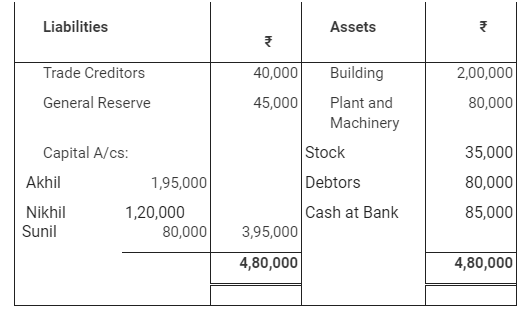

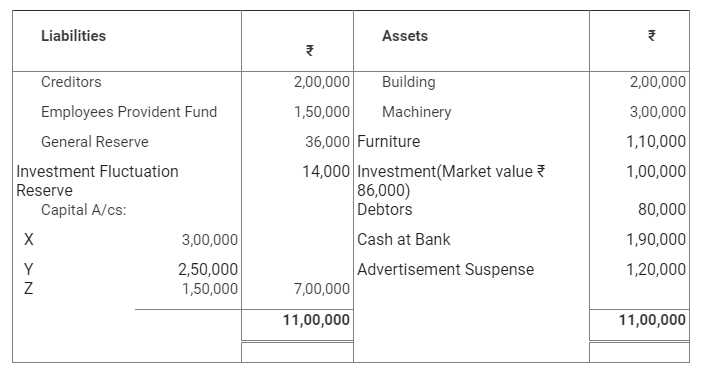

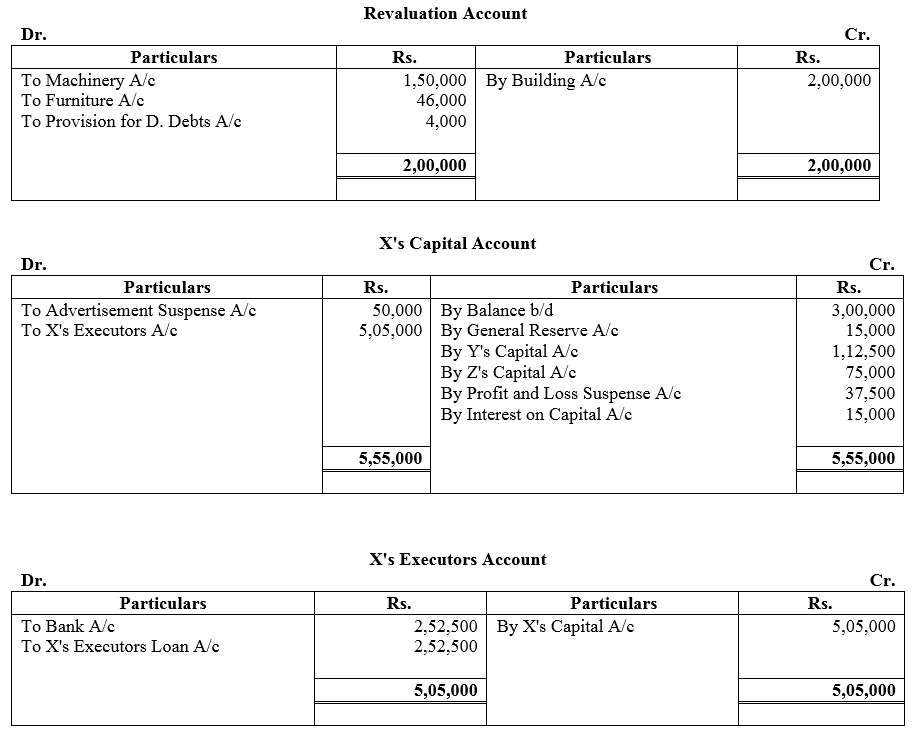

TS Grewal Accountancy Class 12 Solutions Chapter 5 Retirement/Death of a Partner – Here are all the TS Grewal solutions for Class 12 Accountancy Chapter 5. This solution contains questions, answers, images, explanations of the complete Chapter 5 titled Retirement/Death of a Partner of Accountancy taught in Class 12. If you are a student of Class 12 who is using TS Grewal Textbook to study Accountancy, then you must come across Chapter 5 Retirement/Death of a Partner. After you have studied lesson, you must be looking for answers of its questions. Here you can get complete TS Grewal Solutions for Class 12 Accountancy Chapter 5 Retirement/Death of a Partner in one place.

TS Grewal Accountancy Class 12 Solutions Chapter 5 Retirement / Death of a Partner

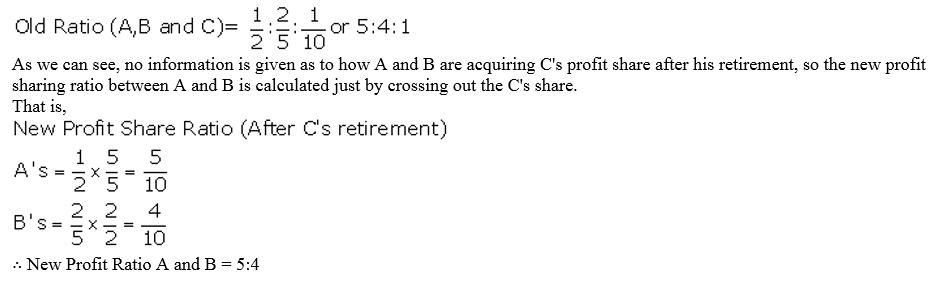

Question 1.

A, B and C were partners sharing profits in the ratio of 1/2, 2/5 and 1/10. Find the new ratio of the remaining partners if C retires.

Solution:

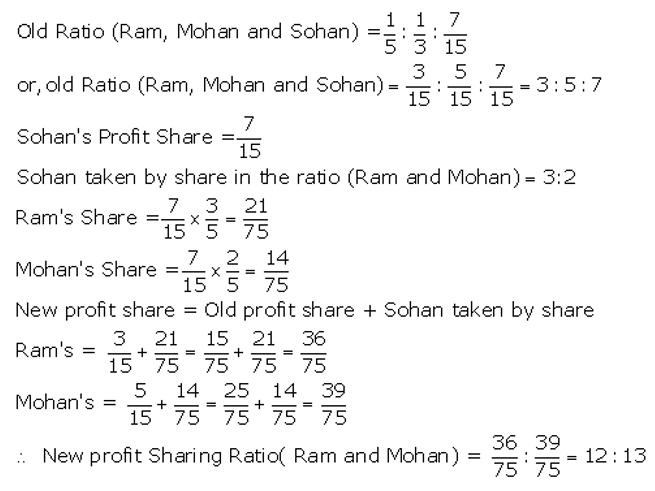

Question 2.

Ram, Mohan and Sohan were partners sharing profits in the ratio of 1/5, 1/3 and 7/15 respectively. Sohan retires and his share was taken by Ram and Mohan in the ratio of 3 : 2. Find out the new ratio.

Solution:

Question 3.

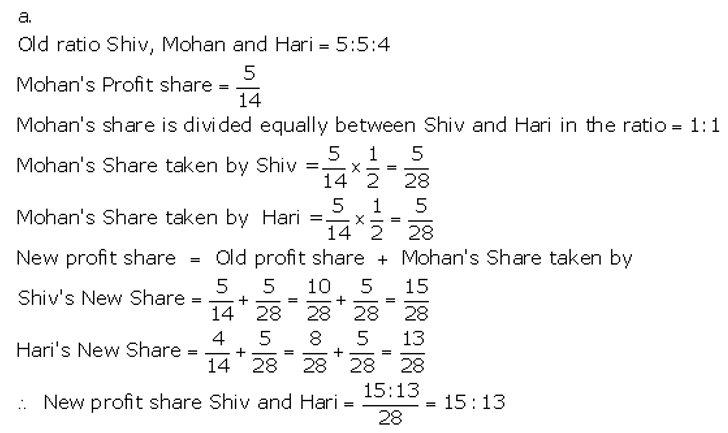

From the following particulars, calculate new profit-sharing ratio of the partners:

(a) Shiv, Mohan and Hari were partners in a firm sharing profits in the ratio of 5 : 5 : 4. Mohan retired and his share was divided equally between Shiv and Hari.

(b) P, Q and R were partners sharing profits in the ratio of 5 : 4 : 1. P retires from the firm.

Solution:

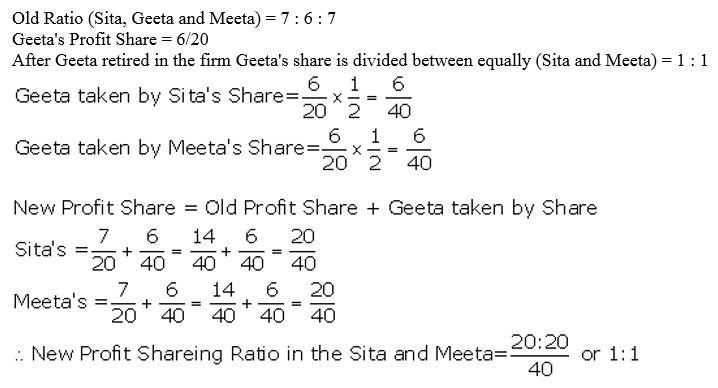

Question 4.

Sita, Geeta and Meeta were partners in a firm sharing profits in the ratio of 7 : 6 : 7. Geeta retired and her share was divided equally between Sita and Meeta. Calculate the new profit-sharing ratio of Sita and Meeta.

Solution:

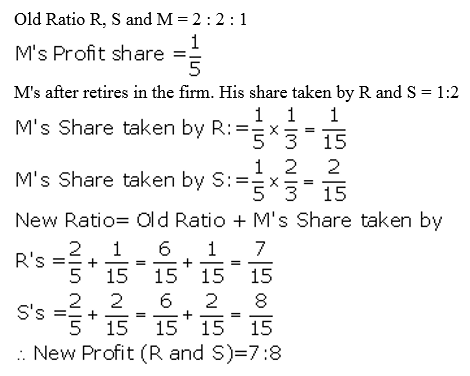

Question 5.

R, S and M are partners sharing profits in the ratio of 2/5, 2/5 and 1/5. M decides to retire from the business and his share is taken by R and S in the ratio of 1 : 2. Calculate the new profit-sharing ratio.

Solution:

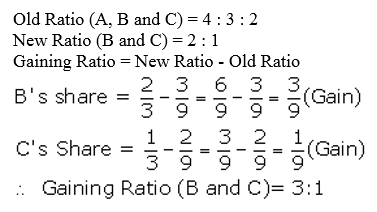

Question 6.

A, B and C were partners sharing profits in the ratio of 4 : 3 : 2. A retires, assuming B and C will share profits in the ratio of 2 : 1. Determine the gaining ratio.

Solution:

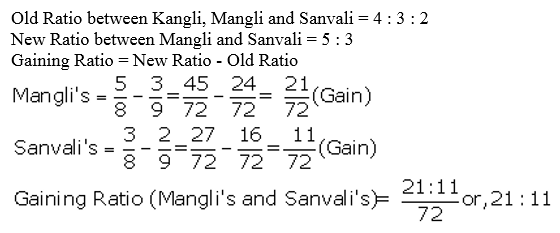

Question 7.

Kangli, Mangli and Sanvali are partners sharing profits in the ratio of 4 : 3 : 2. Kangli retires . Assuming Mangli and Sanvali will share profits in the future in the ratio of 5 : 3, determine the gaining ratio.

Solution:

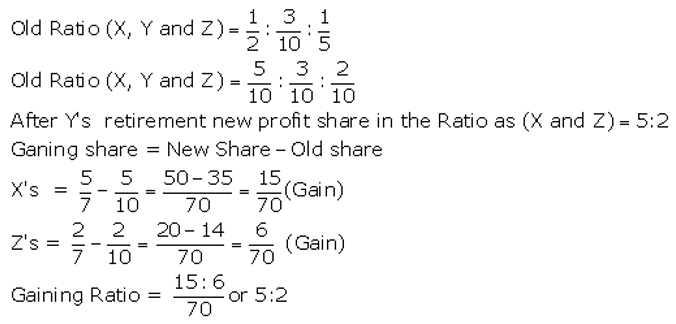

Question 8.

X, Y and Z are partners sharing profits in the ratio of 1/2, 3/10 and 1/5. Calculate the gaining ratio of remaining partners when Y retires from the firm.

Solution:

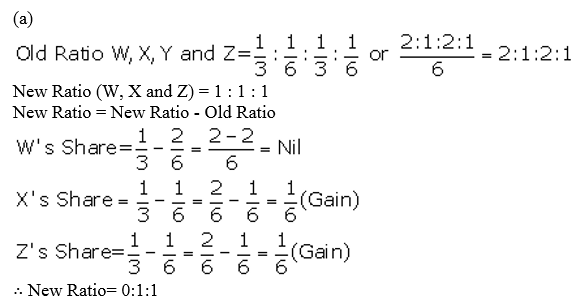

Question 9.

(a) W, X, Y and Z are partners sharing profits and losses in the ratio of 1/3, 1/6, 1/3 and 1/6 respectively. Y retires and W, X and Z decide to share the profits and losses equally in future. Calculate gaining ratio.

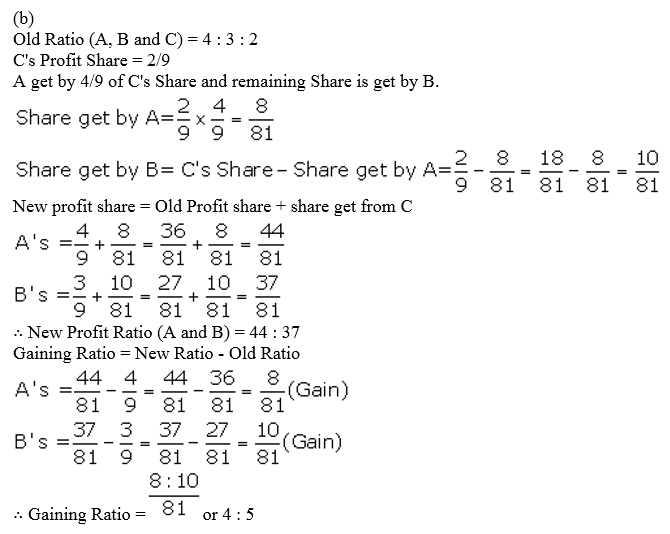

(b) A, B and C are partners sharing profits and losses in the ratio of 4 : 3 : 2. C retires from the business. A is acquiring 4/9 of C’s share and balance is acquired by B. Calculate the new profit-sharing ratio and gaining ratio.

