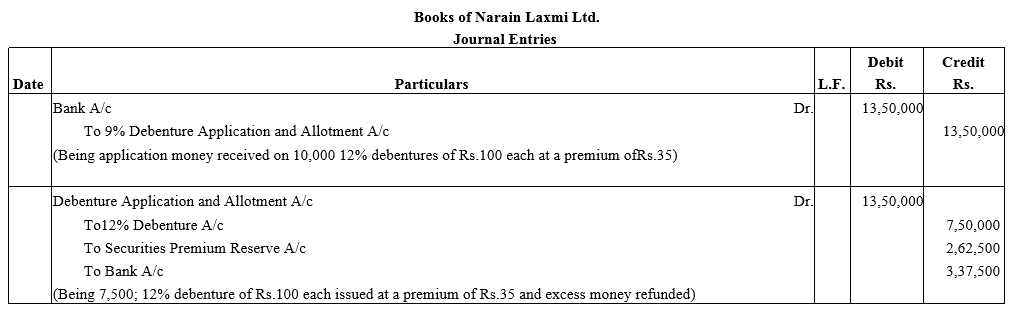

Question 4.

Narain Laxmi Ltd. invited applications for issuing 7,500; 12% Debentures of ₹ 100 each at a premium of ₹ 35 per debenture. The full amount was payable on application. Applications were received for 10,000 Debentures. Allotment was made to all the applications on pro rata.

Pass necessary Journal entries for the above transactions in the books of Narain Laxmi Ltd.

Solution:

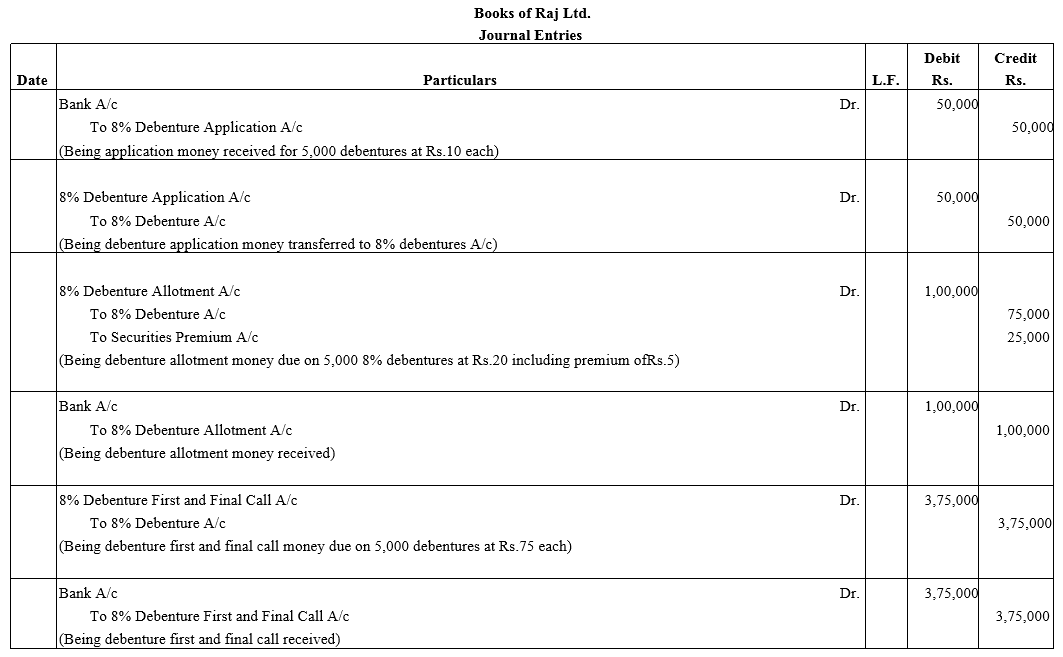

Question 5.

Raj Ltd. issued 5,000; 8% Debentures of ₹ 100 each at a premium of 5% payable as follows:

₹ 10 on application; ₹ 20 along with premium on allotment and balance on first and final call.

Pass necessary Journal entries.

Solution:

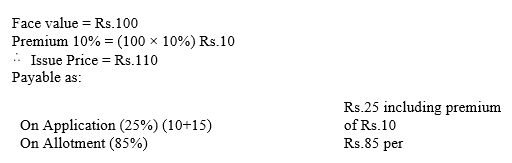

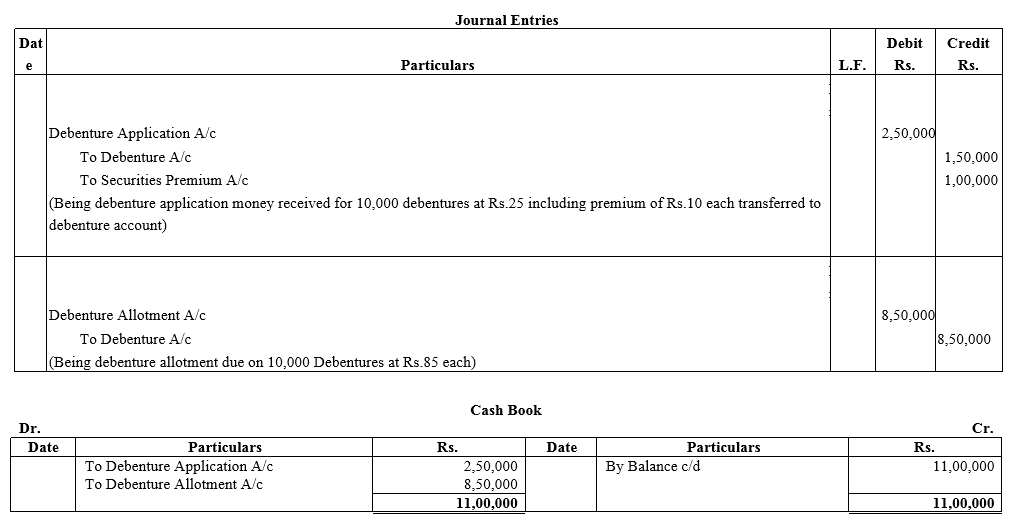

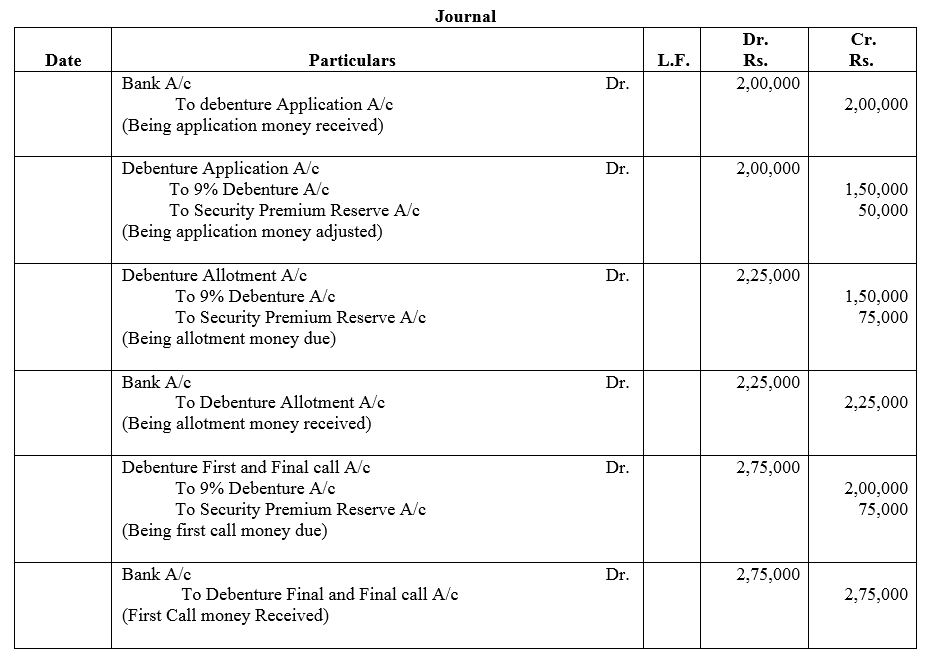

Question 6.

Nipa Limited issued ₹ 10,00,000 Debentures of ₹ 100 each at a premium of 10%, payable 25% on application (including premium) and the balance on allotment. The debentures were applied for and the amount was dully received.

You are required to give Journal entries and prepare Cash Book.

Solution:

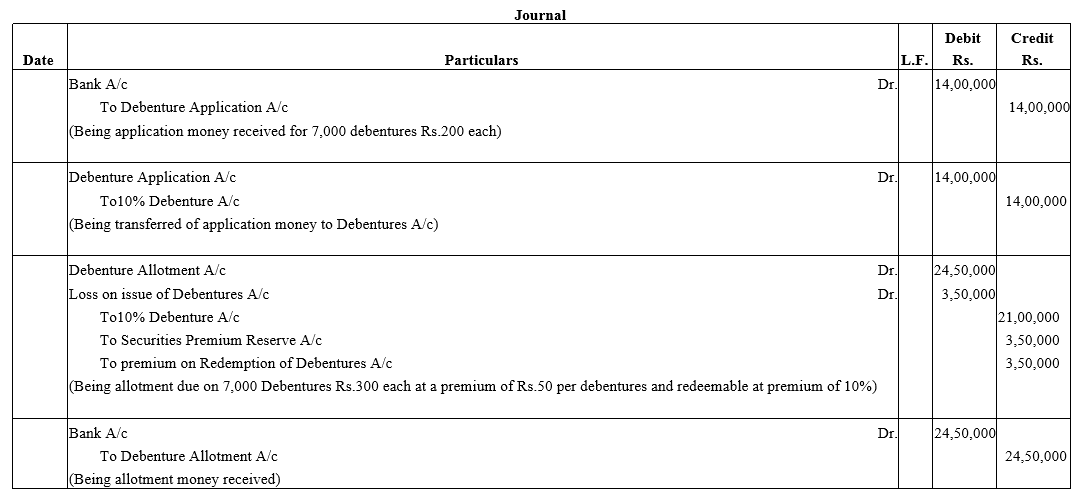

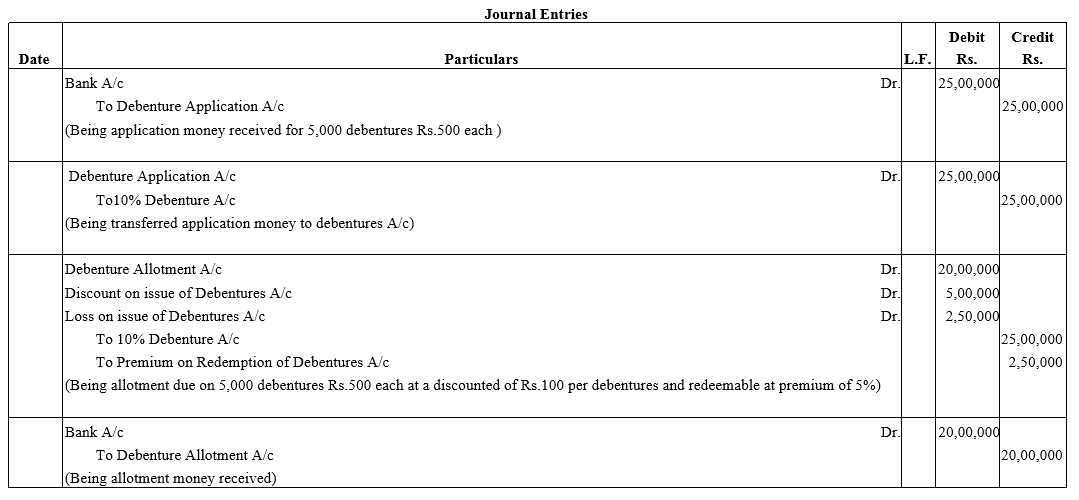

Question 7.

Alok Ltd. issued 7,000, 10% Debentures of ₹ 500 each at a premium of ₹ 50 per debenture redeemable at a premium of 10% after 5 years. According to the terms of issue, ₹ 200 was payable on application and balance on allotment.

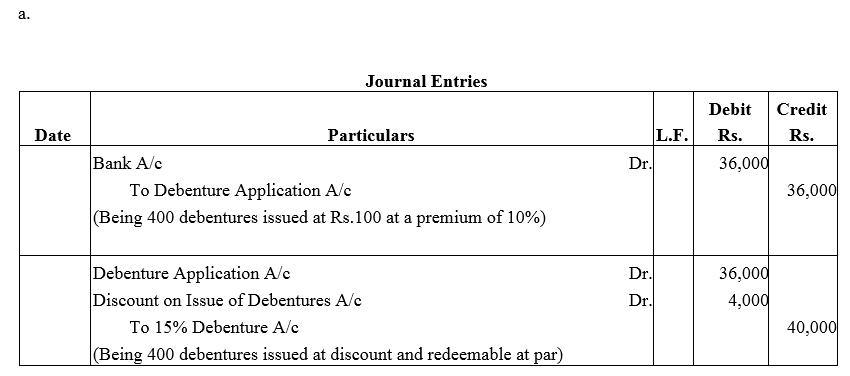

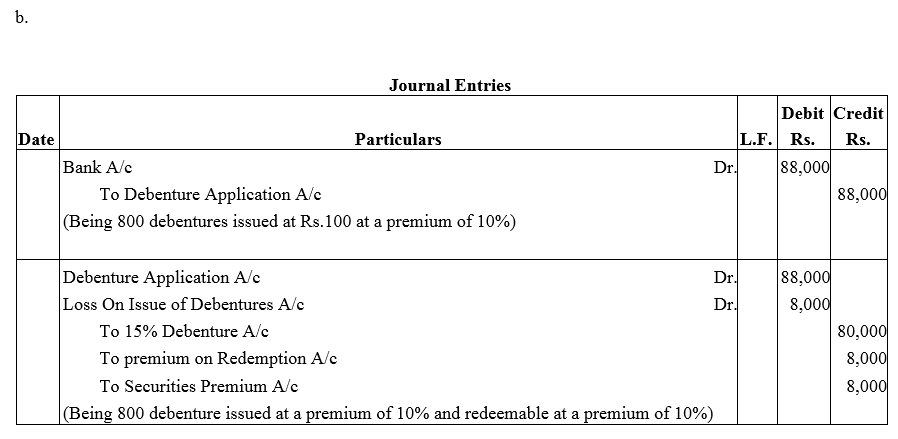

Record necessary Journal entries at the time of issue of 10% Debentures.