Solution:

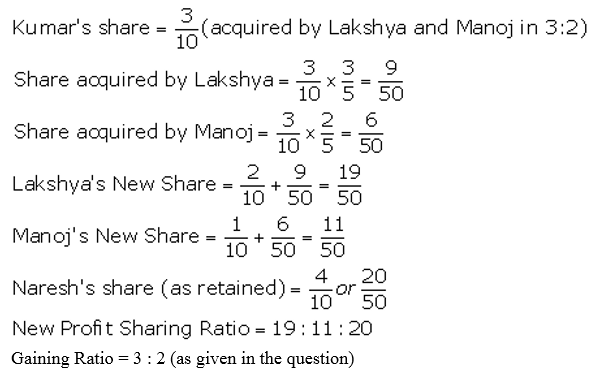

Question 10.

Kumar, Lakshya, Manoj and Naresh are partners sharing profits in the ratio of 3 : 2 : 1 : 4. Kumar retires and his share is acquired by Lakshya and Manoj in the ratio of 3 : 2. Calculate new profit-sharing ratio and gaining ratio of the remaining partners.

Solution:

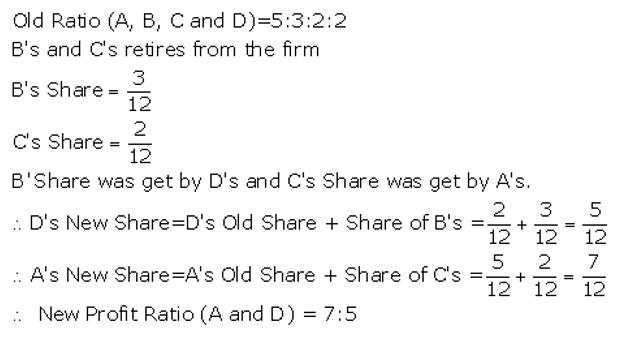

Question 11.

A, B, C and D were partners in a firm sharing profits in 5 : 3 : 2 : 2 ratio. B and C retired from the firm. B’s share was acquired by D and C’s share was acquired by A. Calculate new profit-sharing ratio of A and D.

Solution:

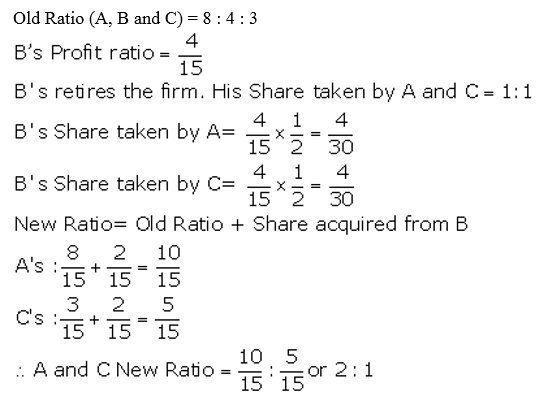

Question 12.

A, B and C were partners in a firm sharing profits in 8 : 4 : 3. B retires and his share is taken up equally by A and C. Find the new profit-sharing ratio.

Solution:

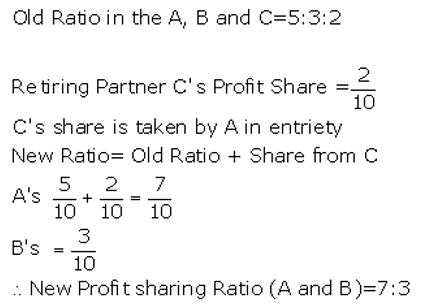

Question 13.

A, B and C are partners sharing profits in the ratio of 5 : 3 : 2. C retires and his share is taken up by A. Calculate new profit-sharing ratio of A and B.

Solution:

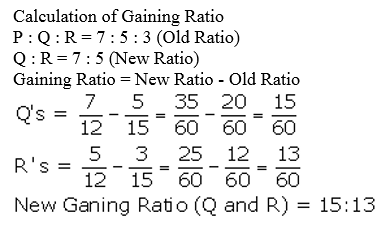

Question 14.

P, Q and R are partners sharing profits in the ratio of 7 : 5 : 3. P retires and it is decided that profit-sharing ratio between Q and R will be same as existing between P and Q. Calculate New profit-sharing ratio and Gaining Ratio.

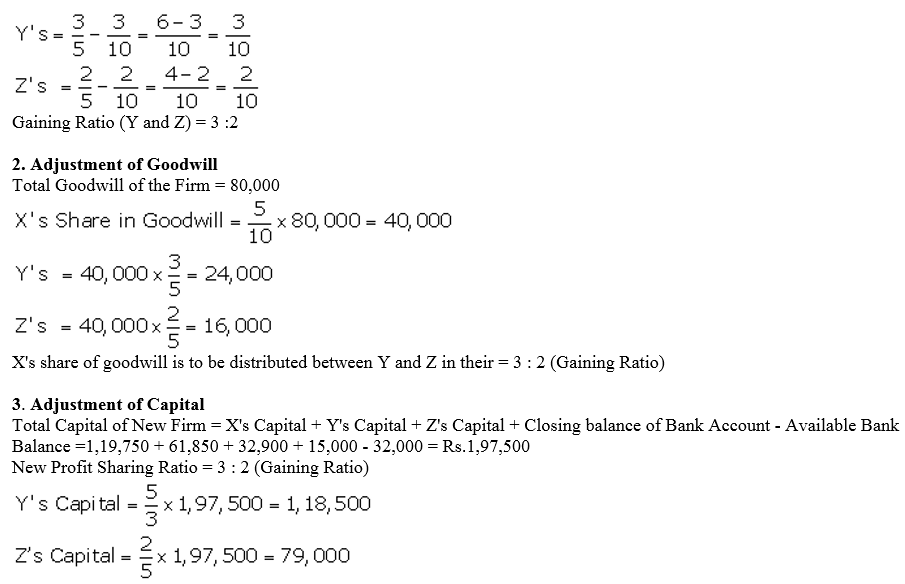

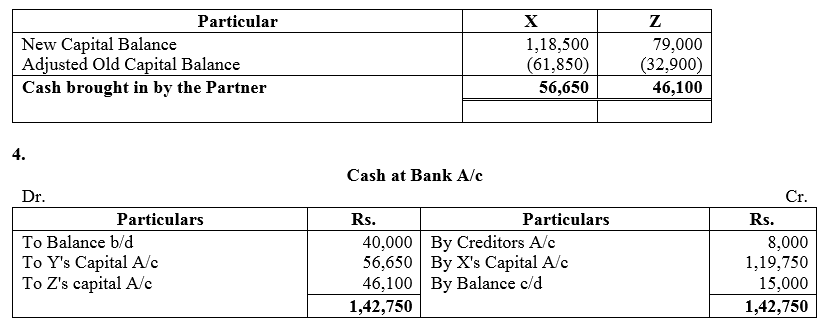

Solution:

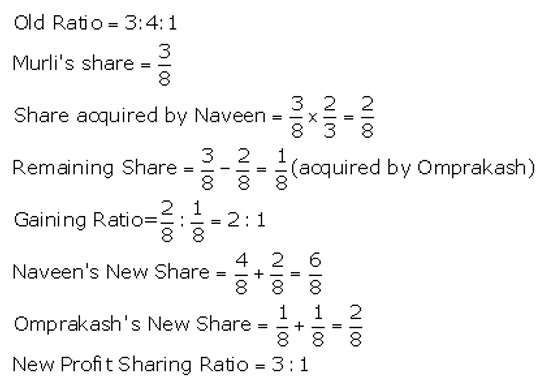

Question 15.

Murli, Naveen and Omprakash are partners sharing profits in the ratio of 3/8, 1/2 and 1/8. Murli retires and surrenders 2/3rd of his share in favour of Naveen and remaining share in favour of Omprakash. Calculate new profit-sharing ratio and gaining ratio of the remaining partners.

Solution:

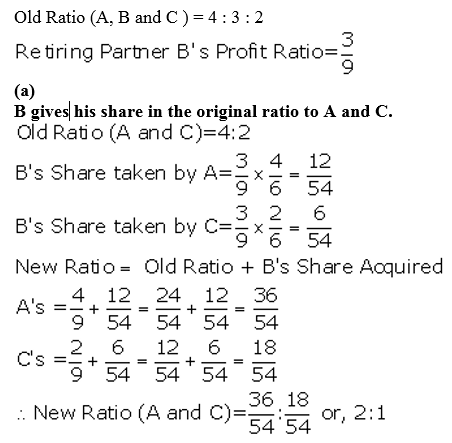

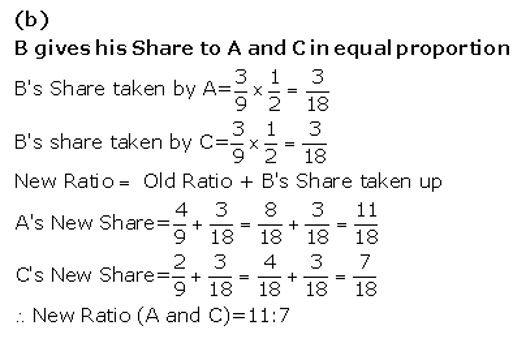

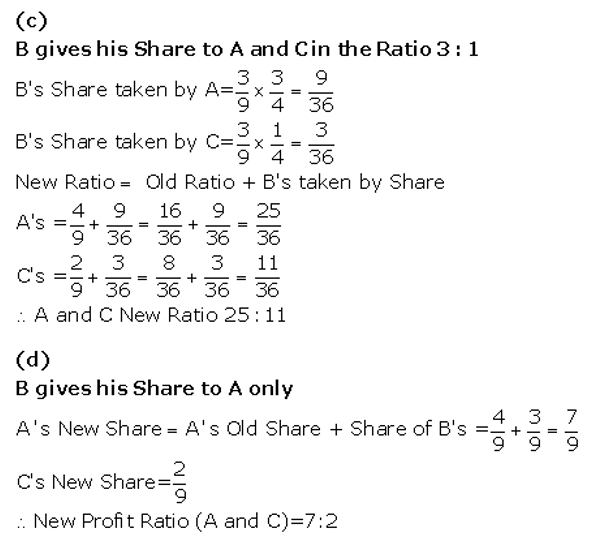

Question 16.

A, B and C are partners in a firm sharing profits and losses in the ratio of 4 : 3 : 2. B decides to retire from the firm. Calculate new profit-sharing ratio of A and C in the following circumstances:

(a) If B gives his share to A and C in the original ratio of A and C.

(b) If B gives his share to A and C in equal proportion.

(c) If B gives his share to A and C in the ratio of 3 : 1.

(d) If B gives his share to A only.

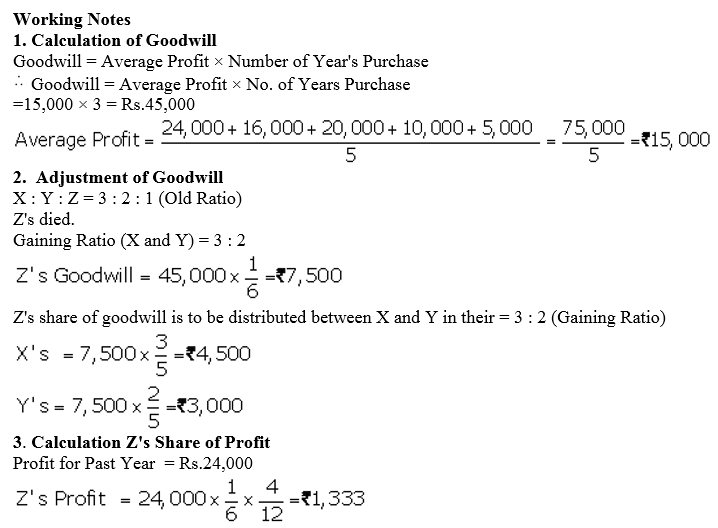

Solution:

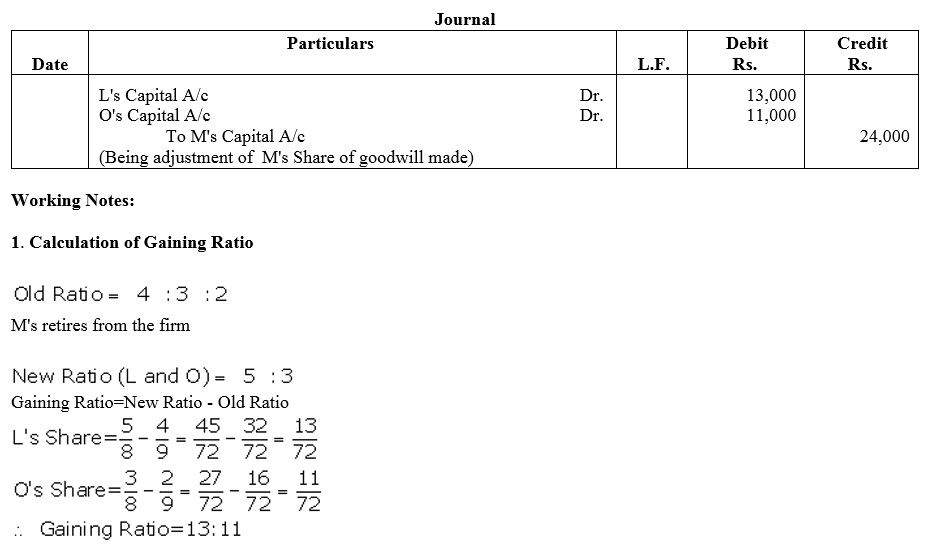

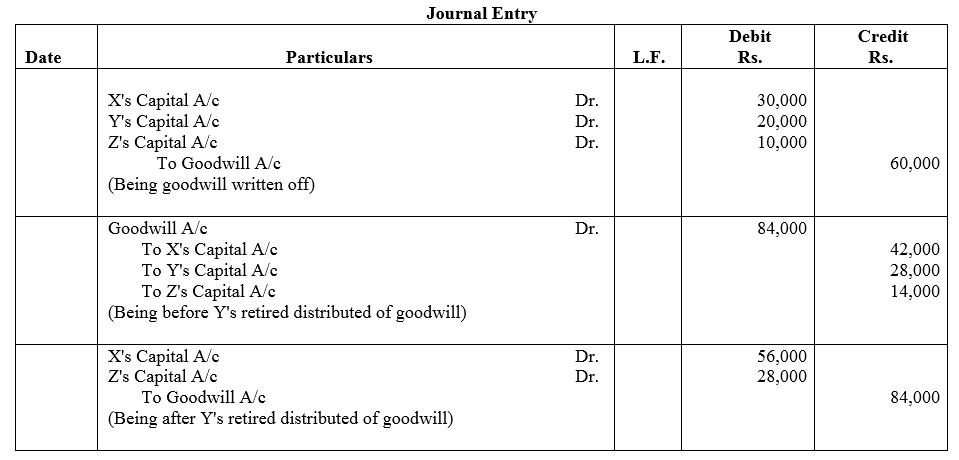

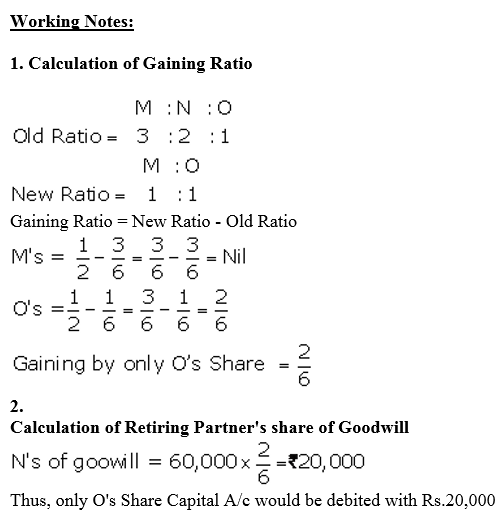

Question 17.

L, M and O are partners sharing profits and losses in the ratio of 4 : 3 : 2. M retires and the goodwill is valued at ₹ 72, 000. Calculate M’s share of goodwill and pass the necessary Journal entry for Goodwill. L and O decided to share the future profits and losses in the ratio of 5 : 3.

Solution:

Question 18.

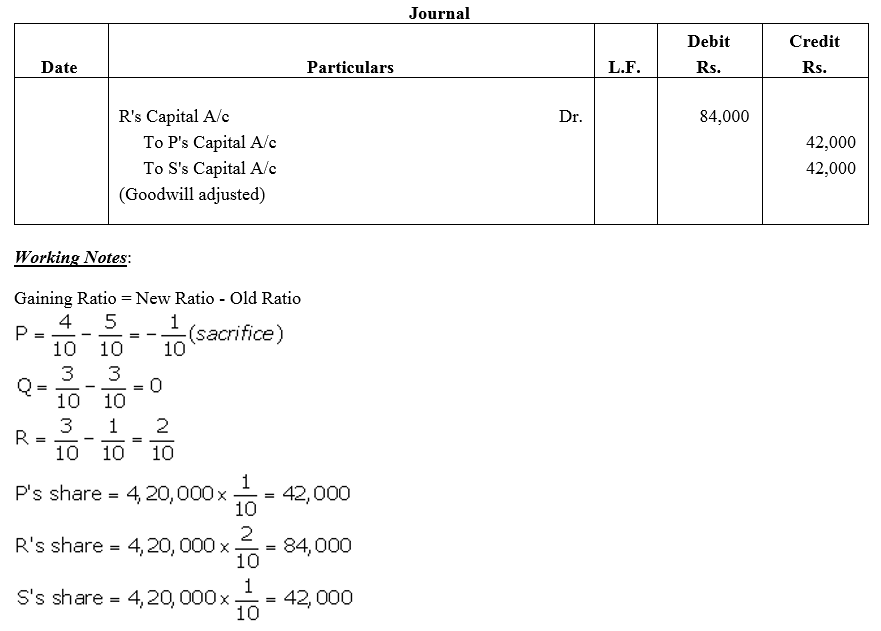

P, Q, R and S were partners in a firm sharing profits in the ratio of 5 : 3 : 1 : 1. On 1st January, 2017, S retired from the firm. On S’s retirement the goodwill of the firm was valued at ₹ 4,20,000. The new profit-sharing ratio between P, Q and R will be 4 : 3 : 3.

Showing your working notes clearly, pass necessary journal entry for the treatment of goodwill in the books of the firm on S’s retirement.

Solution:

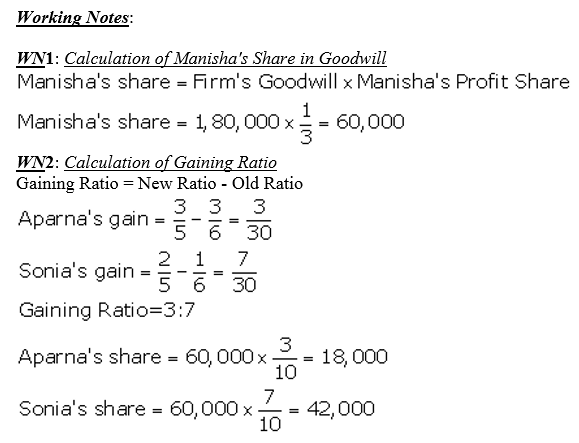

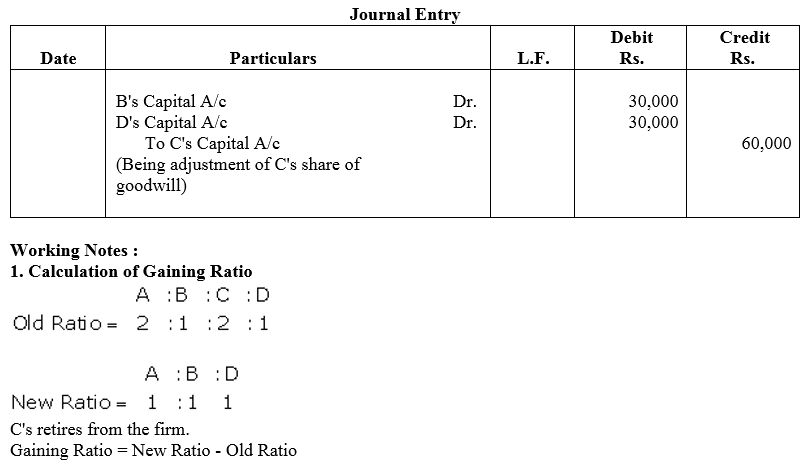

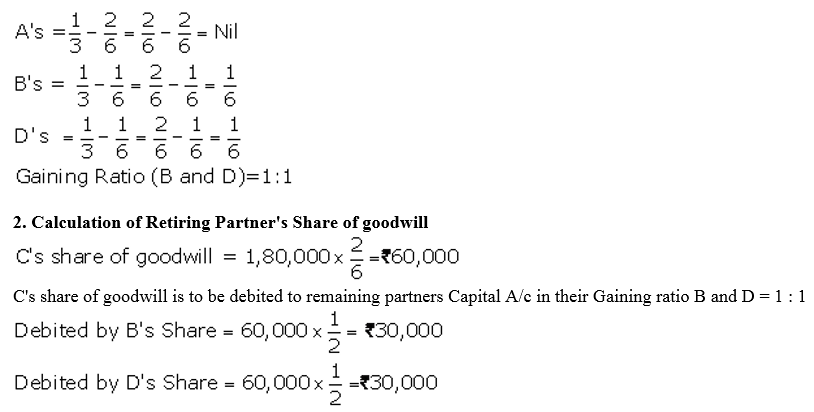

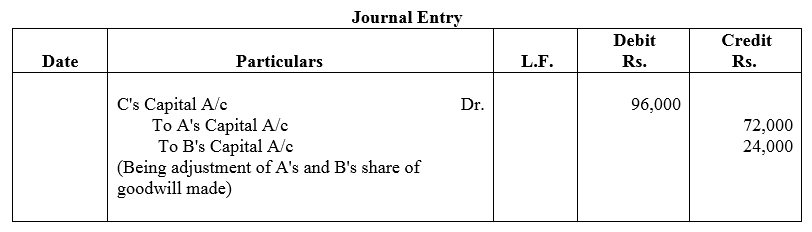

Question 19.

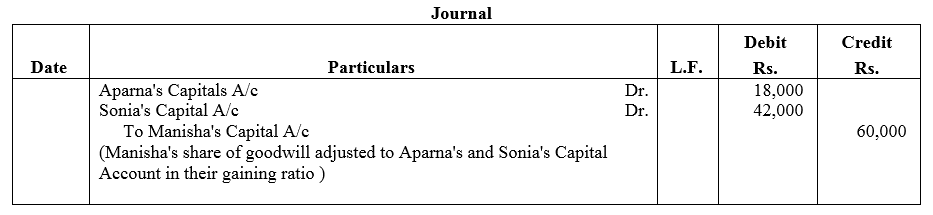

Aparna, Manisha and Sonia are partners sharing profits in the ratio of 3 : 2 : 1. Manisha retires and goodwill of the firm is valued at ₹ 1,80,000. Aparna and Sonia decided to share future profits in the ratio of 3 : 2. Pass necessary journal entries.

Solution:

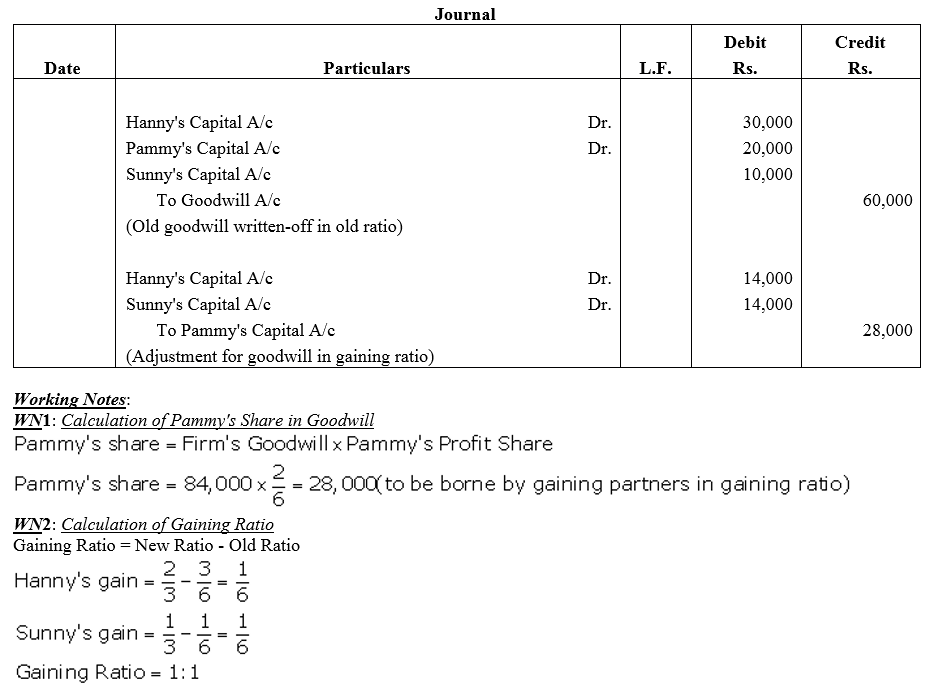

Question 20.

Hanny, Pammy and Sunny are partners sharing profits in the ratio of 3 : 2 : 1. Goodwill is appearing in the books at a value of ₹ 60,000. Pammy retires and at the time of Pammy’s retirement, goodwill is valued at ₹ 84,000. Hanny and Sunny decided to share future profits in the ratio of 2 : 1. Record the necessary journal entries.

Solution:

Question 21.

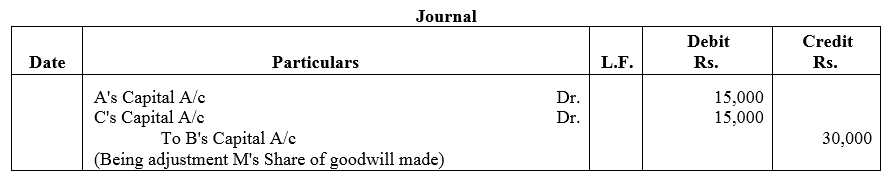

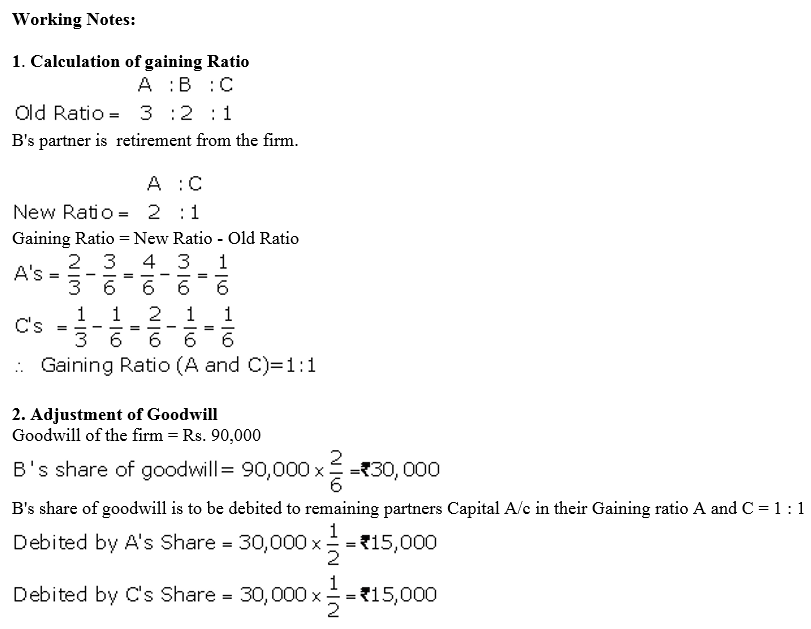

A, B and C are partners sharing profits in the ratio of 3 : 2 : 1. B retired and the new profit-sharing ratio between A and C was 2 : 1. On B’s retirement, the goodwill of the firm was valued at ₹ 90,000. Pass necessary journal entry for the treatment of goodwill on B’s retirement.