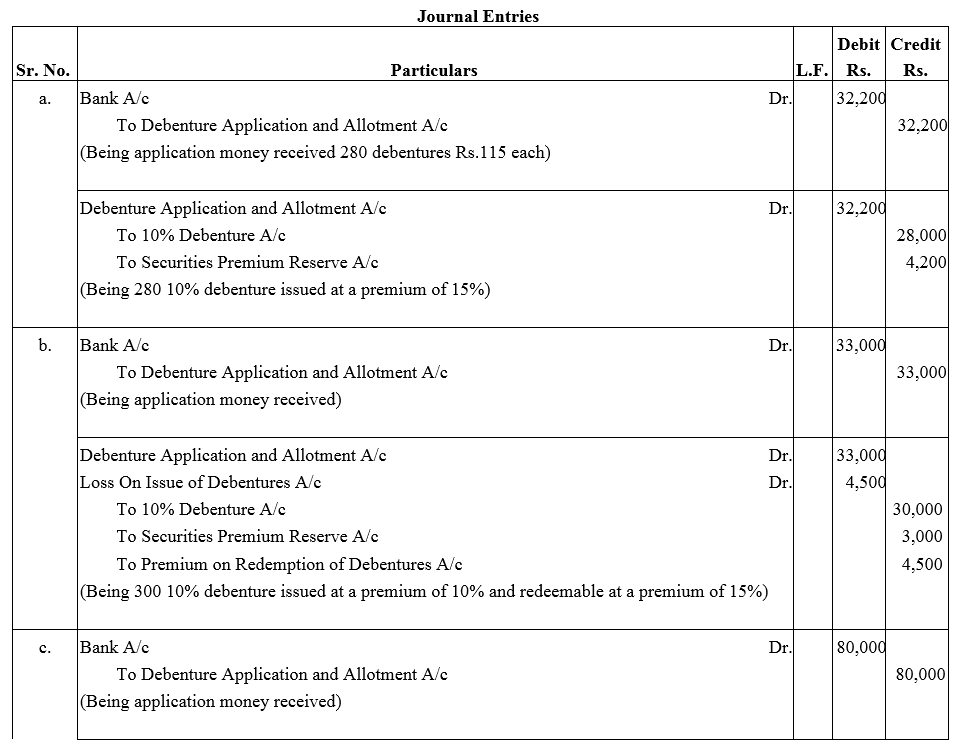

Solution:

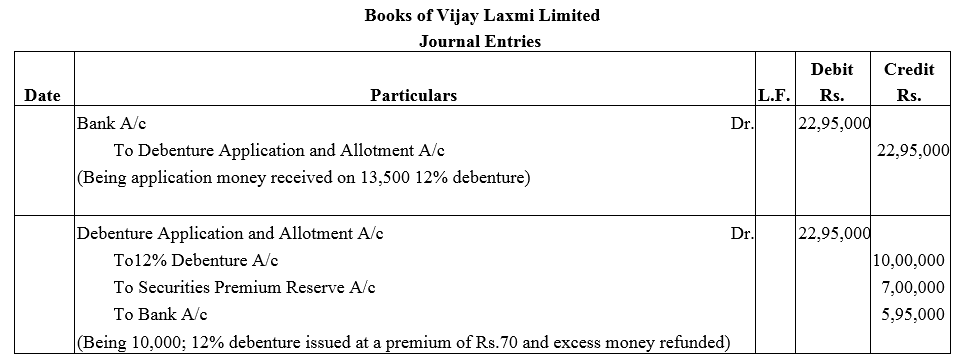

Question 8.

Vijay Laxmi Ltd. invited applications for 10,000; 12% Debentures of ₹ 100 each at a premium of ₹ 70 per debenture. The full amount was payable on application.

Applications were received for 13,500 debentures. Applications for 3,500 debentures were rejected and application money was refunded. Debentures were allotted to the remaining applications.

Solution:

Question 9.

Iron Products Ltd. issued 5,000; 9% Debentures of ₹ 100 each at a premium of ₹ 40 payable as follows:

(i) ₹ 40, including premium of ₹ 10 on applications;

(ii) ₹ 45, including premium of ₹ 15 on allotment and

(iii) Balance as first and final call.

The issue was subscribed and allotment made. Calls were made and due amount was received.

Pass Journal entries.

Solution:

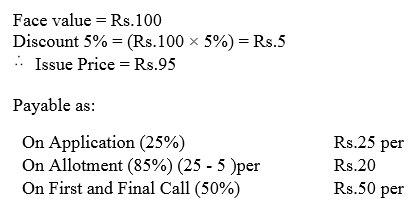

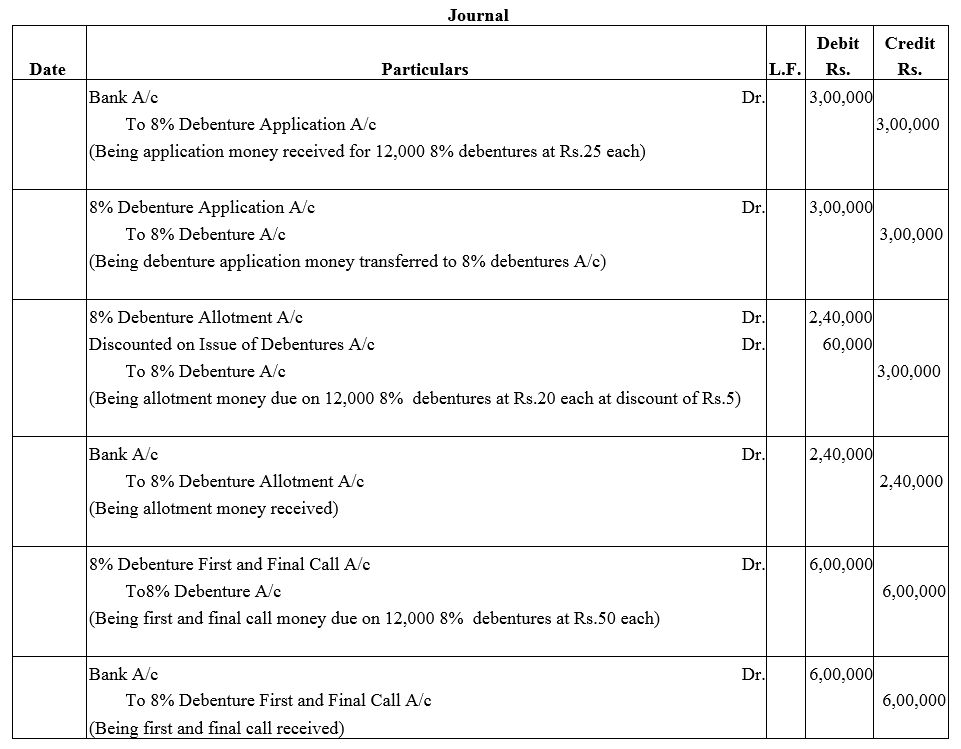

Question 10.

X Ltd. issued 12,000; 8% Debentures of ₹ 100 each at a discount of 5% payable as 25% on application; 20% on allotment and balance after three months. Pass Journal entries.

Solution:

Question 11.

Alka Ltd. issued 5,000, 10% Debentures of ₹ 1,000 each at a discount of 10% redeemable at a premium of 5% after 5 years. According to the terms of issue ₹ 500 was payable on application and the balance amount on allotment of debentures. Record necessary entries regarding issue of 10% Debentures.

Solution:

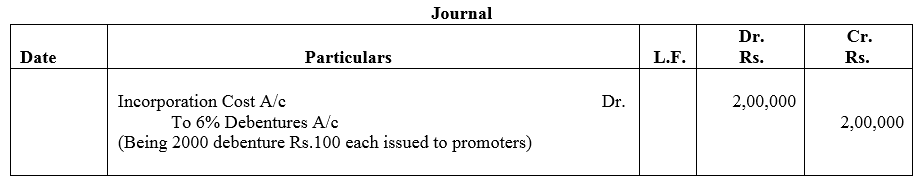

Question 12.

Amrit Ltd. was promoted by Amrit and Bhaskar with an authorised capital of ₹ 10,00,000 divide into 1,00,000 shares of ₹ 10 each.

The company decided to issue 1,000, 6% Debentures of ₹ 100 each to Amrit and Bhaskar each for their services in incorporating the company. Pass journal entry.

Solution:

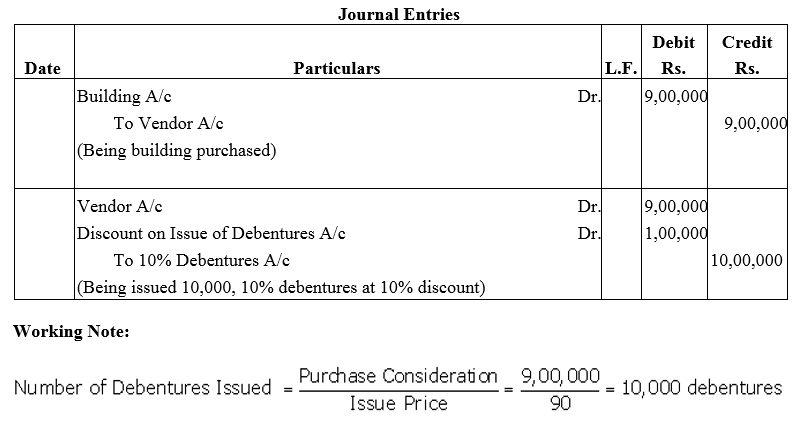

Question 13.

A limited company bought a Building for ₹ 9,00,000 and the consideration was paid by issuing 10% Debentures of the normal (face) value of ₹ 100 each at a discount of 10%. Give journal entries.

Solution:

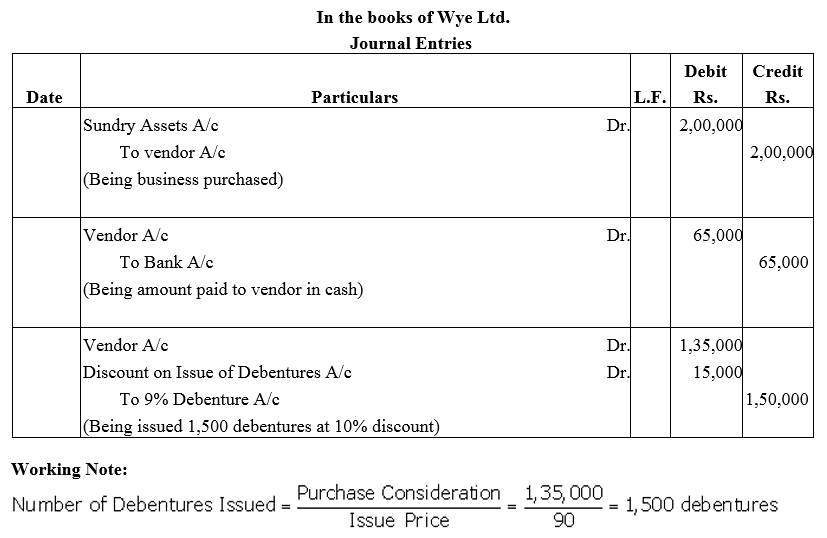

Question 14.

Wye Ltd. purchased an established business for ₹ 2,00,000 payable as ₹ 65,000 by cheque and the balance by issuing 9% Debentures of ₹ 100 each at a discount of 10%.

Give journal entries in the books of Wye Ltd.

Solution:

Question 15.

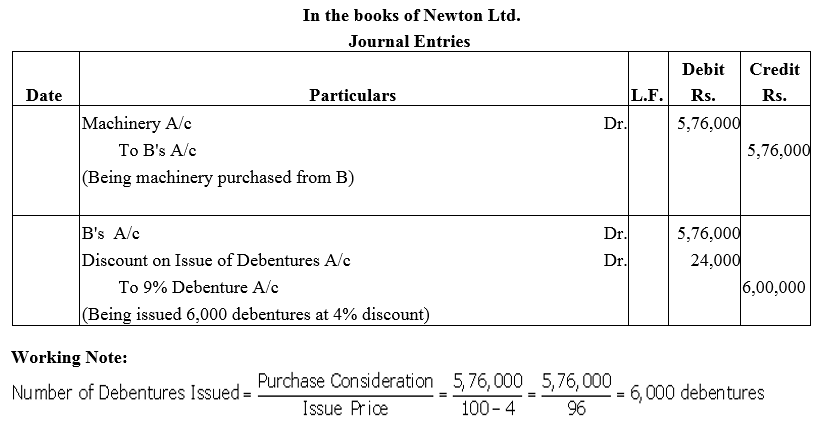

Newton Ltd. purchased a Machinery from B for ₹ 5,76,000 to be paid by the issue of 9% Debentures of ₹ 100 each at 4% discount. Journalise the trasactions.

Solution:

Question 16.

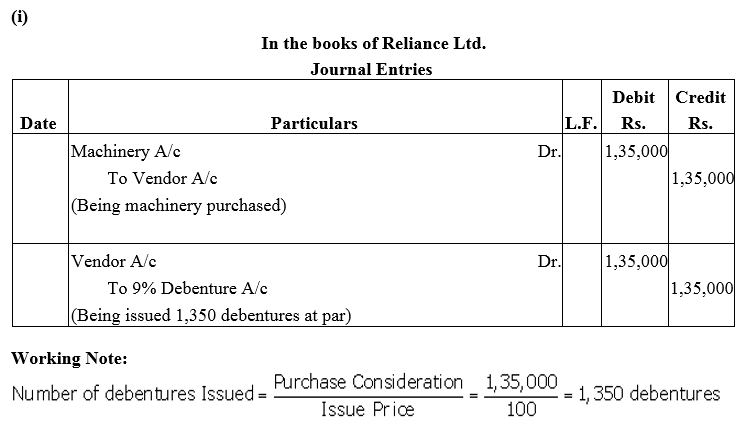

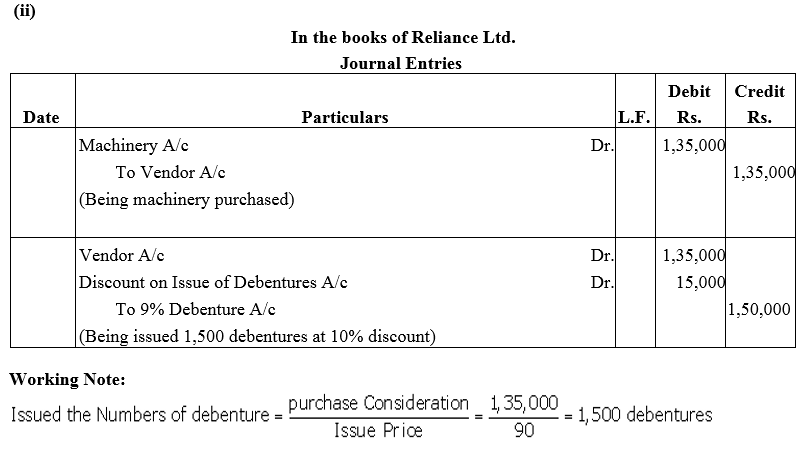

Reliance Ltd. purchased machinery costing ₹ 1,35,000. It was agreed that the purchase consideration be paid by issuing 9% Debentures of ₹ 100 each. Assume debentures have been issued

(i) at par and

(ii) at a discount of 10%.

Give necessary journal entries.

Solution:

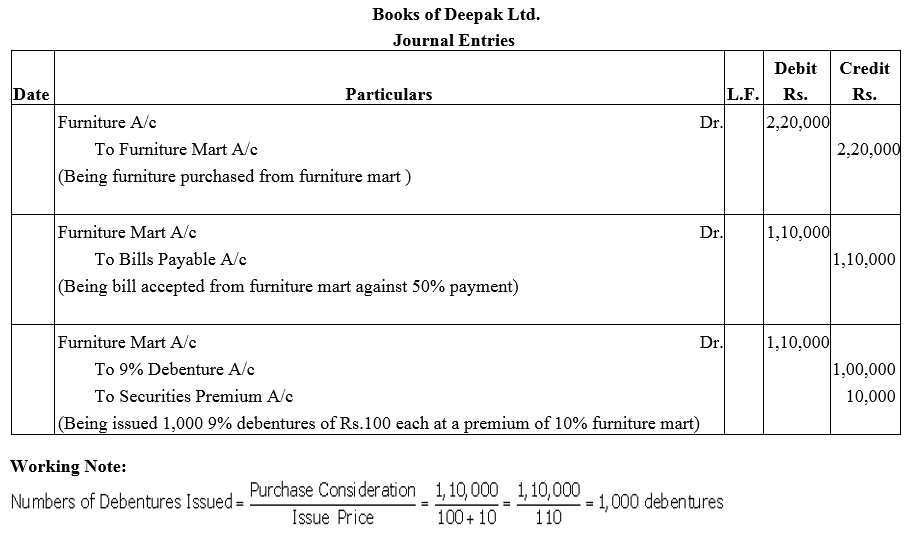

Question 17.

Deepak Ltd purchased furniture of ₹ 2,20,000 from M/s. Furniture Mart. 50% of the amount was paid to M/s. Furniture Mart by accepting a Bill of Exchanged and for the balance the company issued 9% Debenture of ₹ 100 each at a premium of 10% in favour of M/s. Furniture Mart.

Pass Journal entries in the books of Deepak Ltd.

Solution:

Question 18.

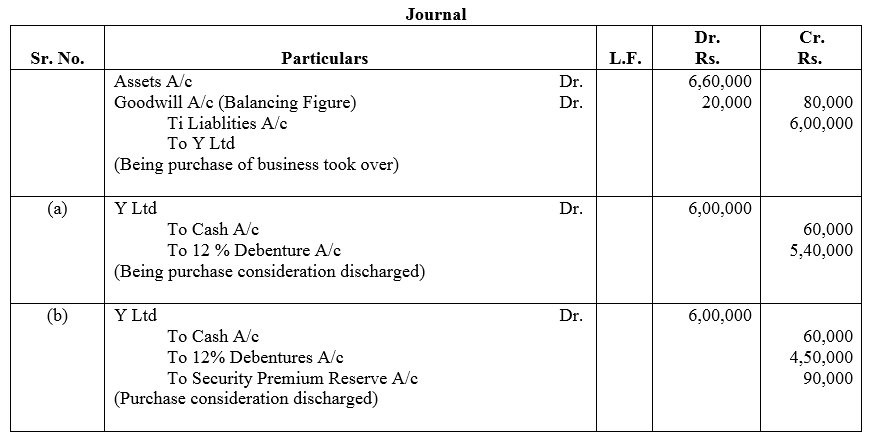

X Ltd. took over the assets of ₹ 6,00,000 and liabilities of ₹ 80,000 of Y Ltd for an agreed purchase consideration of ₹ 6,00,000 payable 10% in cash and the balance by the issue of 12% Debentures of ₹ 100 each. Give necessary journal entries in the books of X Ltd., assuming that:

Case (a): The debentures are issued at par.

Case (b): The debentures are issued at 20% premium.

Case (c): The debentures are issued at 10% discount.

Solution:

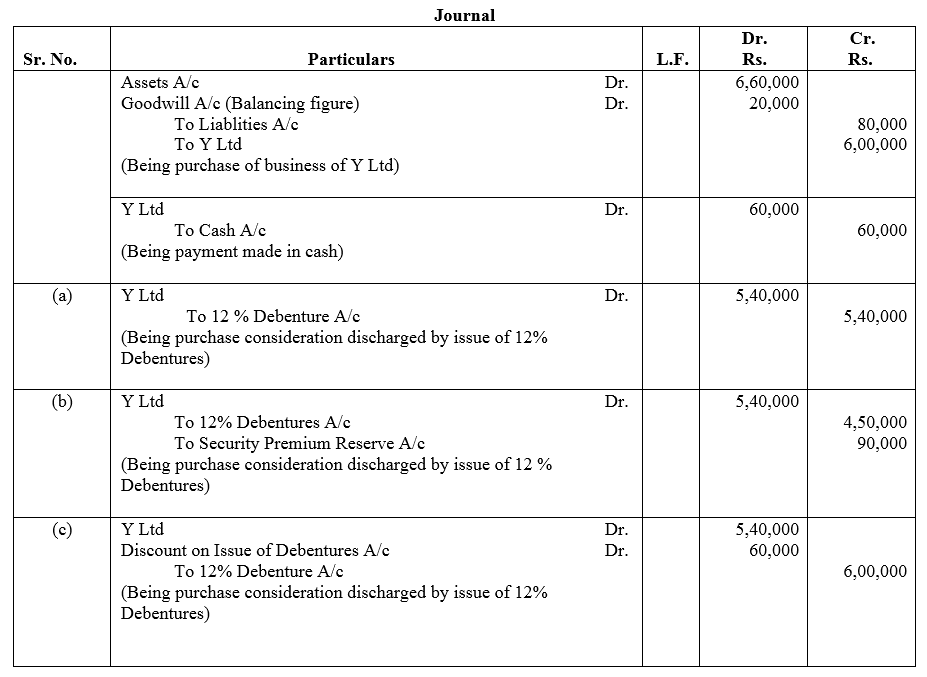

Question 19.

X Ltd. took over the assets of ₹ 6,60,000 and liabilities of ₹ 80,000 of Y Ltd. for ₹ 6,00,000. Give necessary journal entries in the books of X Ltd. assuming that:

Case (a): The purchase consideration was payable 10% in cash and the balance in 5,400; 12% Debentures of ₹ 100 each.

Case (b): The purchase consideration was payable 10% in cash and the balance in 4,500; 12% Debentures of ₹ 100 each issued at 20% premium.

Solution:

Question 20.

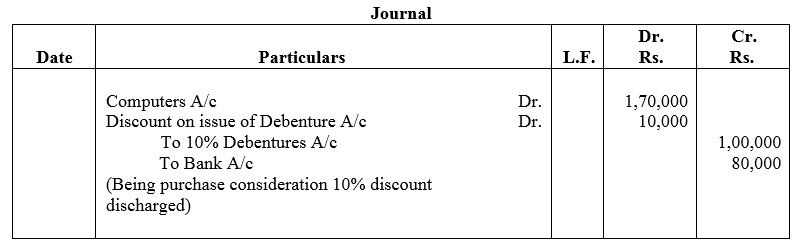

Perfect Barcode Ltd. purchased computers from M/s. Computer Mart and paid the consideration as follows:

(a) 1,000, 10% Debentures of ₹ 100 each at a discount of 10% ; and

(b) Issued a cheque for ₹ 80,000 for the balance amount.

Pass the journal entry in the books of Perfect Barcode Ltd.

Solution:

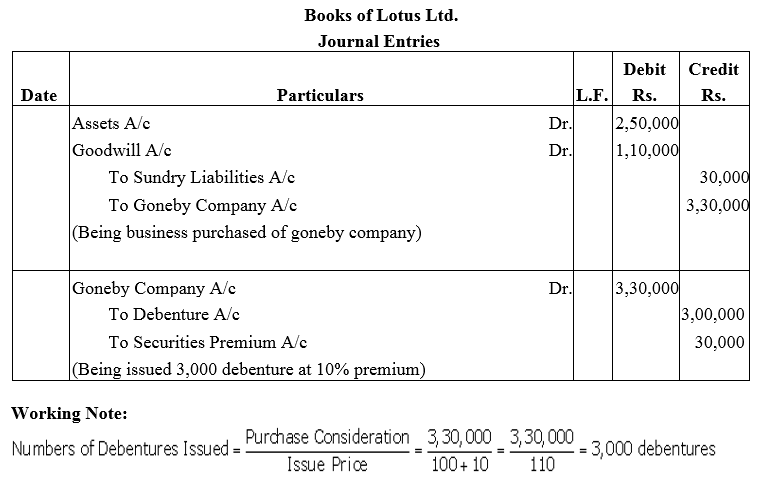

Question 21.

Lotus Ltd. took over assets of ₹ 2,50,000 and liabilities of ₹ 30,000 of Goneby Company for the purchase consideration of ₹ 3,30,000. Lotus Ltd. paid the purchase consideration by issuing debentures of ₹ 100 each at 10% premium.

Give journal entries in the books of Lotus Ltd.

Solution:

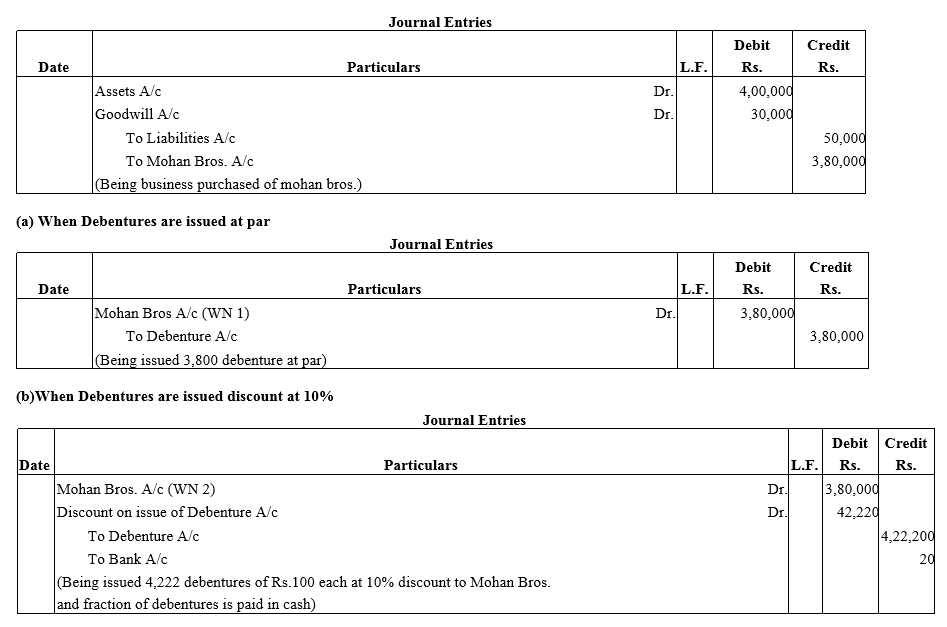

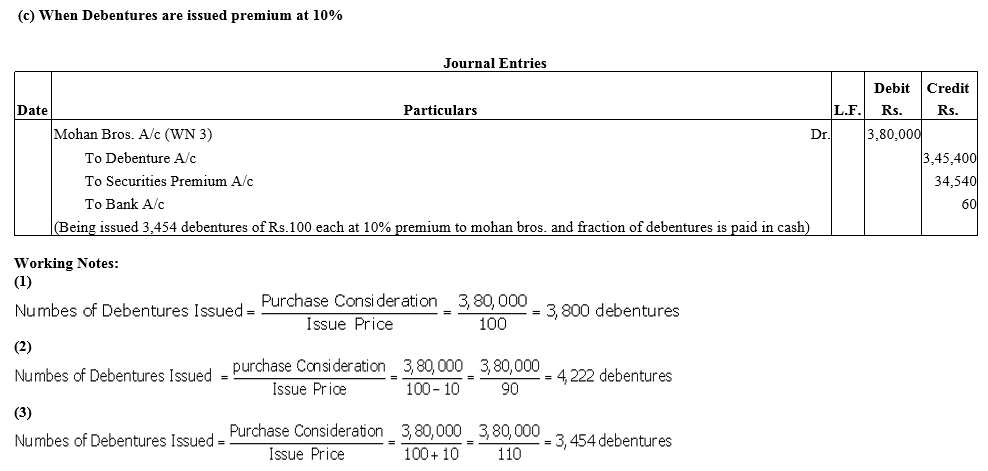

Question 22.

Exe Ltd. purchased the assets of the book value ₹4,00,000 and took over the liabilities of ₹ 50,000 from Mohan Bros.It was agreed that the purchase consideration, settled at ₹ 3,80,000 be paid by issuing debentures of ₹ 100 each.

Pass journal entries if debenture are issued:

(a) at par

(b) at a discount of 10% and

(c) at a premium of 10%.

It was agreed that any fraction of debentures be paid in cash.

Solution:

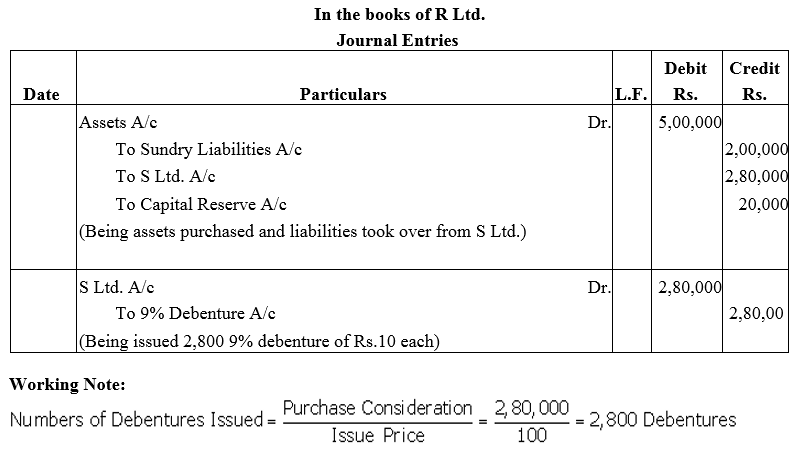

Question 23.

R Ltd. purchased the assets of S Ltd. for ₹ 5,00,000. It also agreed to take over the liabilities of S Ltd. amounted to ₹ 2,00,000 for a purchase consideration of ₹ 2,80,000. The payment of S Ltd. was made by issue of 9% Debentures of ₹ 100 each at par.

Pass necessary journal entries in the books of R Ltd.

Solution:

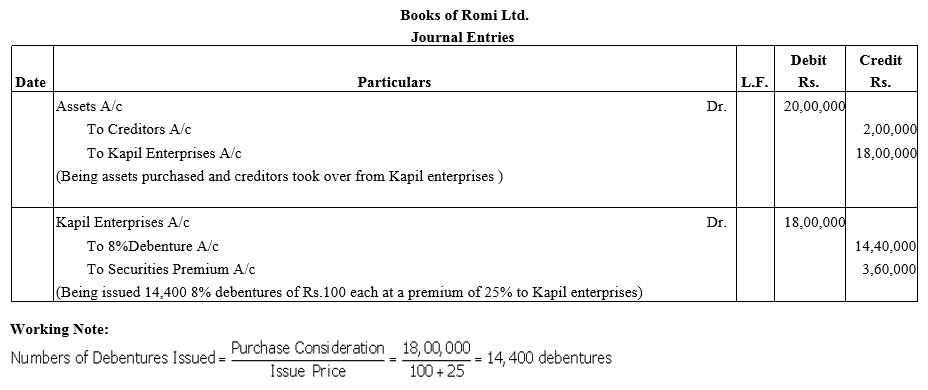

Question 24.

Romi Ltd. acquired assets of ₹ 20 lakhs and took over creditors of ₹ 2 lakhs from Kapil Enterprises.

Romi Ltd. issued 8% Debentures of ₹ 100 each at a discount of 25% as purchase consideration.