Solution:

Question 22.

X, Y and Z are partners sharing profits in the ratio of 3 : 2 : 1. Goodwill is appearing in the books at a value of ₹ 60,000. Y retires and at the time of Y’s retirement, goodwill is valued at ₹ 84,000. X and Z decide to share future profits in the ratio of 2 : 1. Pass the necessary journal entries through Goodwill Account.

Solution:

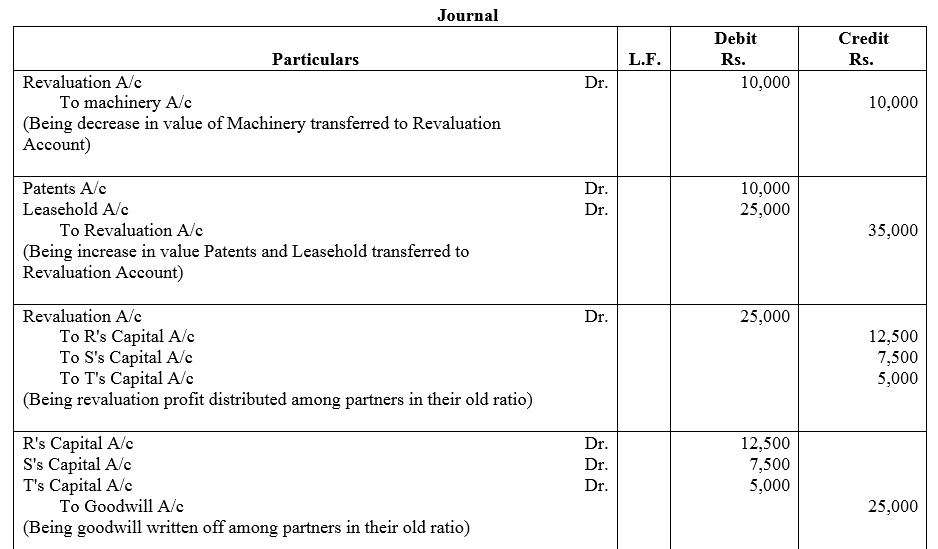

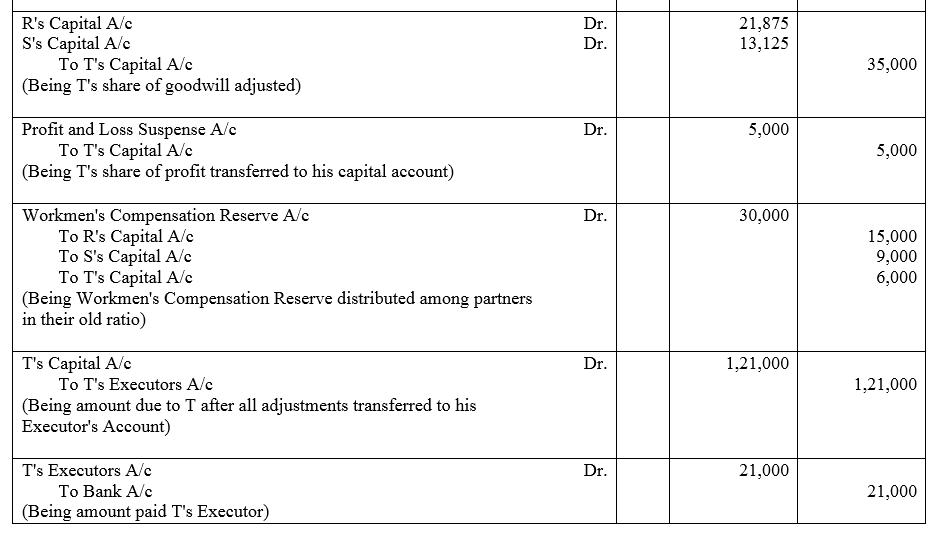

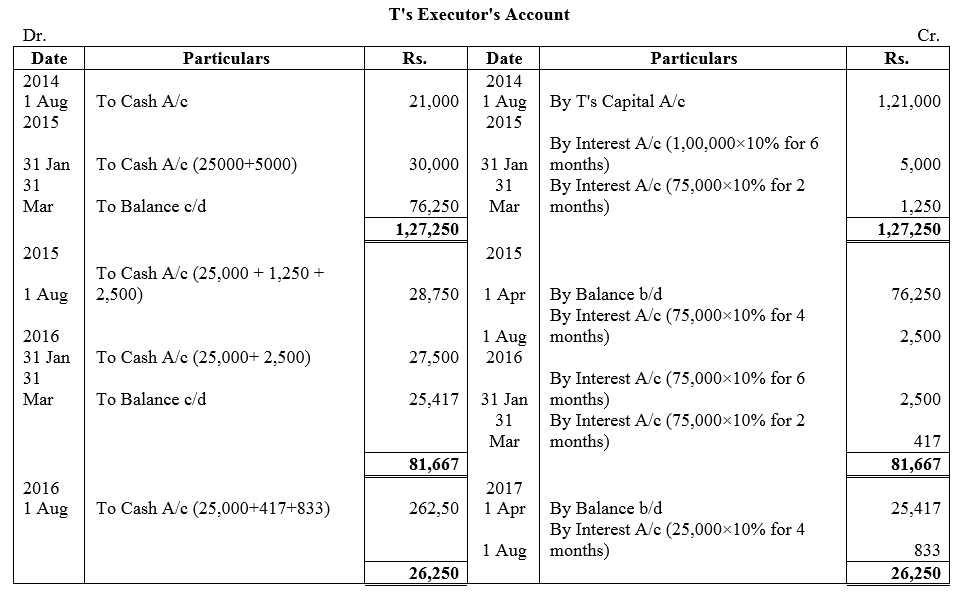

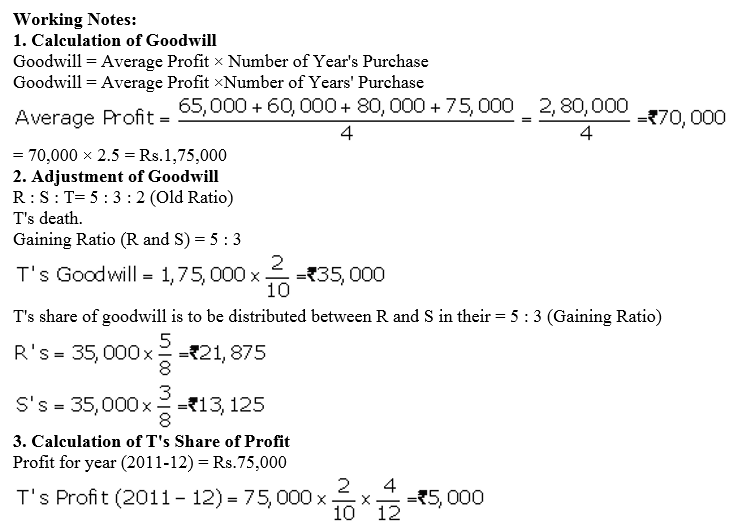

Question 23.

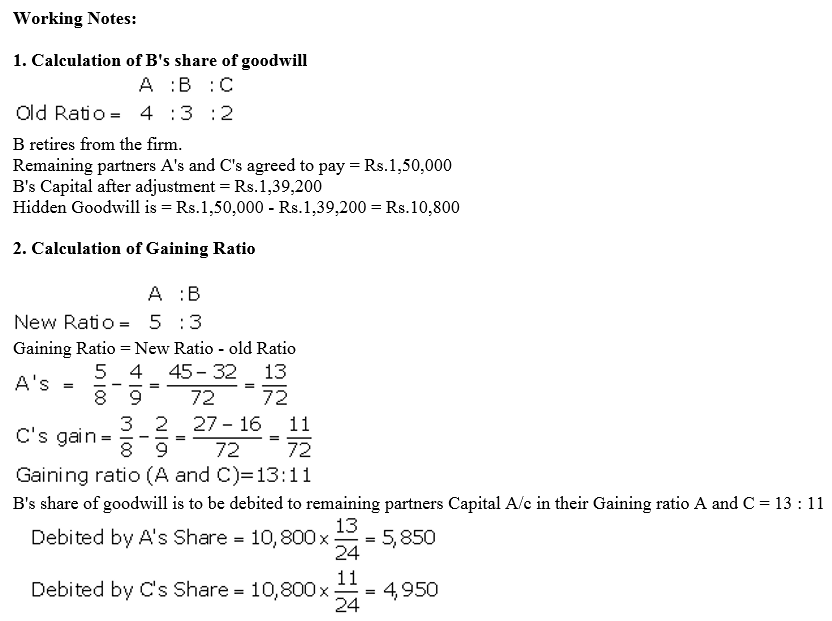

A, B and C are partners sharing profits in the ratio of 4/9 : 3/9 : 2/9. B retires and his capital after making adjustments for reserves and gain (profit) on revaluation stands at ₹ 1, 39, 200. A and C agreed to pay him ₹ 1,50,000 in full settlement of his claim. Record necessary journal entry for adjustment of goodwill if the new profit-sharing ratio is decided at 5 : 3.

Solution:

Question 24.

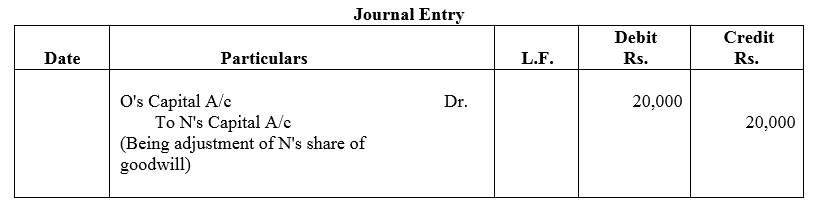

M, N and O are partners in a firm sharing profits in the ratio of 3 : 2 : 1. Goodwill has been valued at ₹ 60,000. On N’s retirement, M and O agree to share profits equally. Pass the necessary journal entry for treatment of N’s share of goodwill.

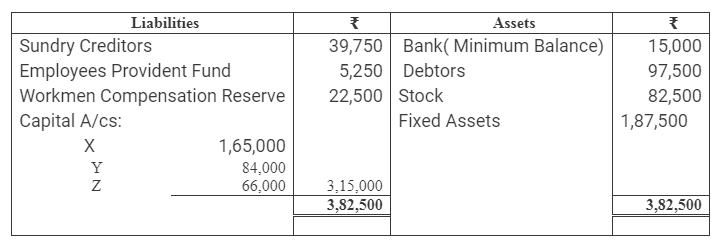

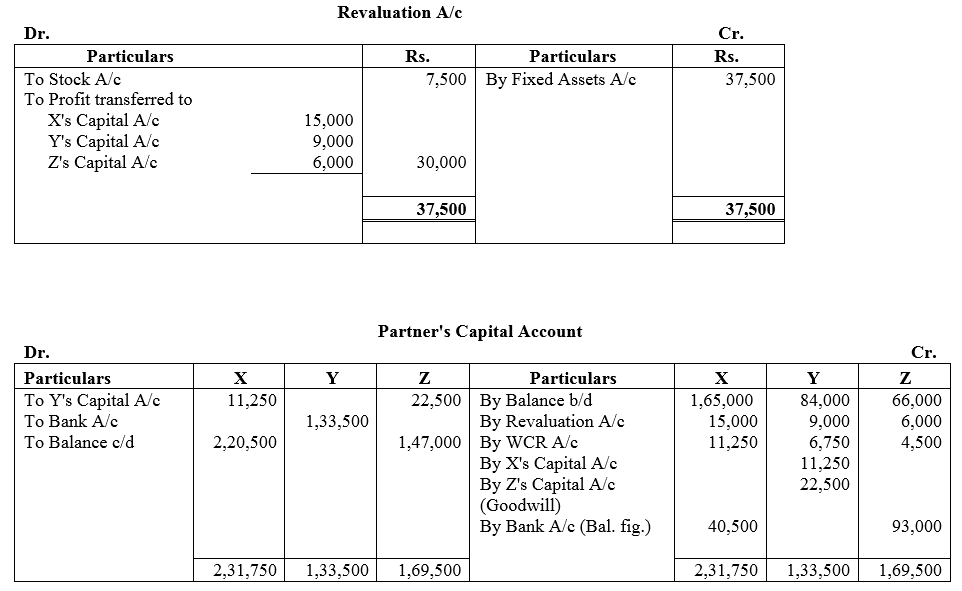

Solution:

Question 25.

A, B, C and D are partners in a firm sharing profits in the ratio of 2 : 1 : 2 : 1. On the retirement of C, Goodwill was valued ₹ 1,80,000. A, B and D decide to share future profits equally. Pass the necessary journal entry for the treatment of goodwill.

Solution:

Question 26.

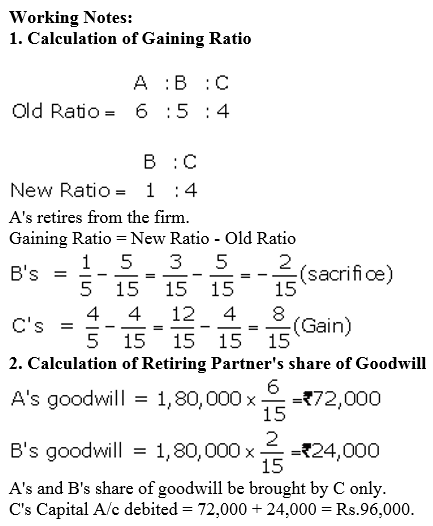

A, B and C were partners in a firm sharing profits in the ratio of 6 : 5 : 4. Their capitals were A – ₹ 1,00,000; B – ₹ 80,000 and C – ₹ 60,000 respectively. On 1st April, 2009, A retired from the firm and the new profit sharing ratio between B and C was decided as 1 : 4. On A’s retirement, the goodwill of the firm was valued at ₹ 1,80,000. Showing your calculations clearly, pass the necessary journal entry for the treatment of goodwill on A’s retirement.

Solution:

Question 27.

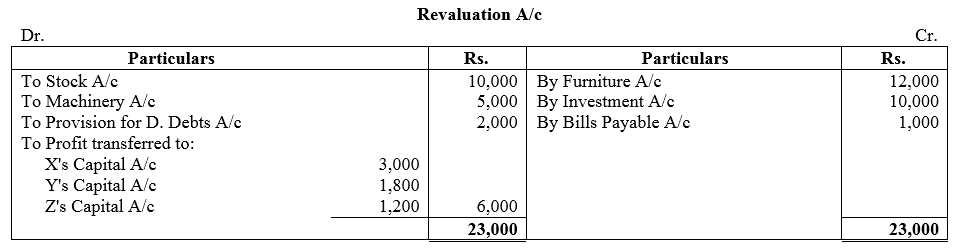

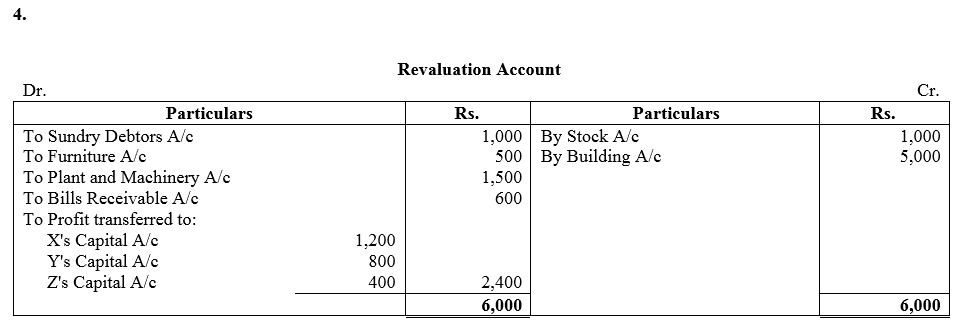

X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2. Z retires and on the date of his retirement, the following adjustments were agreed upon:

(a) The value of Furniture is to be increased by ₹ 12,000.

(b) The value of stock to be decreased by ₹ 10,000.

(c) Machinery of the book value of ₹ 50,000 is to be depreciated by 10%.

(d) A Provision for Doubtful Debts @ 5% is to be created on debtors of book value of ₹ 40,000.

(e) Unrecorded Investment worth ₹ 10,000.

(f) An item of ₹ 1,000 included in bills payable is not likely to be claimed, hence should be written back.

Pass necessary journal entries.

Solution:

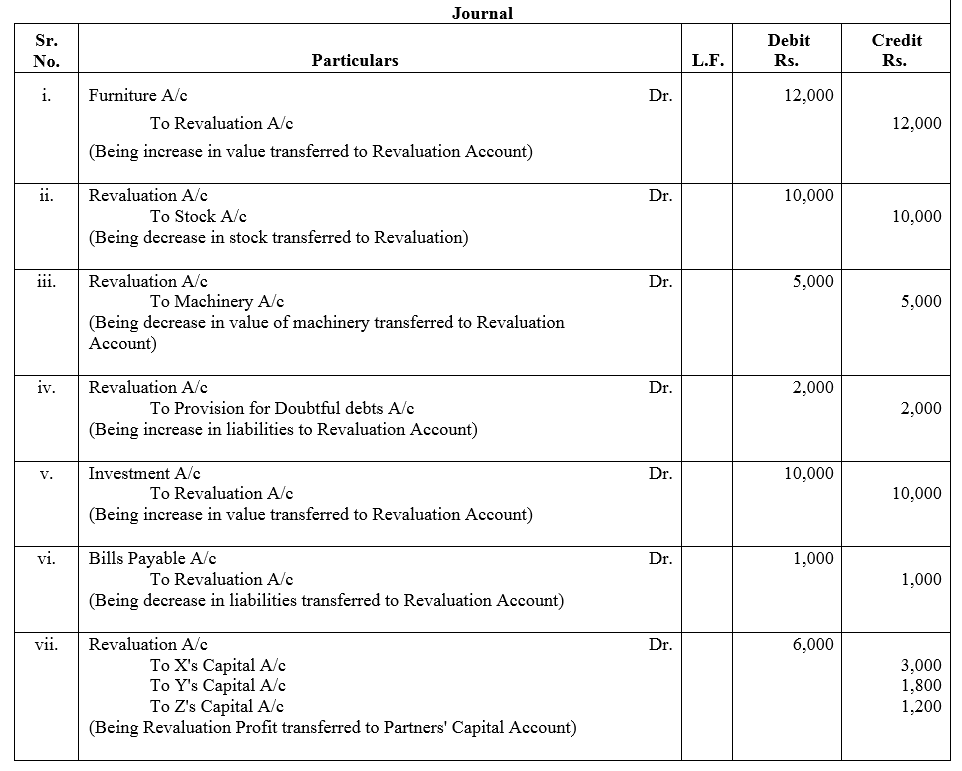

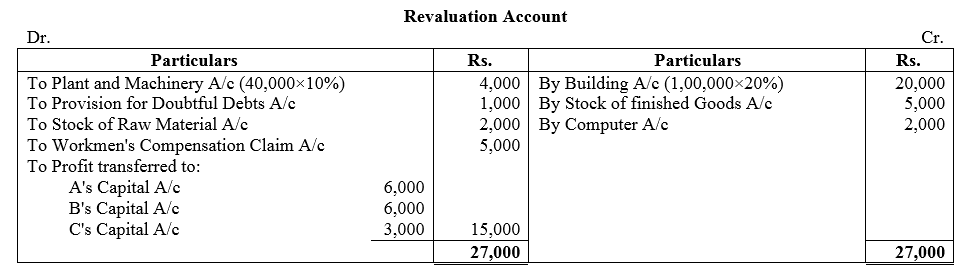

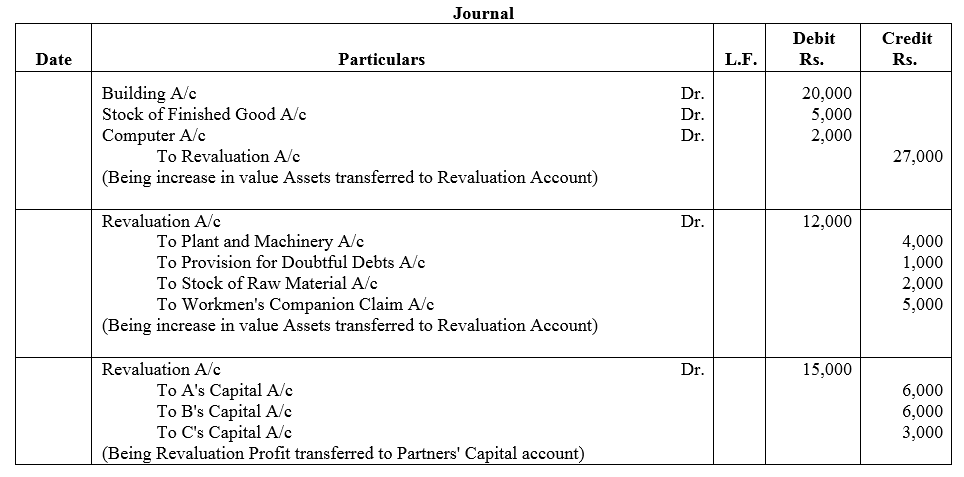

Question 28.

A, B and C were partners, sharing profits and losses in the ratio of 2 : 2 : 1. B decides to retire on 31st March, 2018. On the date of his retirement, some of the assets and liabilities appeared in the books as follows:

Creditors – ₹ 70,000; Building – ₹ 1,00,000; Plant and Machinery – ₹ 40,000; Stock of Raw Material – ₹ 20,000; Stock of Finished Goods – ₹ 30,000 and Debtors – ₹ 20,000.

The following was agreed among the partners on B’s retirement:

(a) Building to be appreciated by 20%.

(b) Plant and Machinery to be depreciated by 10%.

(c) A Provision of 5% on Debtors to be created for Doubtful Debts.

(d) Stock of Raw Materials too be valued at ₹ 18,000 and Finished Goods at ₹ 35,000.

(e) An Old Computer previously written off was sold for ₹ 2,000 as scrap.

(f) Firm had to pay ₹ 5,000 to an injured employee.

Pass necessary journal entries to record the above adjustments and prepare the Revaluation Account.

Solution:

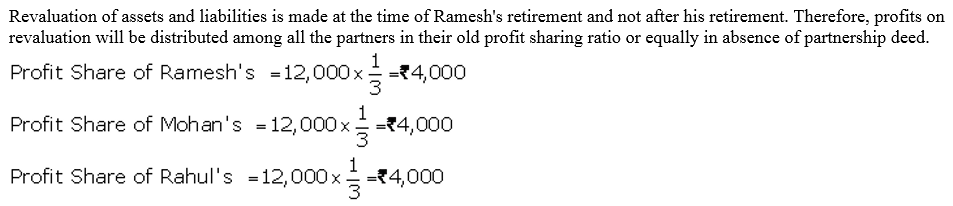

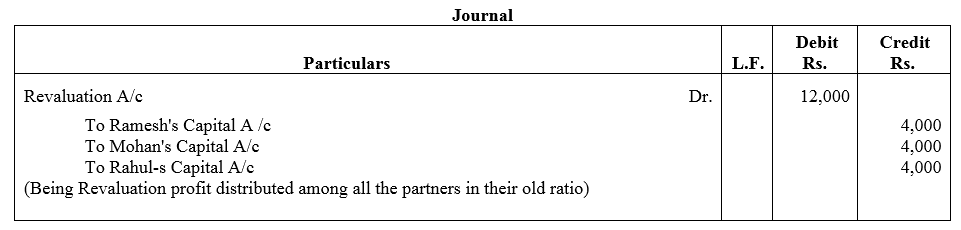

Question 29.

Ramesh wants to retire from the firm. The gain (profit) on revaluation on that date was ₹ 12,000. Mohan and Rahul want to share this in their new profit-sharing ratio of 3 : 2. Ramesh wants this to be shared equally. How is the profit to be shared ? Give reasons.

Solution:

Question 30.

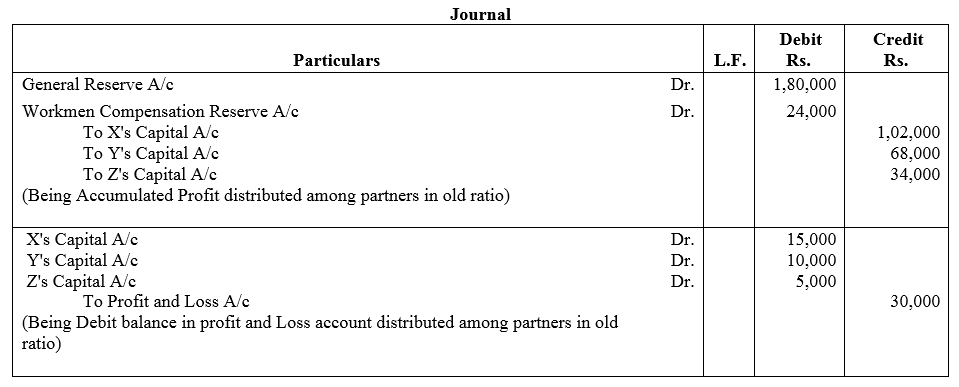

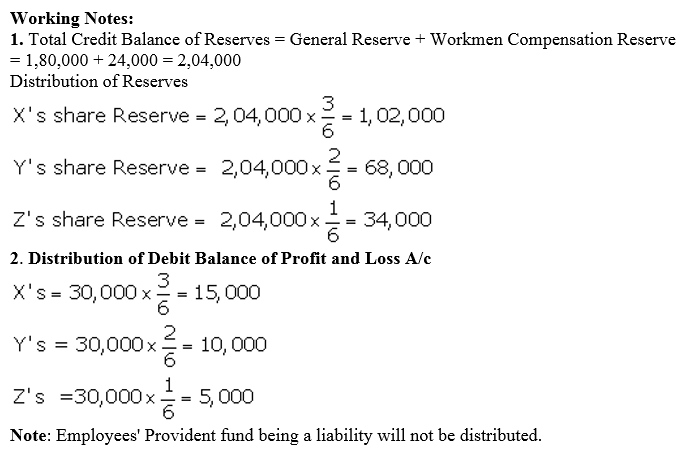

X, Y and Z are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Z retires from the firm on 31st March, 2018. On the date of Z’s retirement, the following balances appeared in the books of the firm:

General Reserve – ₹ 1,80,000

Profit and Loss Account (Dr.) – ₹ 30,000

Workmen Compensation Reserve – ₹ 24,000, which was no more required

Employees Provident Fund – ₹ 20,000.

Pass necessary journal entries for the adjustment of these items on Z’s retirement.