Record necessary journal entries in the books of Romi Ltd.

Solution:

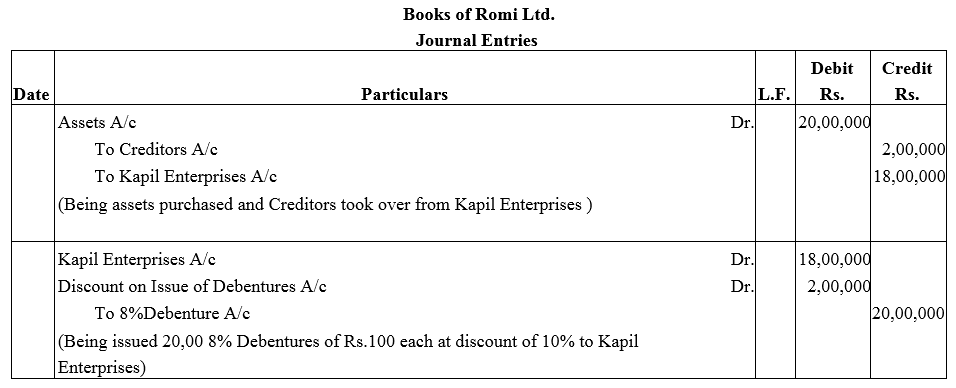

Question 25.

Romi Ltd. acquired assets of ₹ 20 lakhs and took over creditors of ₹ 2 lakhs from Kapil Enterprises.

Romi Ltd. issued 8% Debentures of ₹ 100 each at a discount of 10% as purchase consideration.

Record necessary journal entries in the books of Romi Ltd.

Solution:

Question 26.

X Ltd. issued 10% Debentures of nominal value of ₹ 10,00,000 as follows:

(i) To sundry persons for cash at par ₹ 5,00,000 nominal.

(ii) To a vendor for ₹ 5,50,000 for purchase of fixed assets ₹ 5,00,000 nominal.

Pass journal entries in the books of X Ltd.

Solution:

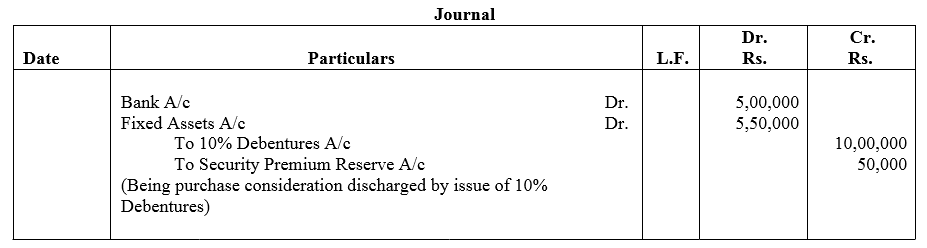

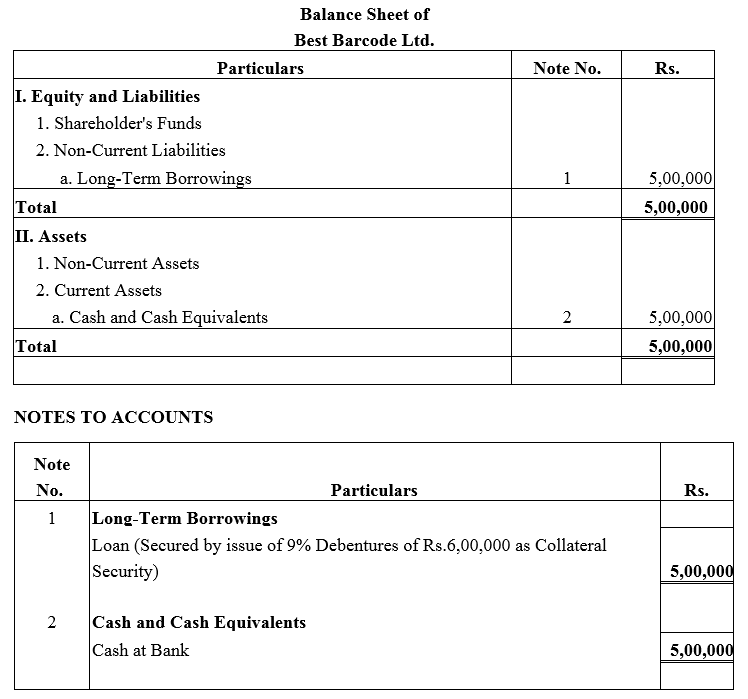

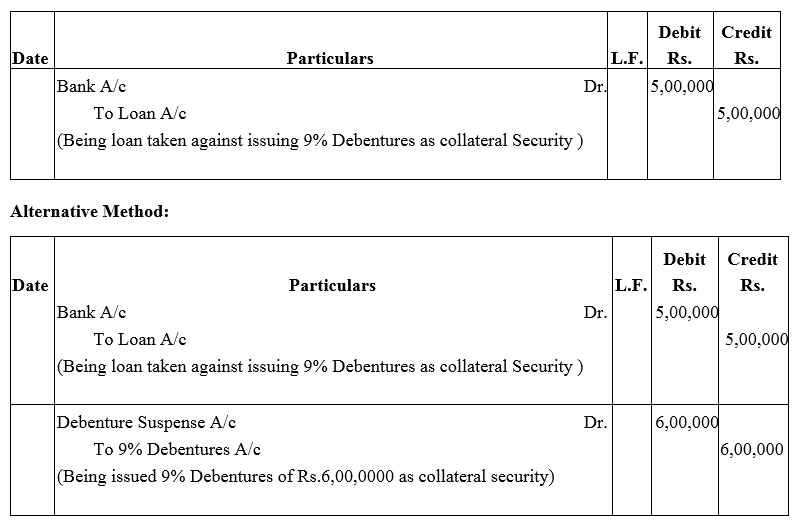

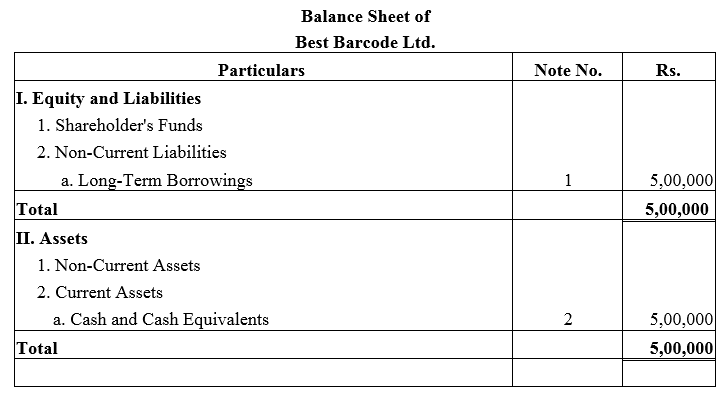

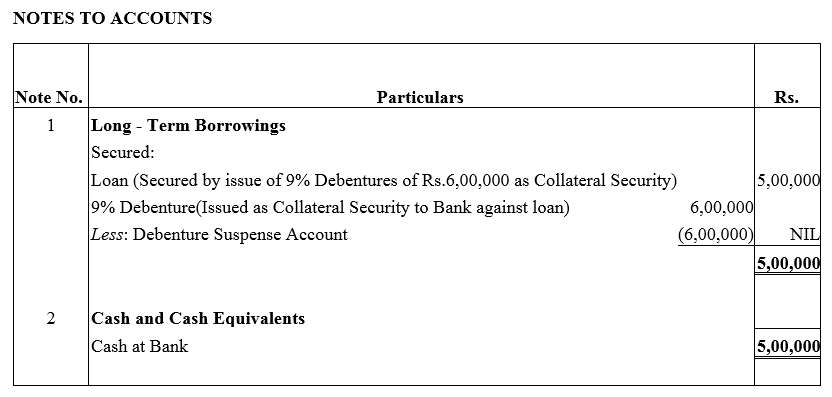

Question 27.

Best Barcode Ltd. took a loan of ₹ 5,00,000 from a bank giving ₹ 6,00,000; 9% Debentures as collateral security. Pass journal entries regarding issue of debentures, if any, and show this loan in the Balance Sheet of the company.

Solution:

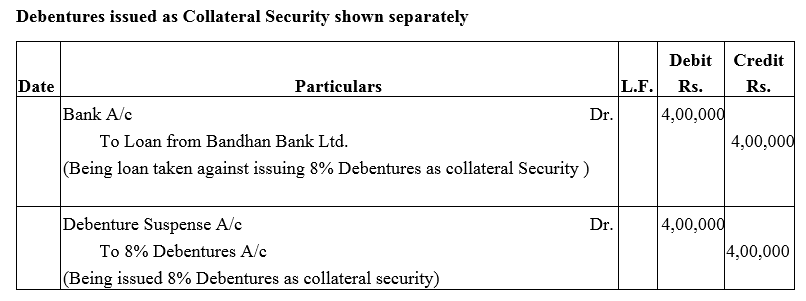

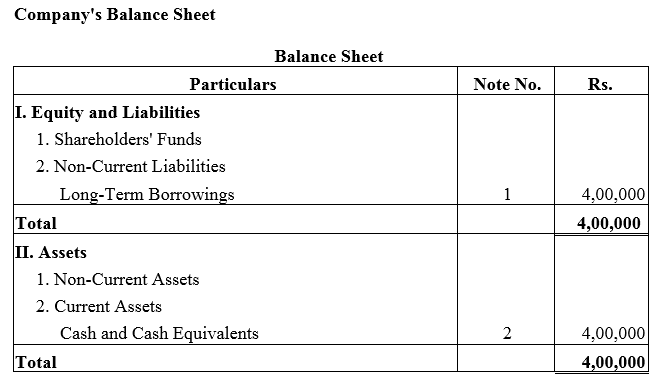

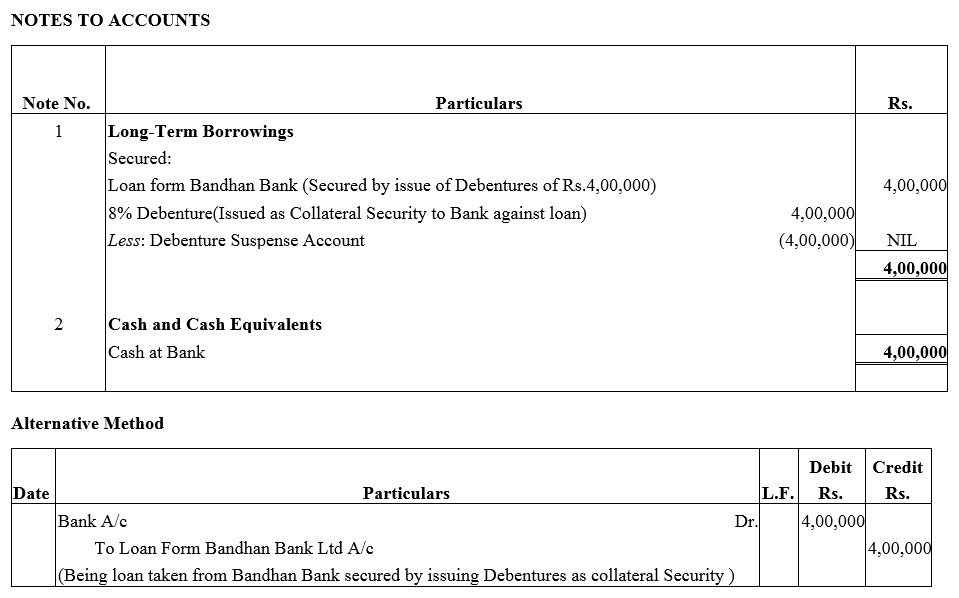

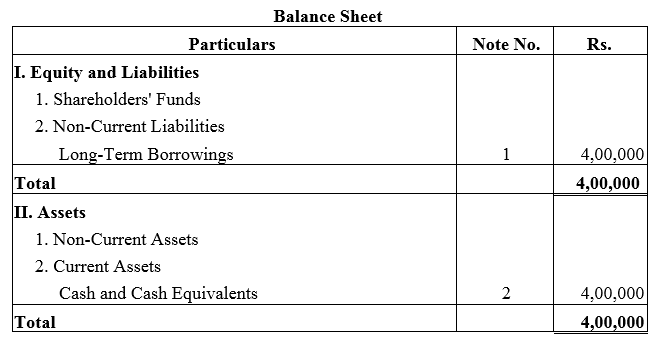

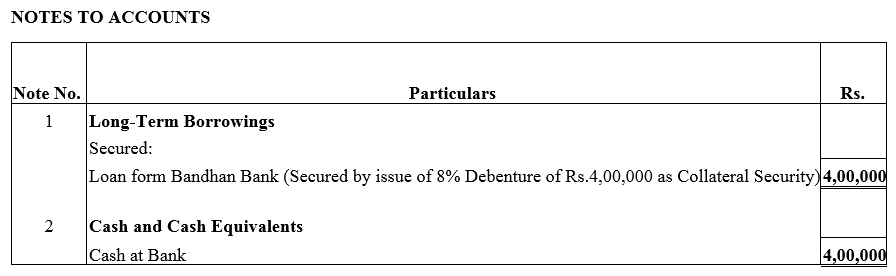

Question 28.

A company took a loan of ₹ 4,00,000 from Bandhan Bank Ltd. and issued 8% Debentures of ₹ 4,00,000 as a collateral security.

Solution:

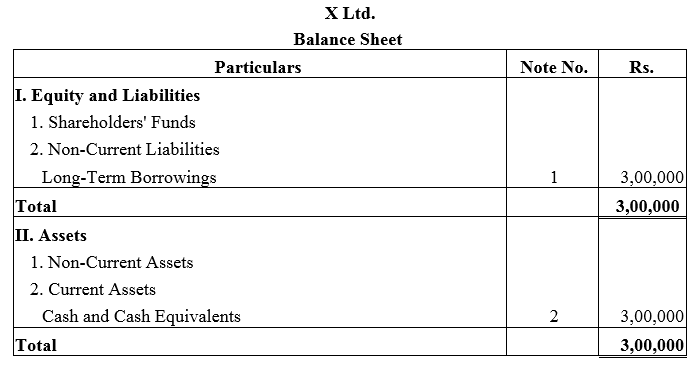

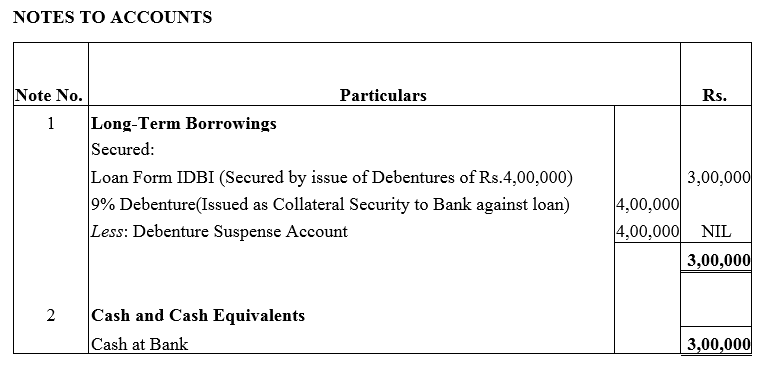

Question 29.