Solution:

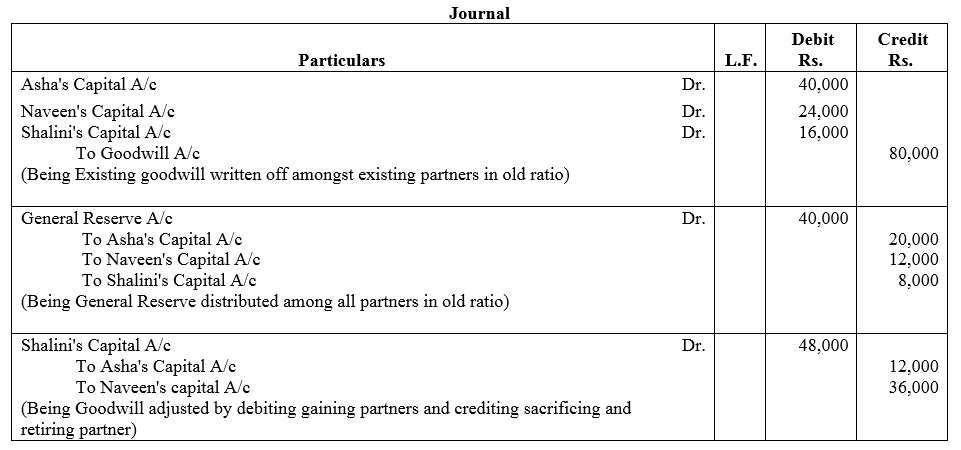

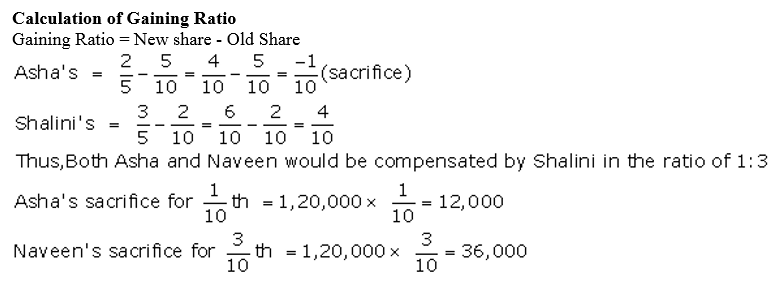

Question 31.

Asha, Naveen and Shalini were partners in a firm sharing profits in the ratio of 5 : 3 : 2. Goodwill appeared in their books at a value of ₹ 80,000 and General Reserve at ₹ 40,000. Naveen decided to retire from the firm. On the date of his retirement, goodwill of the firm was valued at ₹ 1,20,000. The new profit ratio decided among Asha and Shalini is 2 : 3.

Record necessary journal entries on Naveen’s retirement.

Solution:

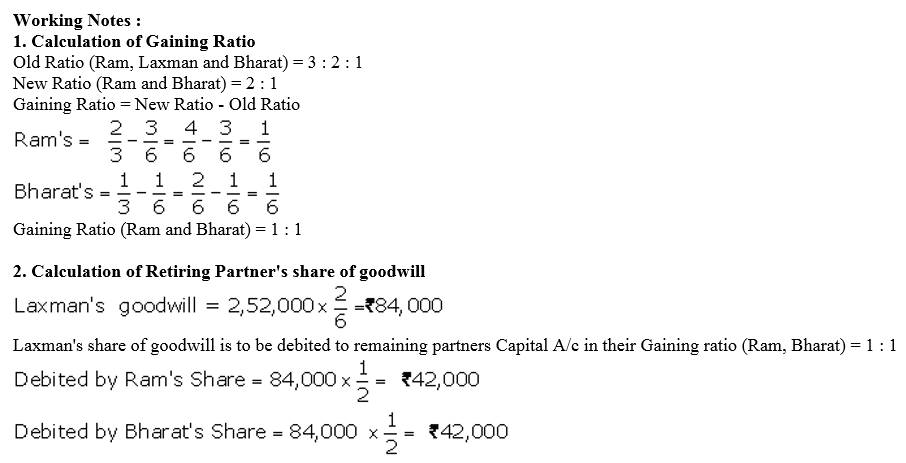

Question 32.

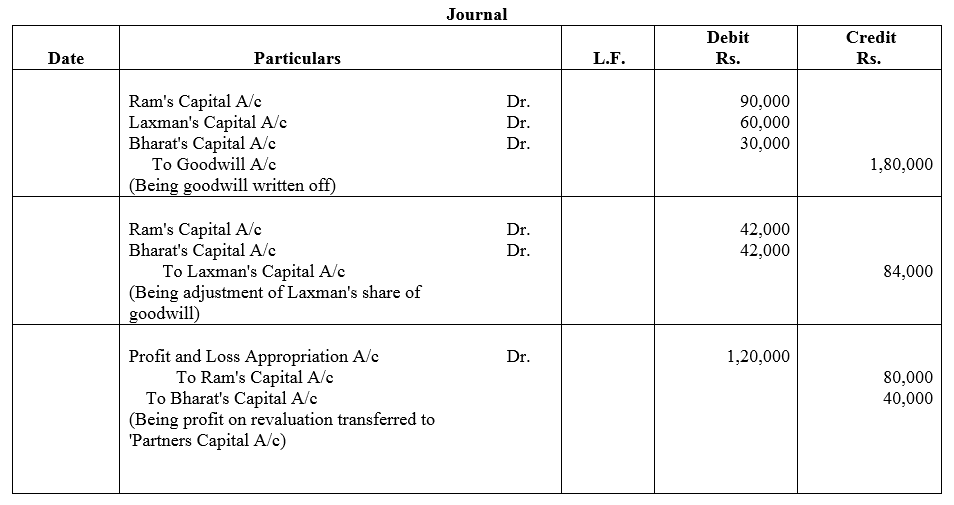

Ram, Laxman and Bharat are partners sharing profits in the ratio of 3 : 2 : 1. Goodwill is appearing in the books at a value of ₹ 1,80,000. Laxman retires and at the time of his retirement, goodwill is valued at ₹ 2,52,000. Ram and Bharat decided to share future profits in the ratio of 2 : 1. The Profit for the first year after Laxman’s retirement amount to ₹ 1,20,000. Give the necessary journal entries to record goodwill and to distribute the profit. Show your calculations clearly.

Solution:

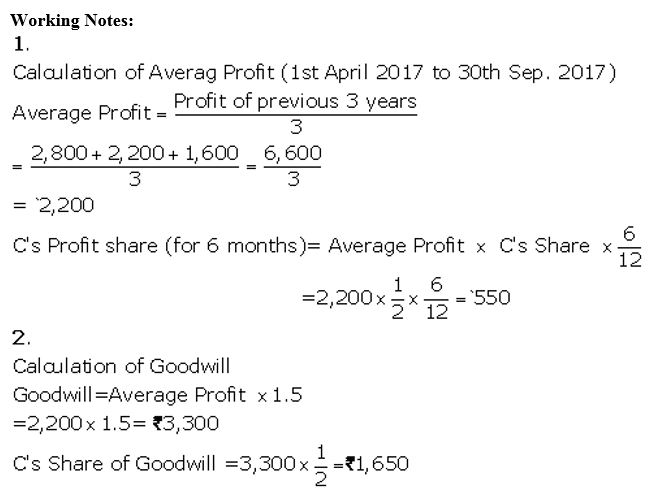

Question 33.

The Partnership Deed of C and D, who are equal partners has a clause that any partner may retire from the firm on the following terms by giving a six-month notice in writing:

The retiring partner shall be paid-

(a) the amount standing to the credit of his Capital Account and Current Account.

(b) His share of profits to the date of retirement, calculated on the basis of the average profit of the three preceding completed years.

(c) half the amount of the goodwill of the firm calculated at 1\(\frac { 1 }{ 2 }\) times the average profit of the three preceding completed years.

C gave a notice on 31st March, 2017 to retire on 30th September 2017, when the balance of his Capital Account was ₹ 6,000 and his Current Account (DR.) ₹ 500. The profits for the three preceding completed years were : year ended 31st March, 2015 – ₹ 2,800; year ended 31st March, 2016 – ₹ 2,200 and year ended 31st March, 2017 – ₹ 1,600. What amount is due to C in accordance with the partnership agreement?

Solution:

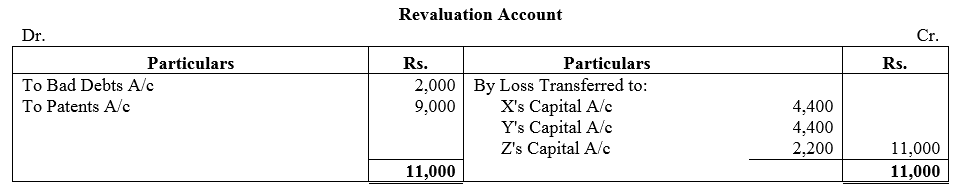

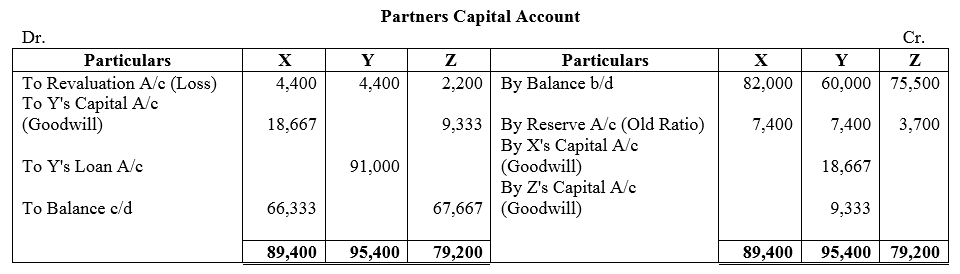

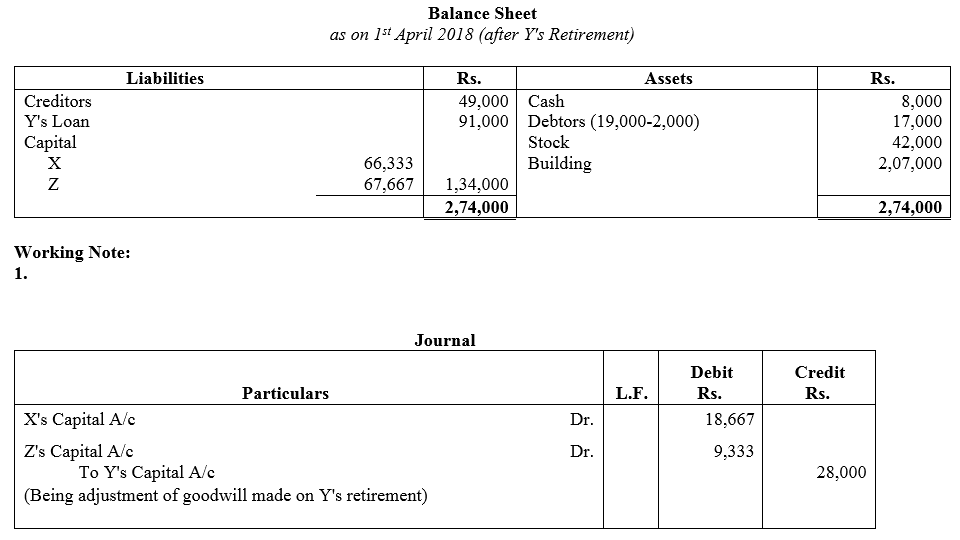

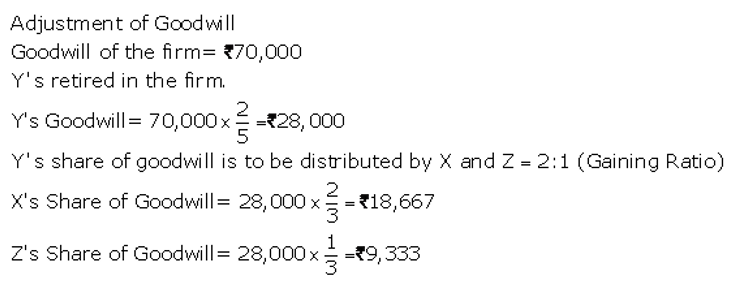

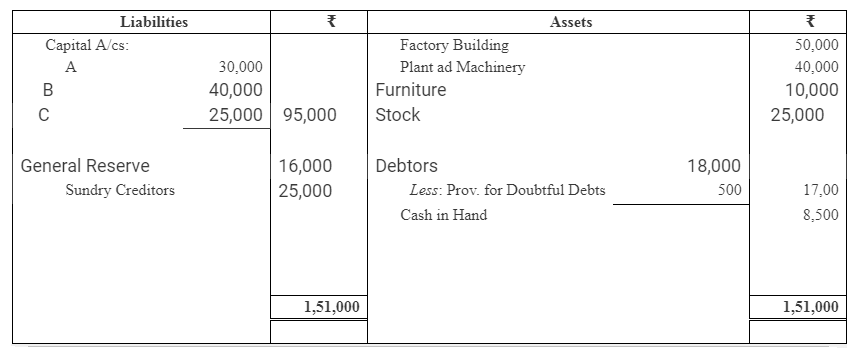

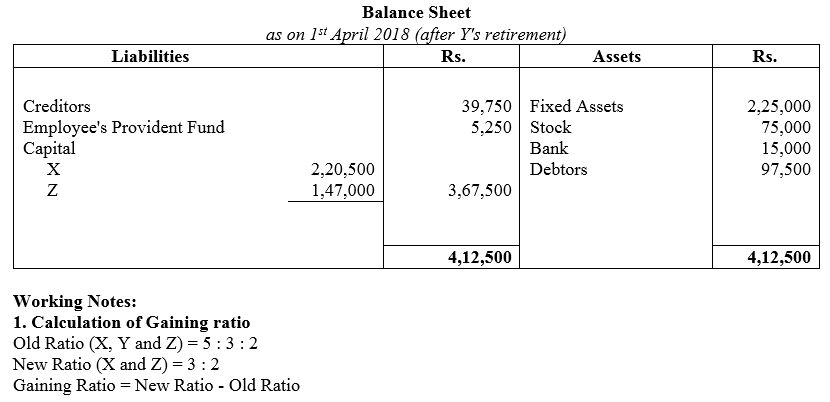

Question 34.