X Ltd. took a loan of ₹ 3,00,000 from IDBI Bank. The company issued 4,000; 9% Debentures of ₹ 100 each as a collateral security for the same. Show how these items will be presented in the Balance Sheet of the company.

Solution:

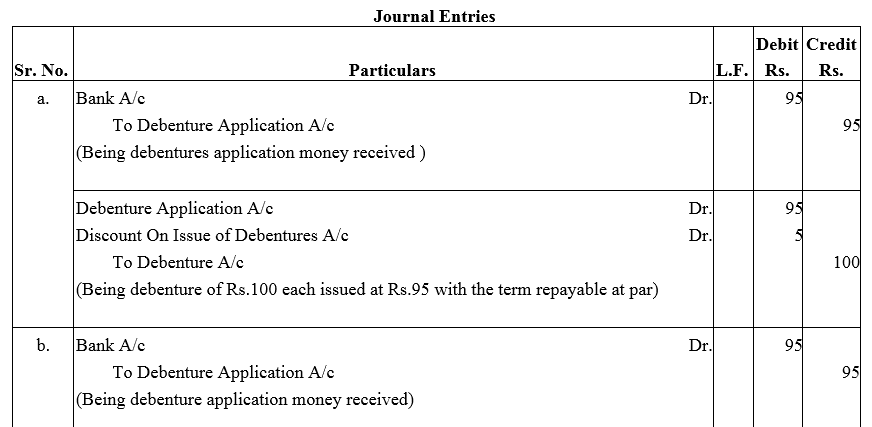

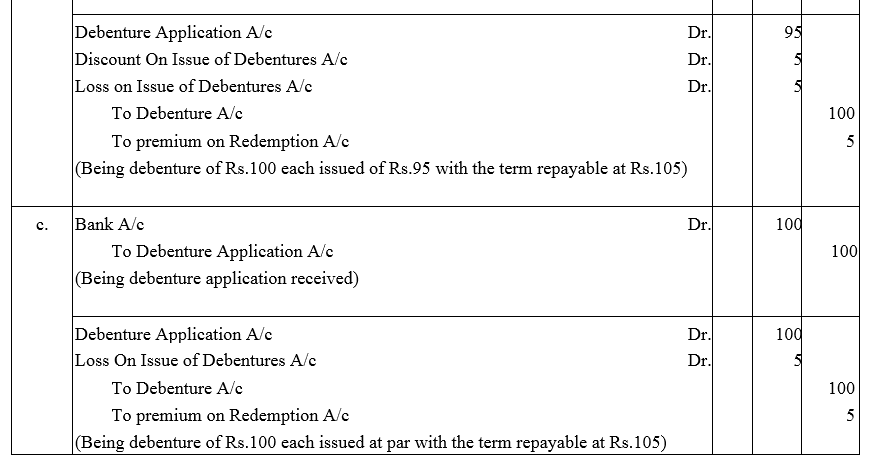

Question 30.

Journalise the following:

(a) A debenture issued at ₹ 95, repayable at ₹ 100.

(b) A debenture issued at ₹ 95, repayable at ₹ 105.

(c) A debenture issued at ₹95, repayable at ₹ 105.

The face value of debenture is ₹ 100 in each of the above cases.

Solution:

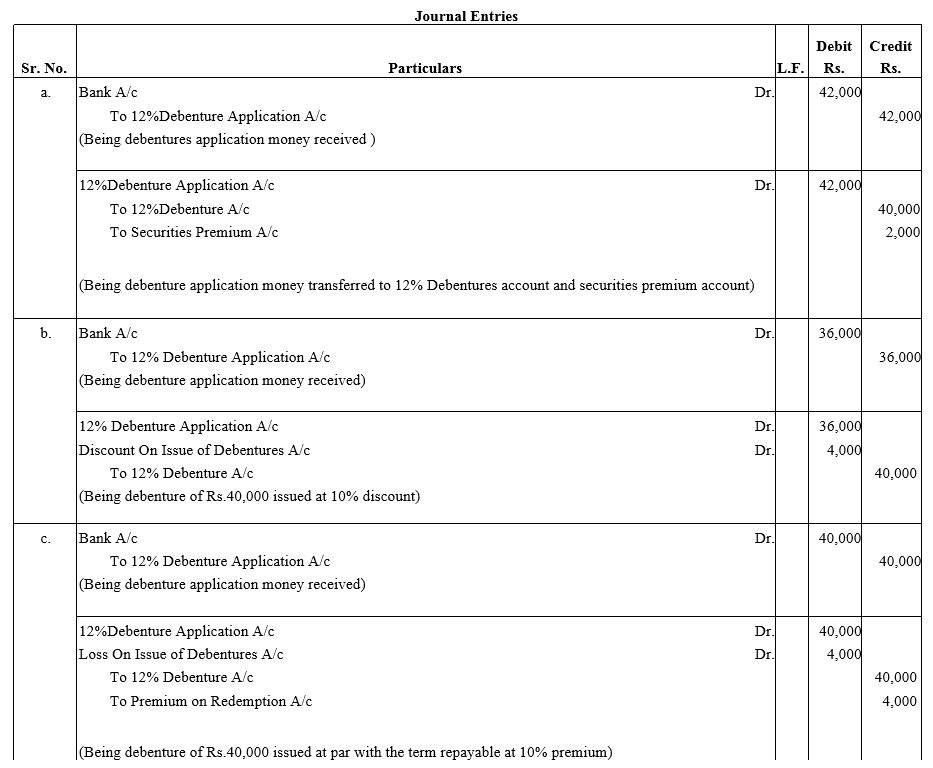

Question 31.

Pass journal entries in the following cases:

(a) A Co.Ltd. issued ₹ 40,000; 12% Debentures at a premium of 5% redeemable at par.

(b) A Co.Ltd. issued ₹ 40,000; 12% Debentures at a discount of 10% redeemable at par.

(c) A Co.Ltd. issued ₹ 40,000; 12% Debentures at par redeemable at 10% premium.

(d) A Co.Ltd. issued ₹ 40,000; 12% Debentures at a discount of 5% and redeemable at 5% premium.

(e) A Co.Ltd. issued ₹ 40,000; 12% Debentures at a premium of 10% redeemable at 110%.

Solution:

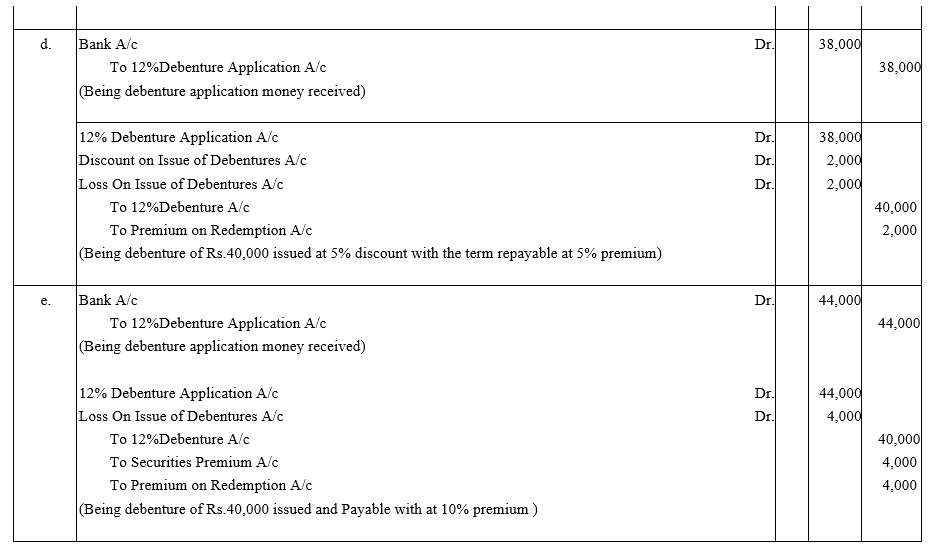

Question 32.

Footfall Ltd.issues 10,000 Debentures of Pass necessary journal entries relating to the issue of Debentures for the following:

(a) Issued ₹ 28,000; 10% Debentures of ₹ 100 each at a premium of 15% redeemable at par.

(b) Issued ₹ 30,000; 10% Debentures of ₹ 100 each at a premium of 10% and redeemable at a premium of 15%.

(c) Issued ₹ 80,000; 10% Debentures of ₹ 100 each at par repayable at a premium of 10%. 100 each at a discount of 10% redeemable at a premium of 5% after the expiry of three years.

Pass journal entries for the issue of these debentures.

Solution:

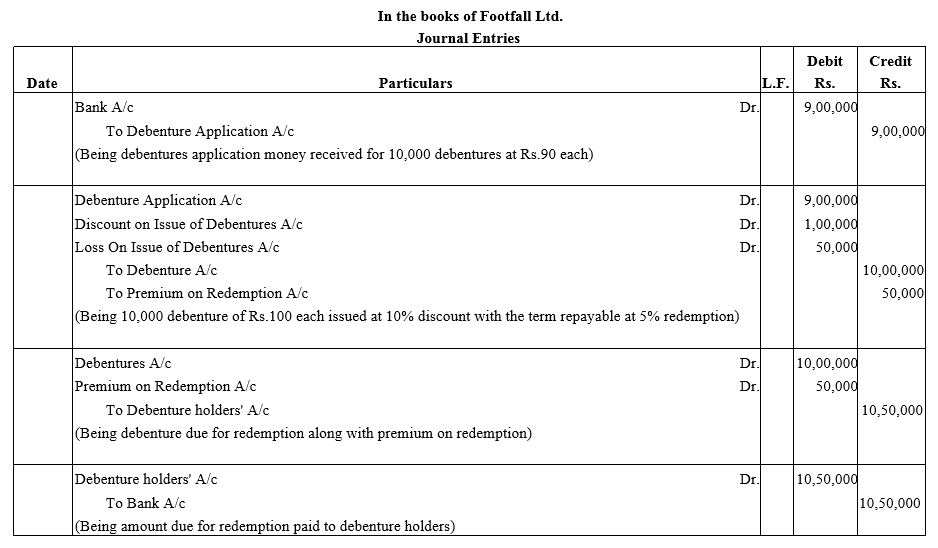

Question 33.

Pass necessary journal entries relating to the issue of Debentures for the following:

(a) Issued ₹ 4,00,000; 9% Debentures of ₹ 100 each at a premium of 8% redeemable at 10% premium.

(b) Issued ₹ 6,00,000; 9% Debentures of ₹ 100 each at par, repayable at a premium of 10%.

(c) Issued ₹ 10,00,000; 9% Debentures of ₹ 100 each at a premium of 5%,redeemable at par.

Solution:

Question 34.

Pass necessary journal entries relating to the issue of Debentures for the following:

(a) Issued ₹ 28,000; 10% Debentures of ₹ 100 each at a premium of 15% redeemable at par.

(b) Issued ₹ 30,000; 10% Debentures of ₹ 100 each at a premium of 10% and redeemable at a premium of 15%.

(c) Issued ₹ 80,000; 10% Debentures of ₹ 100 each at par repayable at a premium of 10%.

Solution:

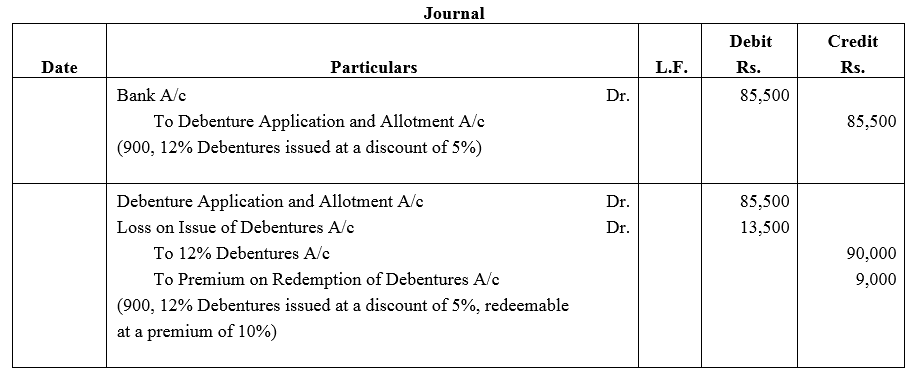

Question 35.

Journalise the following transaction at the time of issue of 12% Debentures:

Nandan Ltd. issued ₹ 90,000, 12% Debentures of ₹ 100 each at a discount of 5% redeemable at 110%.

Solution:

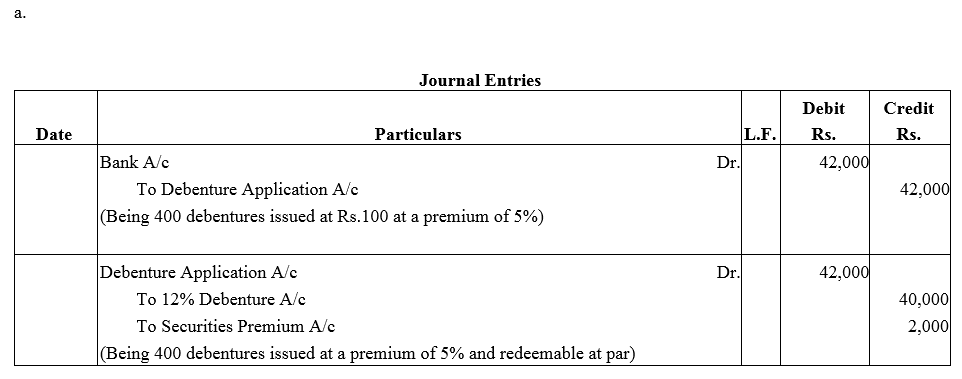

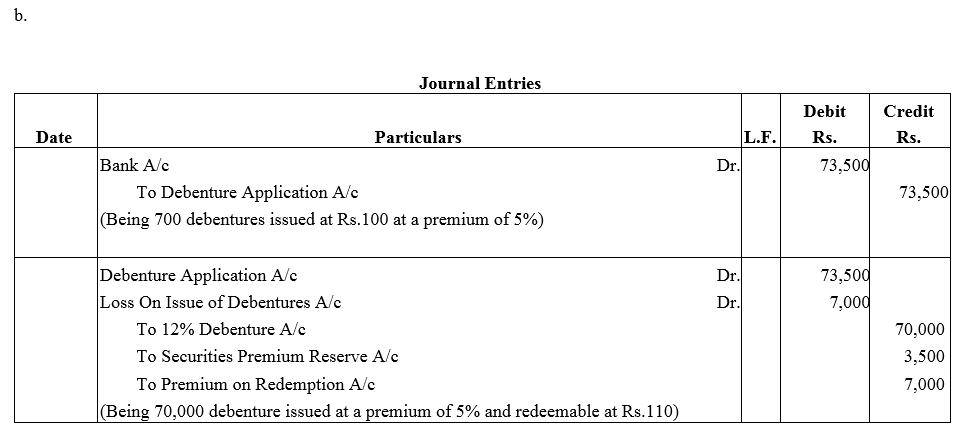

Question 36.

Pass necessary journal entries for the issue of Debentures in the following cases:

(a) ₹ 40,000; 12% Debentures of ₹ 100 each issued at a premium of 5% redeemable at par.

(b) ₹ 70,000; 12% Debentures of ₹ 100 each issued at a premium of 5% redeemable at a premium of 110.

Solution:

Question 37.

Pass necessary journal entries for the issue of Debentures in the following cases:

(a) ₹ 40,000; 15% Debentures of ₹ 100 each issued at a discount of 10% redeemable at par.

(b) ₹ 80,000; 15% Debentures of ₹ 100 each issued at a premium of 10% redeemable at a premium of 10%.

Solution:

Question 38.

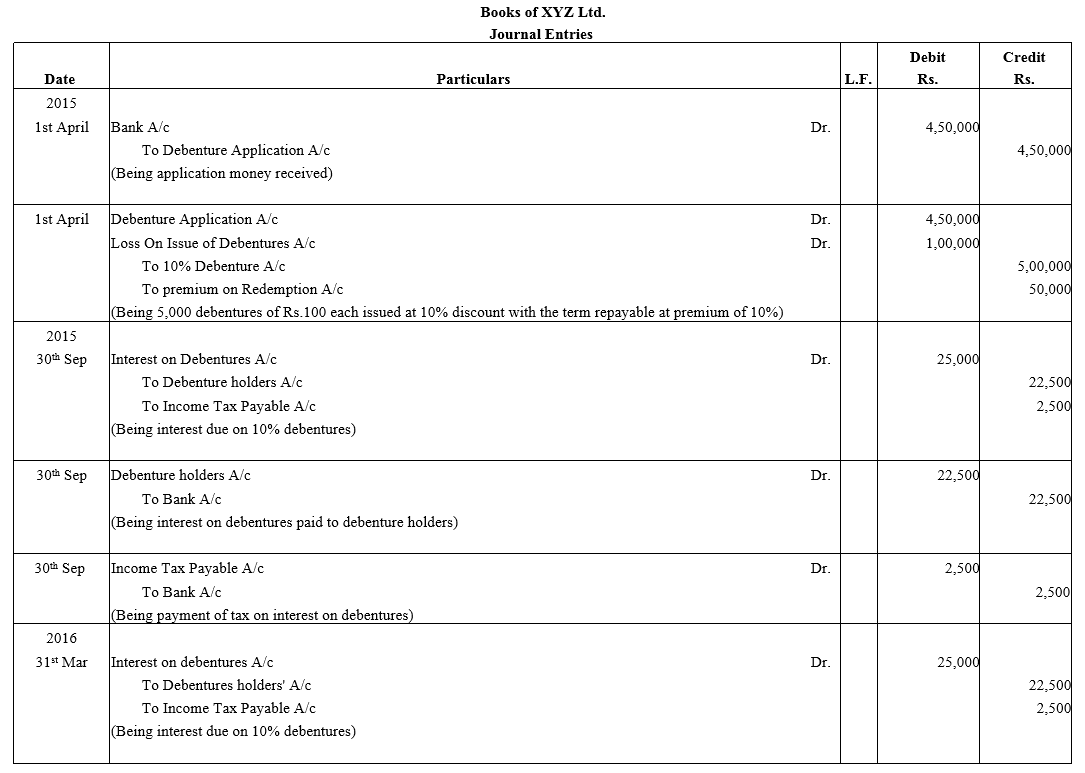

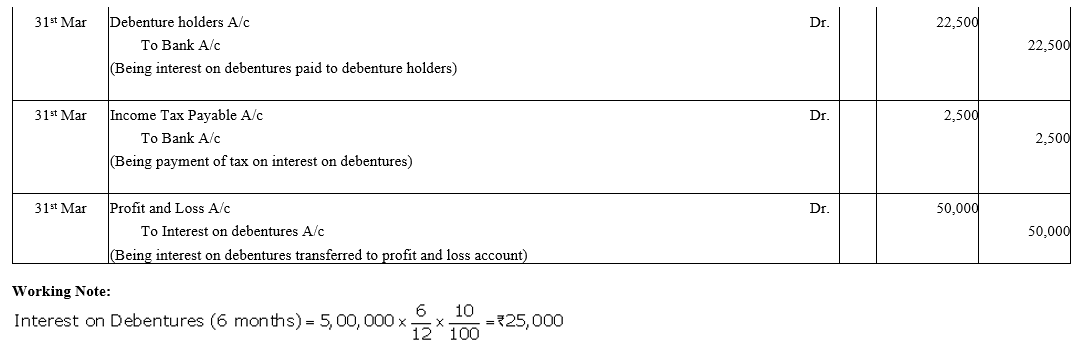

XYZ Ltd.issued 5,000, 10% Debentures of ₹ 100 each on 1st April, 2015 at a discount of 10% redeemable at a premium of 10% after 4 years. Give journal entries for the year ended 31st March, 2016, assuming that the interest was payable half-yearly on 30th September and 31st March. Tax is to be deducted @ 10%.

Solution:

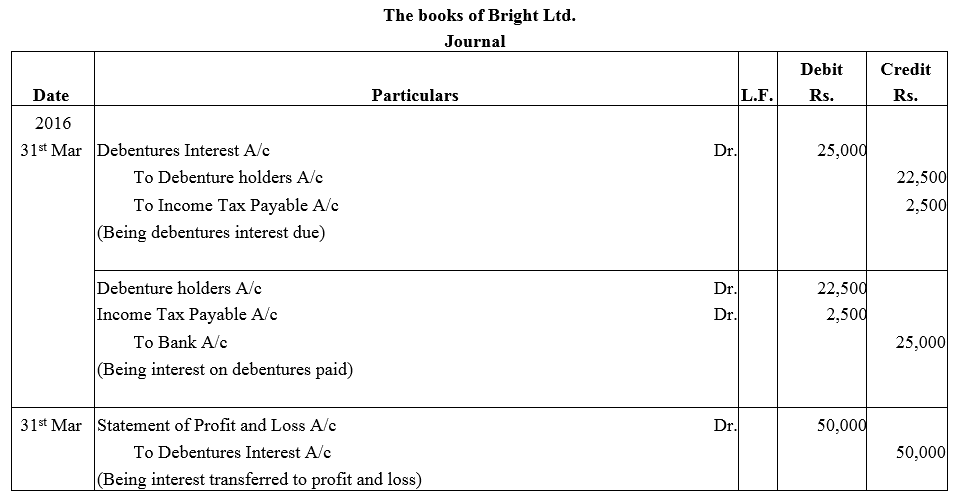

Question 39.

Bright Ltd. issued 5,000; 10% Debentures of ₹ 100 each on 1st April, 2015. The issue was fully subscribed. According to the terms of issue, interest on the debentures is payable half-yearly on 30th September and 31st March and the tax deducted at source is 10%.

Pass necessary journal entries related to the debenture interest for the year ending 31st March, 2016 and transfer of interest on debentures of the year to the Statement of Profit and Loss.

Solution:

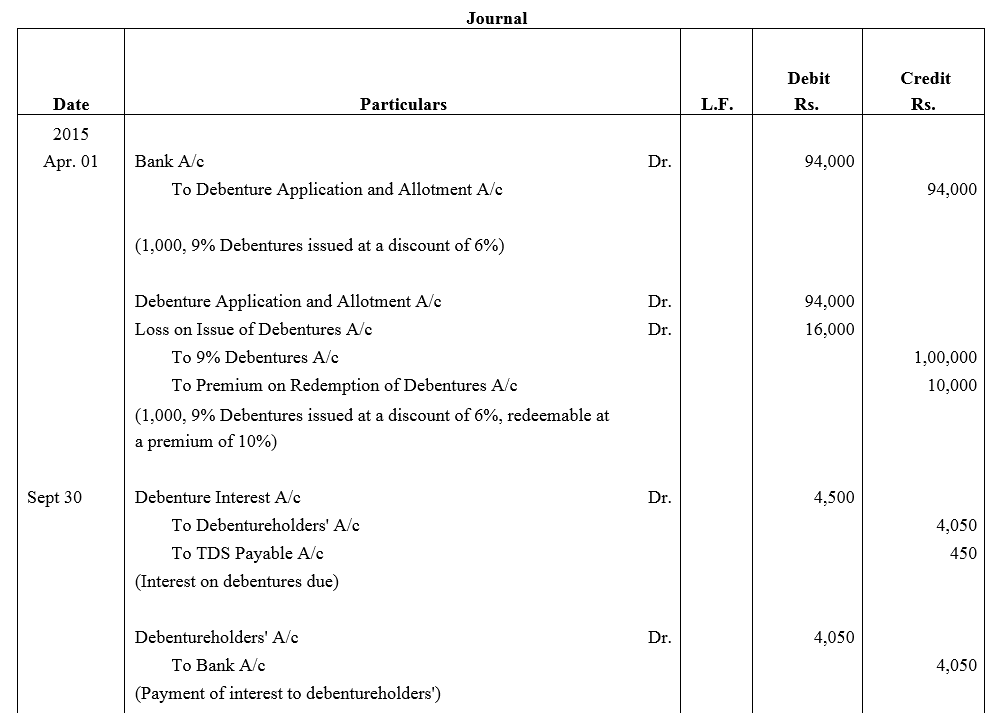

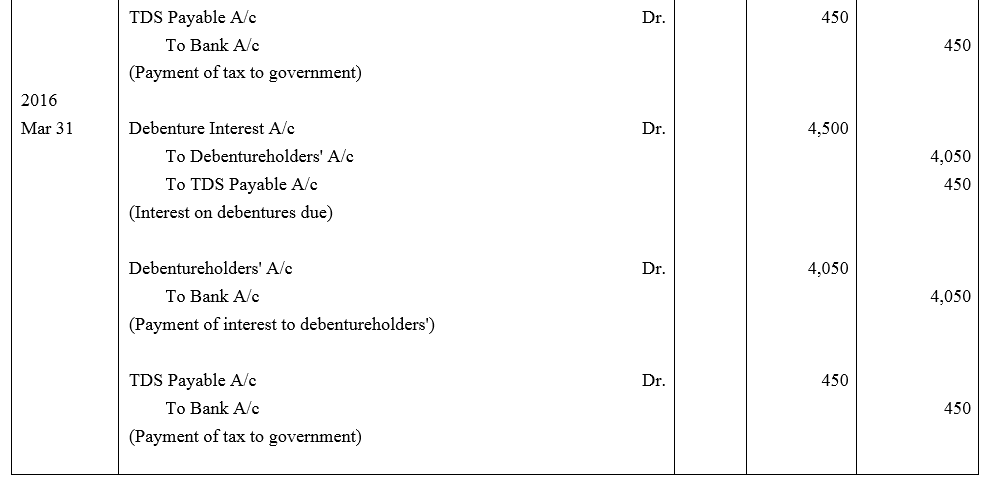

Question 40.

On 1st April, 2015, V.V.L. Ltd issued 1,000, 9% Debentures of ₹ 100 each at a discount of 6%, redeemable at a premium of 10% after three years. Pass necessary journal entries for the issue of debentures and debenture interest for the year ended 31st March, 2016, assuming that interest is payable on 30th September and 31st March and the rate of tax deducted at source is 10%. The company closes its books on 31st March every year.

Solution:

Question 41.

X Ltd. issued 30,000, 10% Debentures of ₹ 100 each at a discount of 5% on 1st April, 2015. As per the terms of issue, debentures are to be redeemed at the end of five years. Show the amount of discount to be written off from Statement of Profit and Loss every year.

Solution:

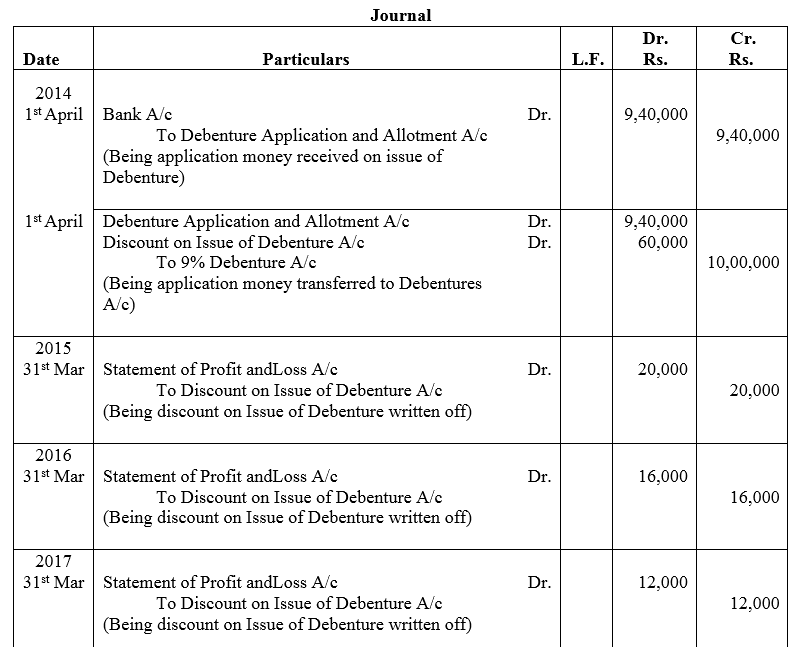

Question 42.

A limited company issued ₹ 10,00,000; 9% Debentures at a discount of 6% on 1st April, 2014. These debentures are to be redeemed equally, in 5 annual installments starting from 31st March, 2015. Discount on Issue of Debentures is written off during the tenure of debentures.

Pass the journal entries for issue of debentures and writing off the discount.