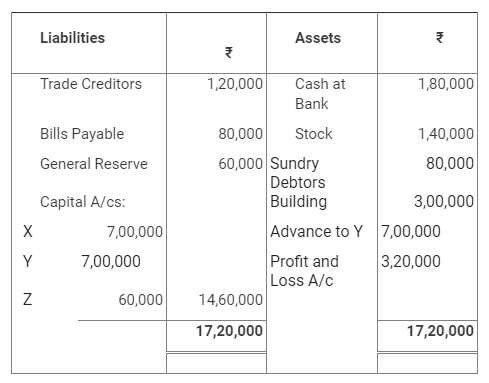

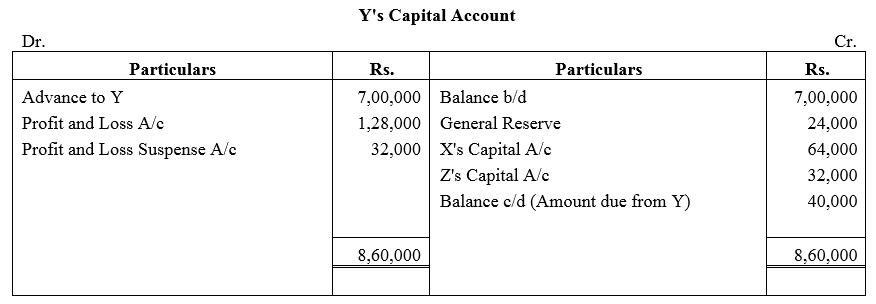

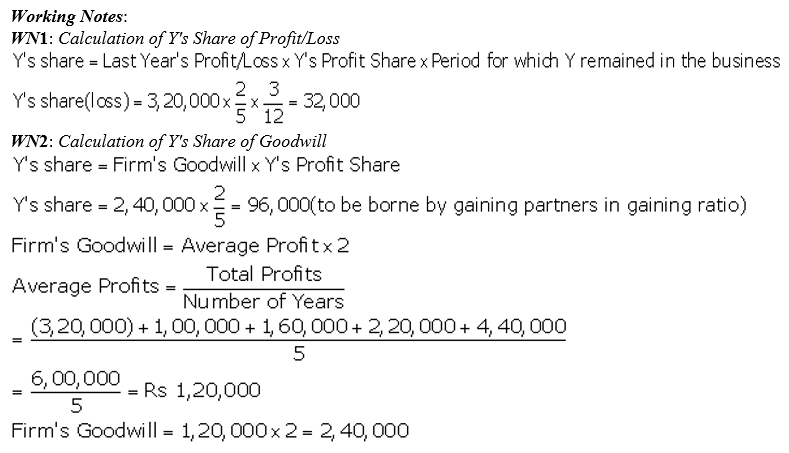

X, Y and Z were partners in a firm sharing profits in the ratio of 2 : 2 : 1. Their Balance Sheet as at 31st March, 2018 was:

Y retired on 1st April, 2018 on the following terms:

(a) Goodwill of the firm was valued at ₹ 70,000 and was not to appear in the books.

(b) Bad Debts amounted to ₹ 2,000 were to be written off.

(c) Patents were considered as valueless.

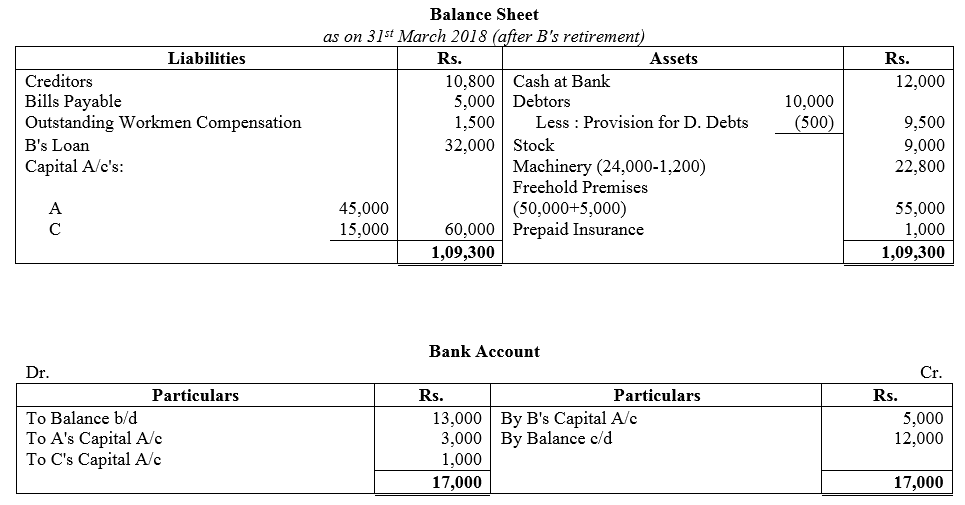

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of X and Z after Y’s retirement.

Solution:

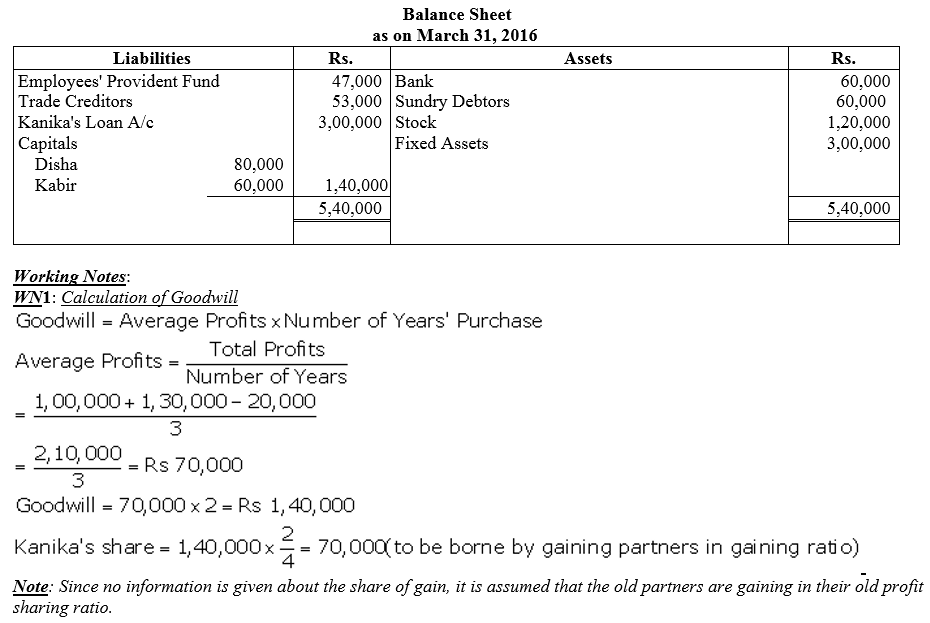

Question 35.

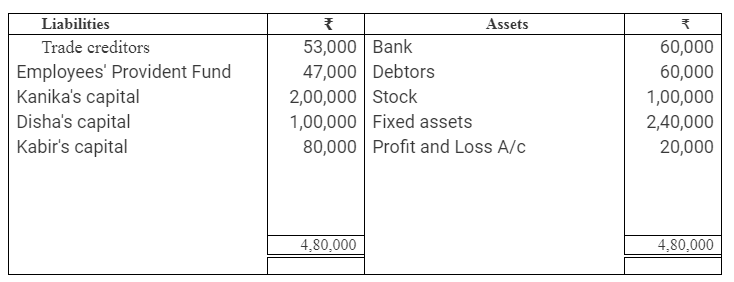

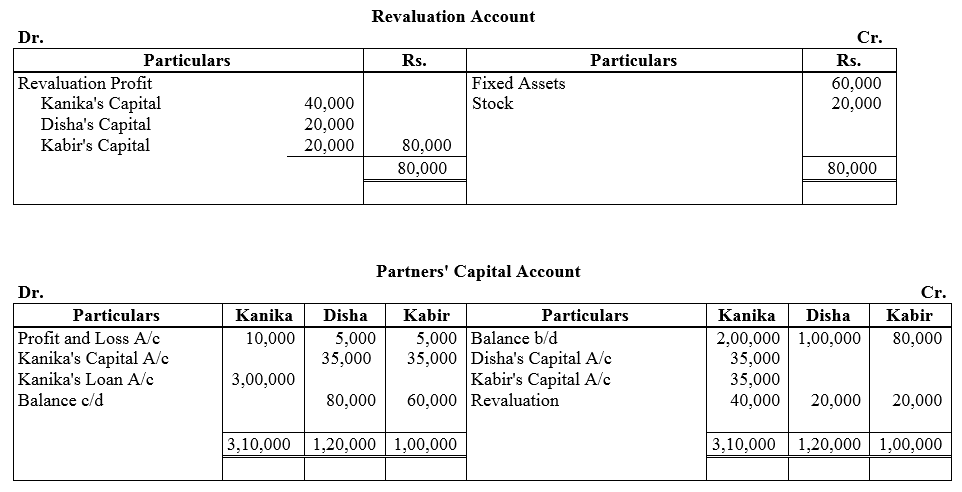

Kanika, Disha and Kabir were partners sharing profits in the ratio of 2 : 1 : 1. On 31st March, 2016, their Balance Sheet was as under:

Kanika retired on 1st April, 2016. For this purpose, the following adjustments were agreed upon:

(a) Goodwill of the firm was valued at 2 years purchase of average profits of three completed years preceding the date of retirement. The profits for the year:

2013-14 were ₹ 1,00,000 and for 2014-15 were ₹ 1,30,000.

(b) Fixed Assets were to be increased to ₹ 3,00,000.

(c) Stock was to be valued at 120%.

(d) The amount payable to Kanika was transferred to her Loan Account.

Prepare Revaluation Account, Capital Accounts of the partners and the Balance Sheet of the reconstituted firm.

Solution:

Question 36.

The Balance Sheet of X, Y and Z who were sharing profits in proportion to their capitals stood as follows at 31st March, 2018:

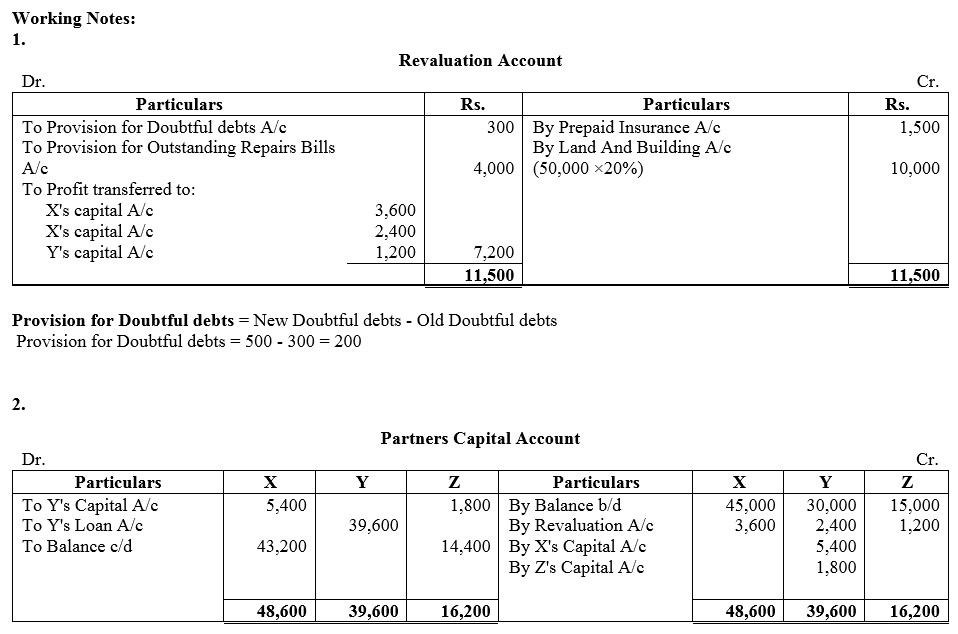

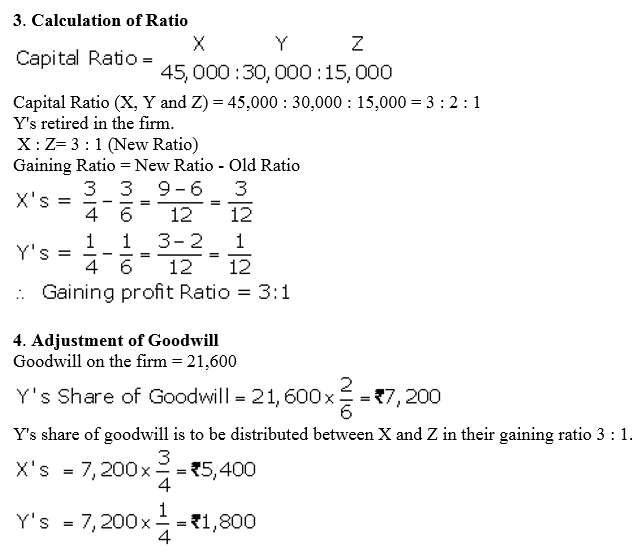

Y retires on 1st April, 2018 and the following readjustments were agreed upon:

(a) Out of insurance premium which was debited to the Profit and Loss Account ₹ 1,500 be carried forward as Unexpired Insurance.

(b) The Provision for Doubtful Debts be brought up to 5% o Debtors.

(c) The Land and Building be appreciated by 20%.

(d) A provision of ₹ 4,000 be made in respect of outstanding bills for repairs.