Solution:

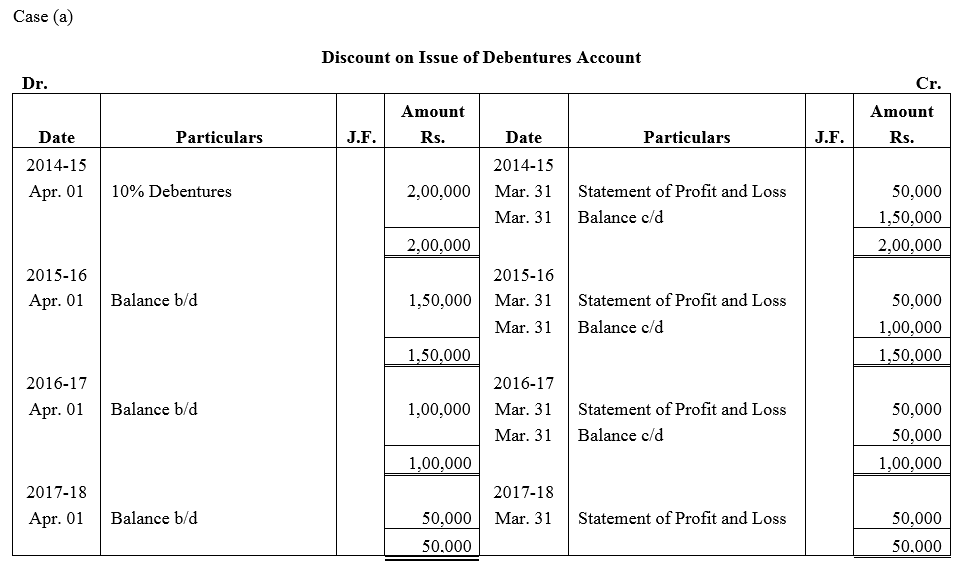

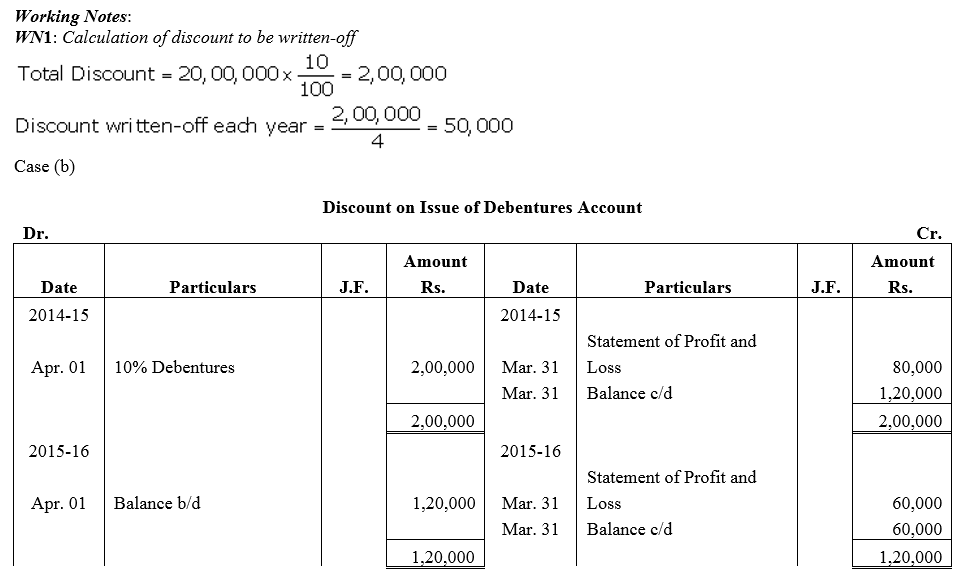

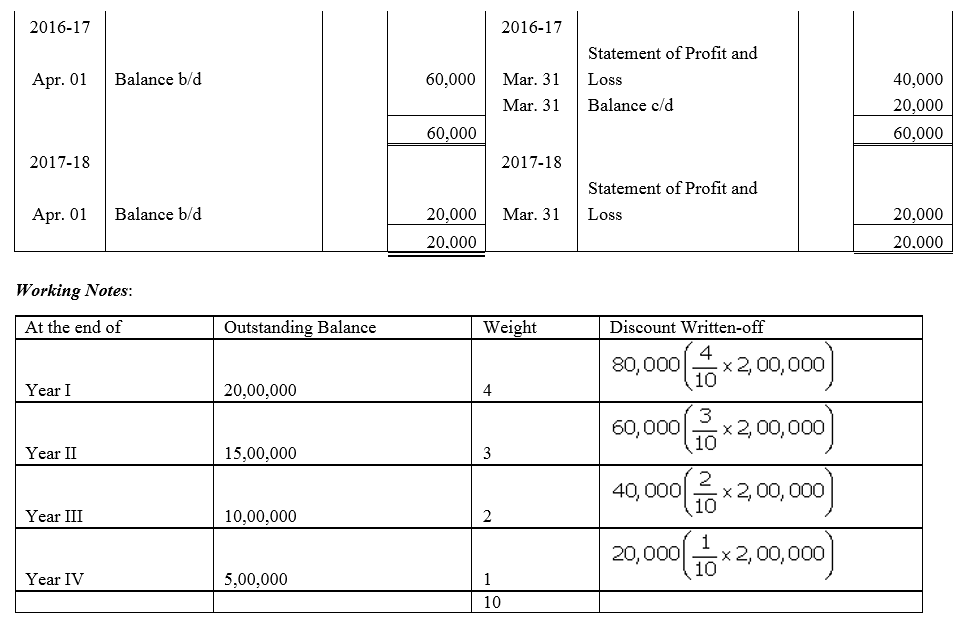

Question 43.

On 1st April, 2014, Popular Ltd. issued 20,000; 10% Debentures of ₹ 100 each at a discount of 10% redeemable at par. Show the Discount on Issue of Debentures Account if

(a) such debentures are redeemable after 4 years, and

(b) such debentures are redeemable by equal annual drawings in 4 years, starting from 31st March, 2015. Popular Ltd. follows financial year as its accounting year.

Solution:

Question 44.

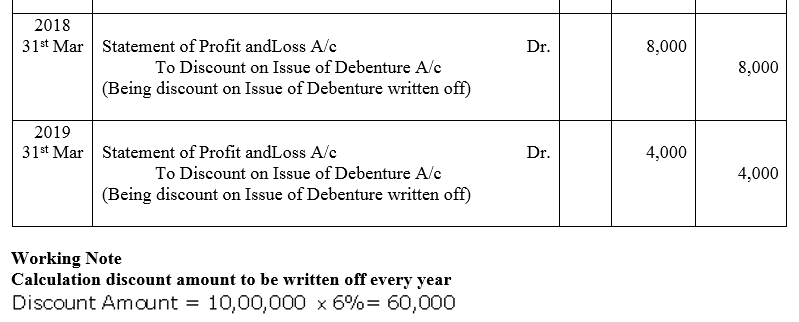

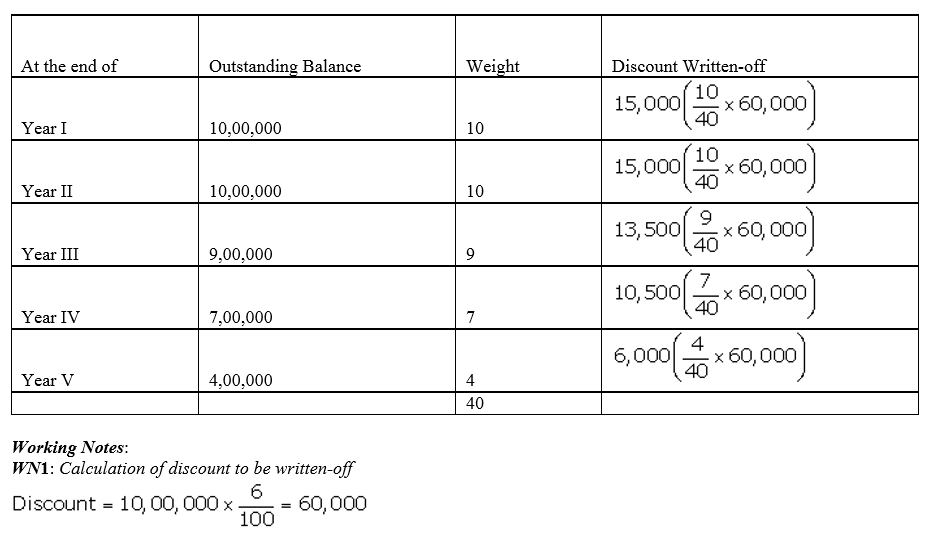

On 1st April 2012, Z Ltd. issued ₹ 10,00,000, 10% Debentures of ₹ 100 each at 94% redeemable at par. The debentures are to be redeemed by drawings method in the following manner:

Calculate the amount of discount on issue of debentures to be written off each year.

Solution:

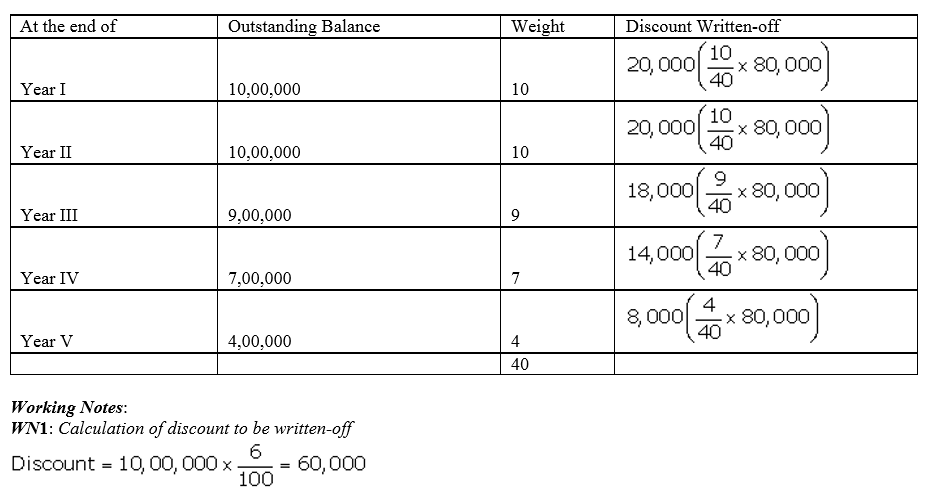

Question 45.

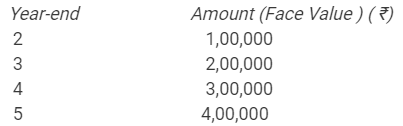

A company issued 9% Debentures of ₹ 10,00,000 at 8% discount, redeemable at par. The debentures are to be redeemed by drawings method in the following manner:

Calculate the amount of discount on issue of debentures to be written off each year.

Solution:

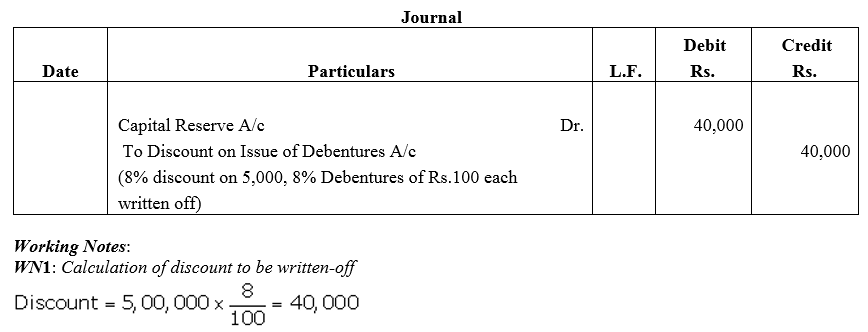

Question 46.

Kangaroo Ltd. issued 5,000, 8% Debentures of ₹ 100 each at a discount of 8%. The company decided to write off discount in the year of loss from Capital Reserve which has a balance of ₹ 1,00,000. Pass the journal entry for writing off discount.

Solution:

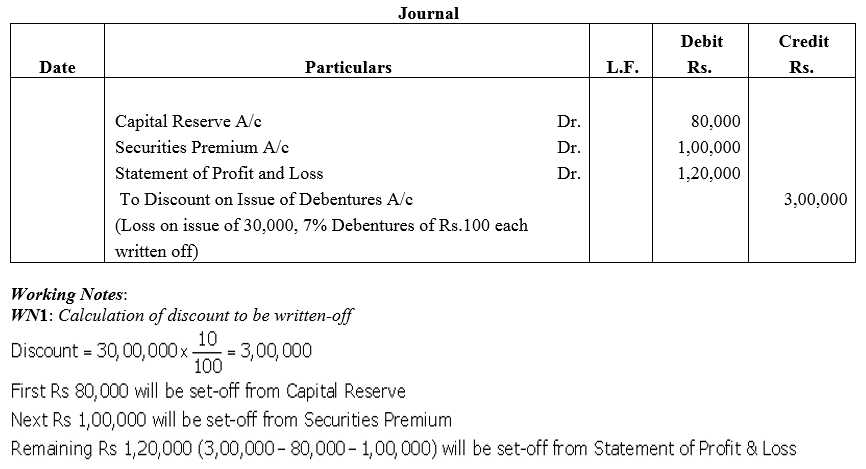

Question 47.

Grand Hotels Ltd.issued 30,000, 7% Debentures of ₹ 100 each at a discount of 5% redeemable at a premium of 5%. It decided to write off loss on issue of debentures first from Capital Reserve then from Securities Premium Reserve and balance from Statement of Profit and Loss. It has balances as follows:

Capital Reserve – ₹ 80,000 and Securities Premium Reserve – ₹ 1,00,000.

Pass the journal entry for writing off loss on Issue of Debentures.

Solution:

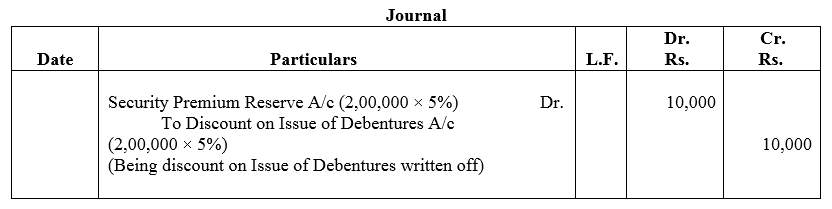

Question 48.

Kitply Ltd.issued ₹ 2,00,000, 10% Debentures at a discount of 5%. The terms of issue provide the repayment at the end of 4 years. Kitply Ltd.has a balance of ₹ 5,00,000 in Securities Premium Reserve. The company decided to write off discount on issue of debentures from Securities Premium Reserve in the first year.

Pass the journal entry.

Solution:

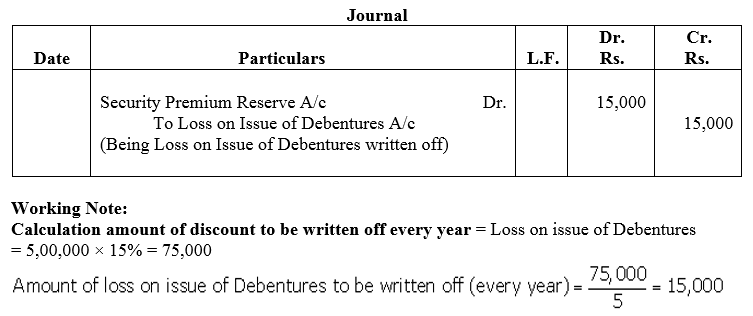

Question 49.

Typhoo Ltd.issued 5,000, 9% Debentures of ₹ 100 each at a discount of 5% redeemable at the end of 5 years at a premium of 10%. Typhoo Ltd.has a balance of ₹ 2,00,000 in Securities Premium Reserve. Loss on Issue of debentures is to be written off equally over the life of debentures from Securities Premium Reserve to the extent possible.

Pass the journal entries for writing off the Loss on Issue of Debentures.

Solution:

Question 50.

Tetley Ltd. issued 10,000, 9% Debentures of ₹ 100 each at a discount of 5% redeemable at the end of 5 years at a premium of 10%. Tetley Ltd. has a balance of ₹ 50,000 in Securities Premium Reserve. Loss on Issue of debentures is to be written off equally over the life of debentures.

Pass the journal entries for writing off the Loss on Issue of Debentures.

Solution:

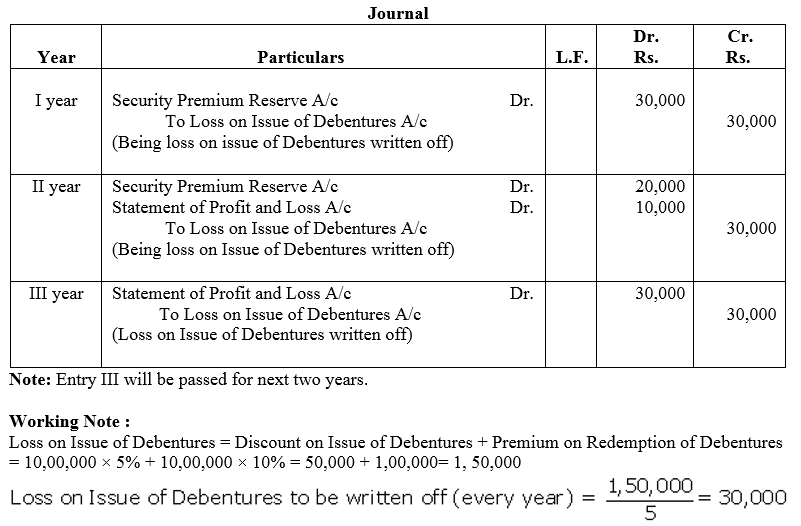

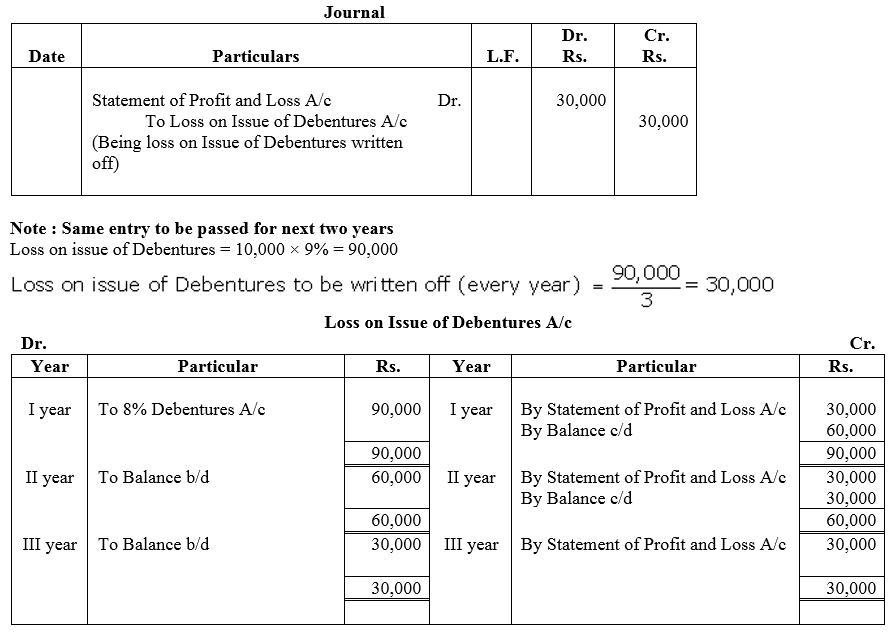

Question 51.

Global Ltd.issued 10,000, 8% Debentures of ₹ 100 each redeemable at the end of 3 years at a premium of ₹ 9.

Pass the journal entries for writing off the Loss on Issue of Debentures. Also prepare Loss on Issue of Debentures Account.

Solution:

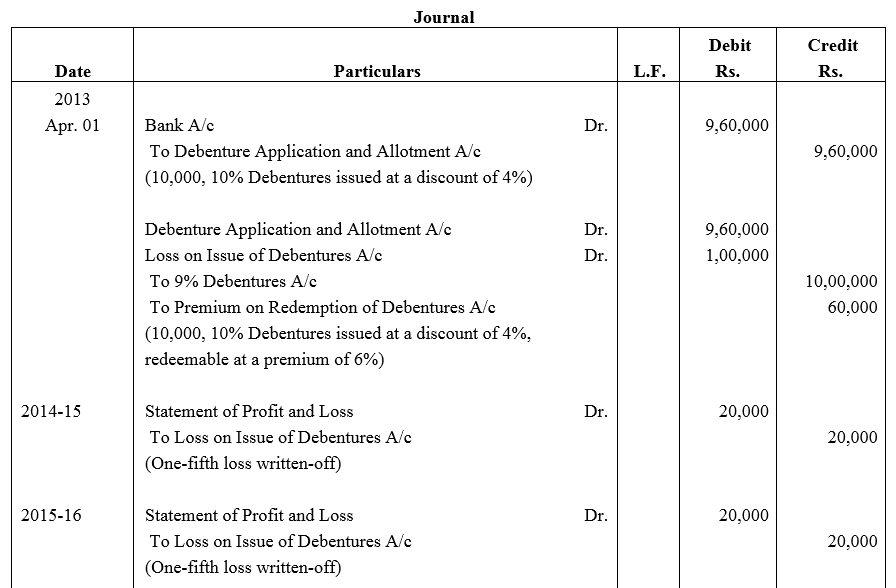

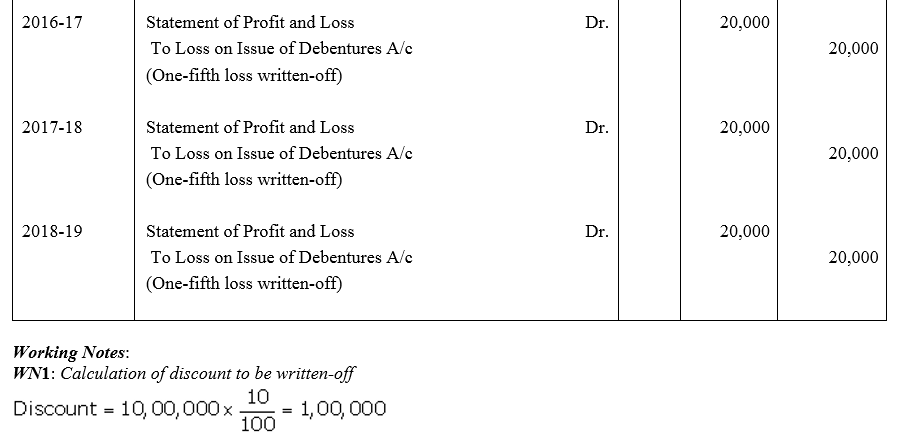

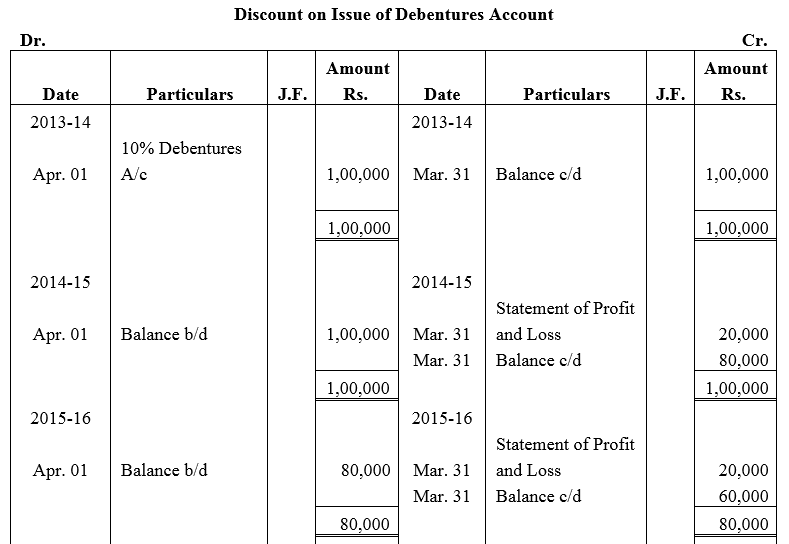

Question 52.

On 1st April, 2013, ABC Ltd. issued 10,000, 10% Debentures of ₹ 100 each at a discount of 4% redeemable after 5 years at a premium of 6%.

Pass the necessary journal entries for issue of debentures and writing off Loss on issue of Debentures. Also prepare Loss on issue of Debentures Account.

Solution:

Question 53.

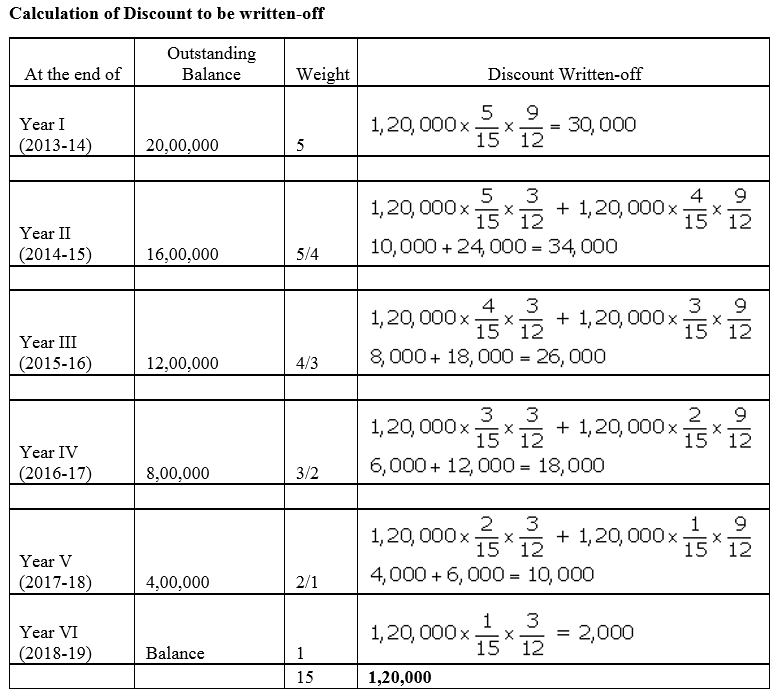

Feeble Ltd.issued 10% Debentures at 94% for ₹ 20,00,000 on 1st July, 2013 repayable by five equal annual installments of ₹ 4,00,000 each starting from 30th June, 2014. Calculate the amount of discount to be written off in every accounting year assuming that the company decides to write off the debentures discount during the life of the debentures.

Solution:

Question 54.

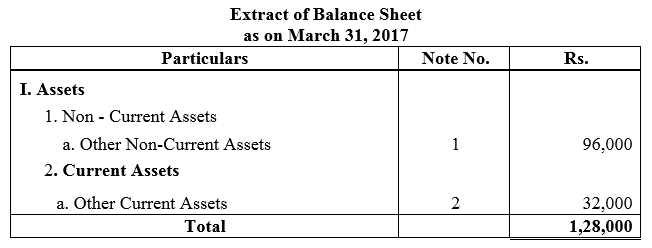

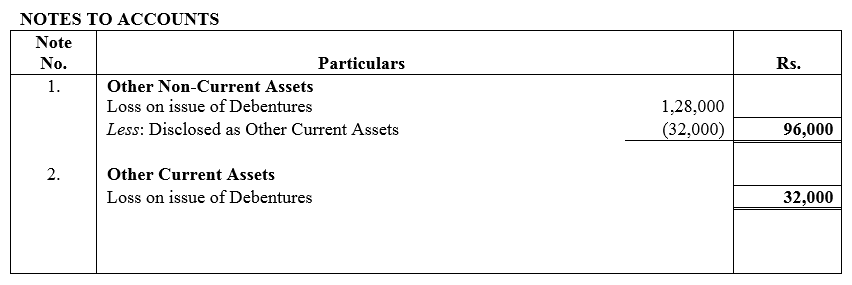

On 1st May, 2016, Goodluck Ltd. issued 16,000, 9% Debentures of ₹ 100 each at a discount of 10% redeemable at a premium of 10% redeemable after five years. All the debentures were subscribed and allotment was made. Discount on issue of Debentures is to be written off over the life of the debentures.

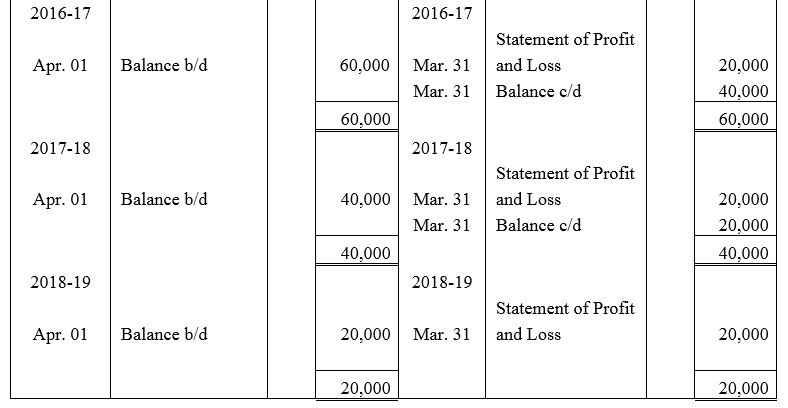

Prepare the Balance Sheet (extract) as at 31st March, 2017 showing Discount on issue of Debentures.

Solution:

Question 55.

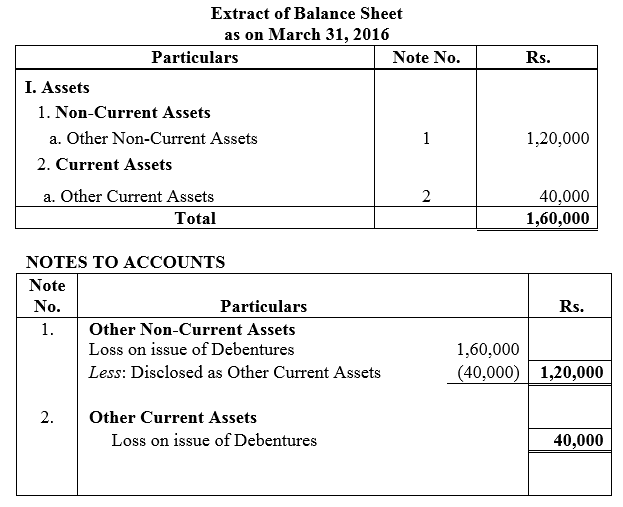

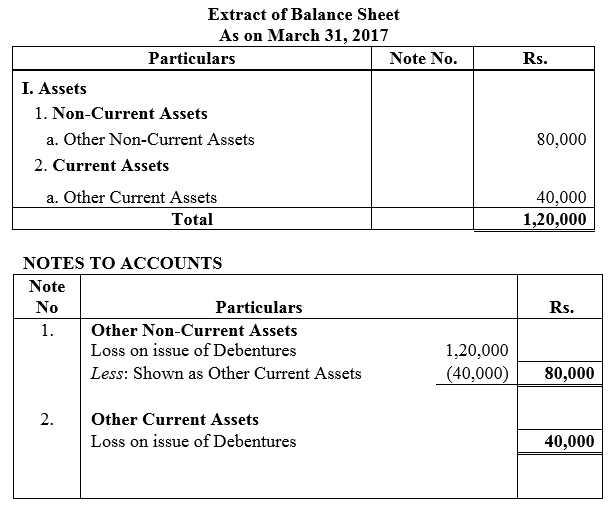

On 1st June, 2015, R Energy Ltd. issued 10,000, 7% Debentures of ₹ 100 each at a discount of 10% redeemable at a premium of 10% at the end of five years. All the debentures were subscribed and allotment was made. Loss on issue of Debentures is to be written off over the life of the debentures.

Prepare the Balance Sheet (extract) as at 31st March, 2016 and 31st March, 2017 showing Loss on issue of Debentures.

Solution:

We hope the TS Grewal Accountancy Class 12 Solutions Chapter 9 Issue of Debentures help you. If you have any query regarding TS Grewal Accountancy Class 12 Solutions Chapter 9 Issue of Debentures, drop a comment below and we will get back to you at the earliest.