(e) The goodwill of the entire firm be fixed at ₹ 21,600.

Y’s share of goodwill be adjusted to that of X and Z whoa re going to share in future profits in the ratio of 3 : 1.

Pass necessary journal entries and give the Balance Sheet after Y’s retirement.

Solution:

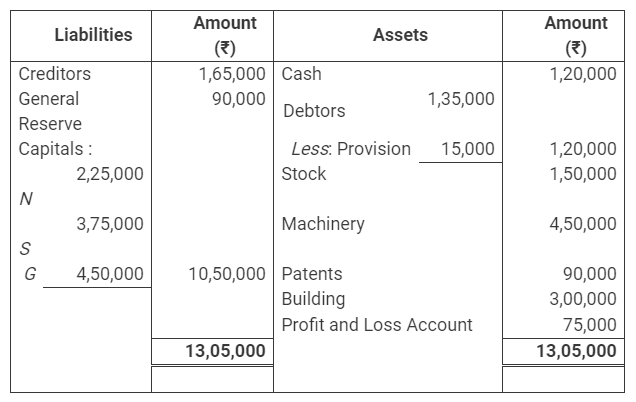

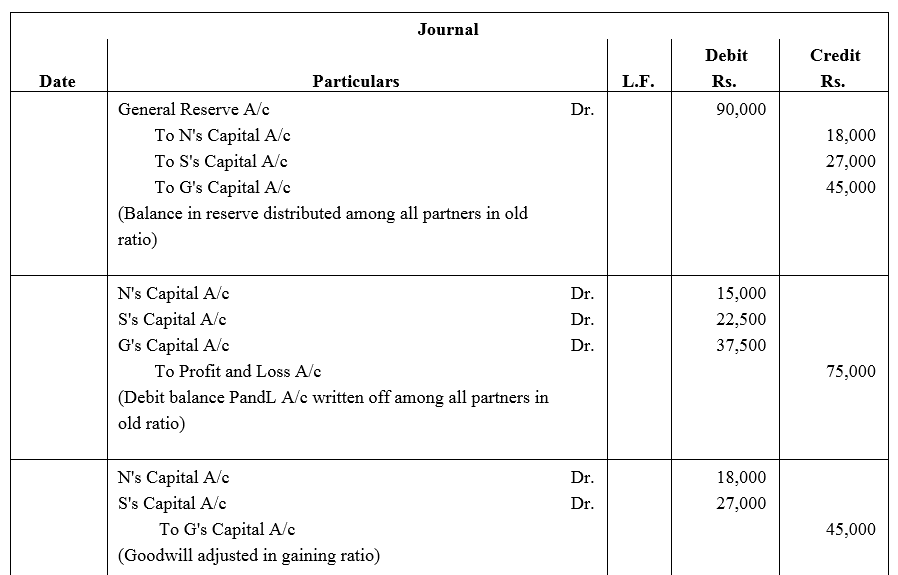

Question 37.

N, S and G were partners in a firm sharing profits and losses in the ratio of 2 : 3 : 5. On 31st March, 2016 their Balance Sheet was as under:

G retired on the above ate and it was agreed that:

(a) Debtors of ₹ 6,000 will be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts will be maintained.

(b) Patents will be completely written off and stock, machinery and building will be depreciated by 5%.

(c) An unrecorded creditor of ₹ 30,000 will be taken into account.

(d) N and S will share the future profits in 2 : 3 ratio.

(e) Goodwill of the firm on G’s retirement was valued at ₹ 90,000.

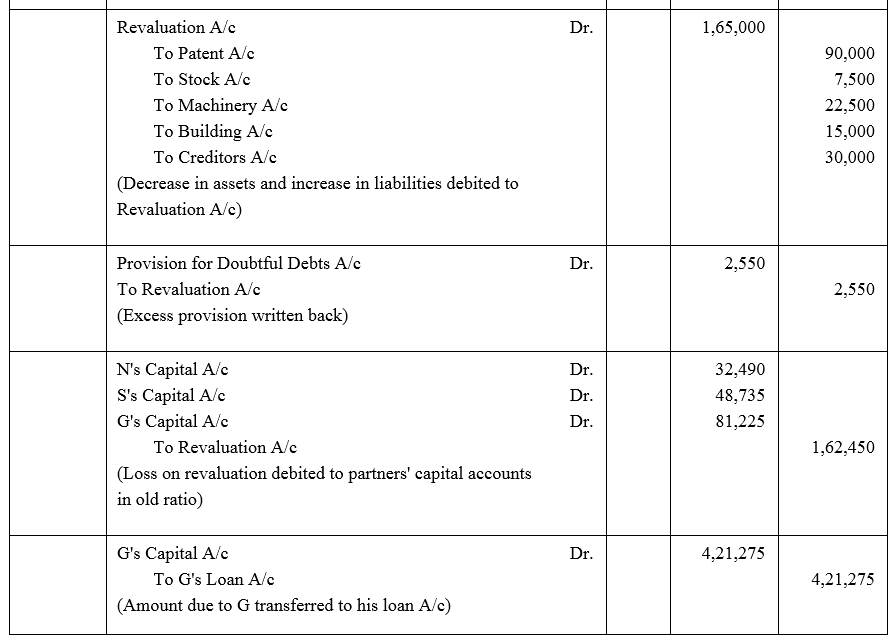

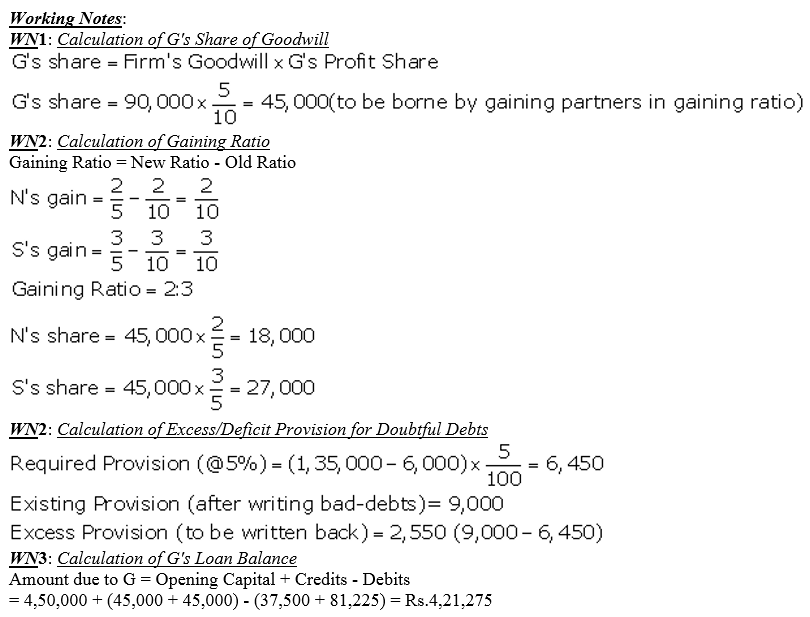

Pass necessary journal entries for the above transactions in the books of the firm on G’s retirement.

Solution:

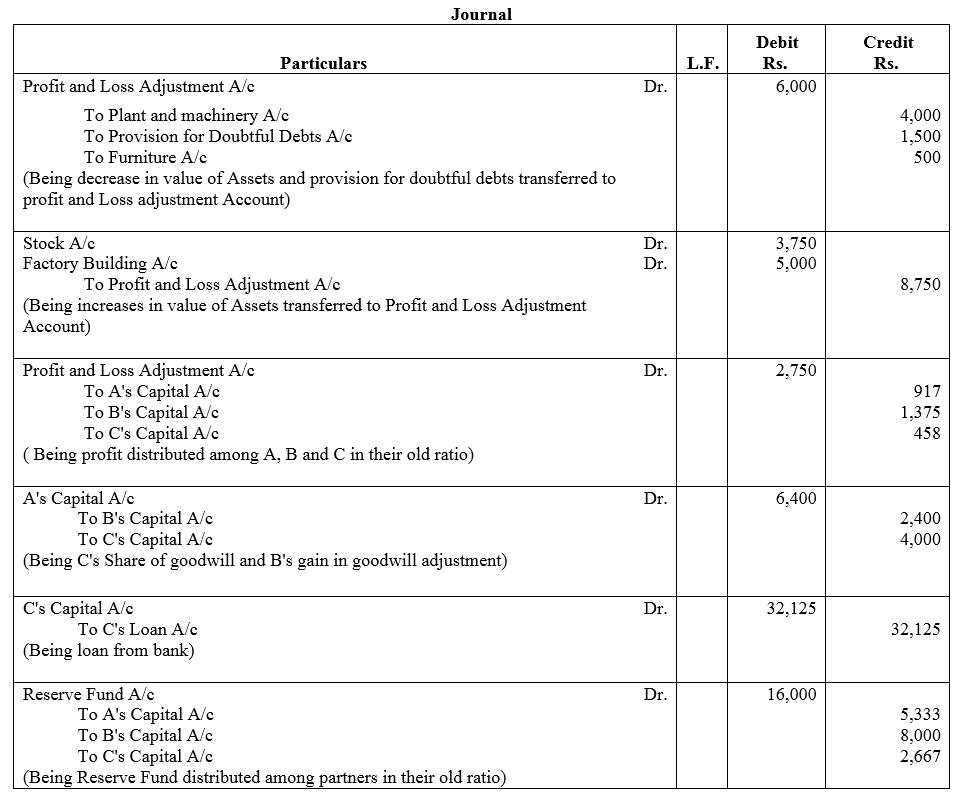

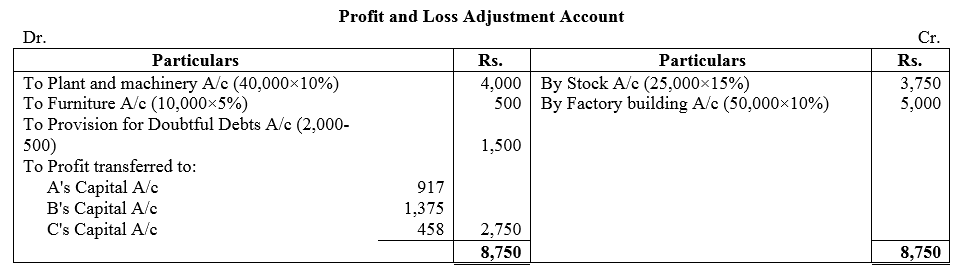

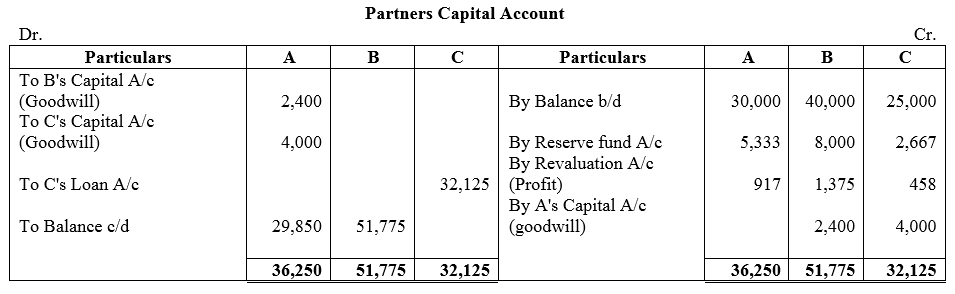

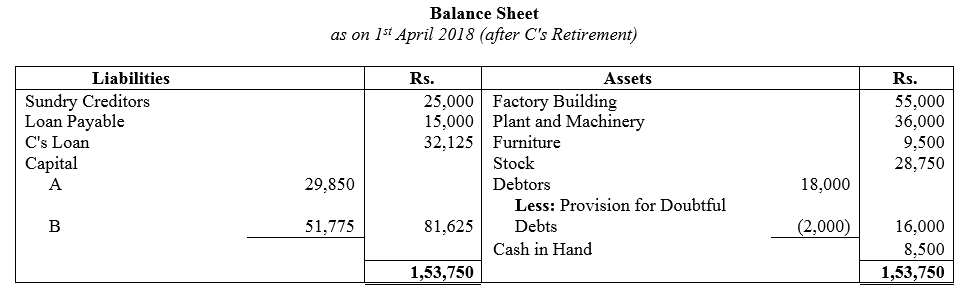

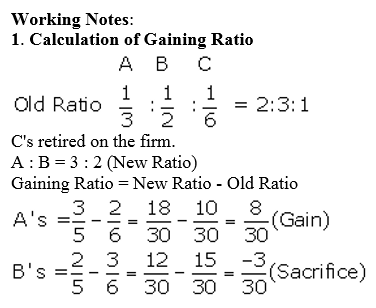

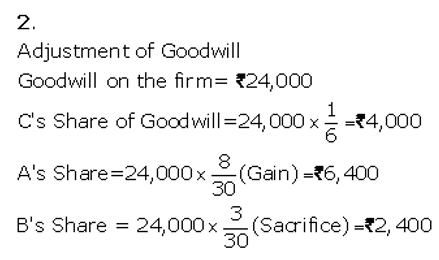

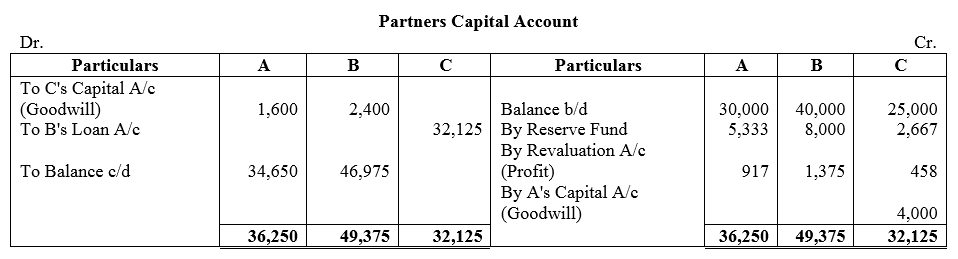

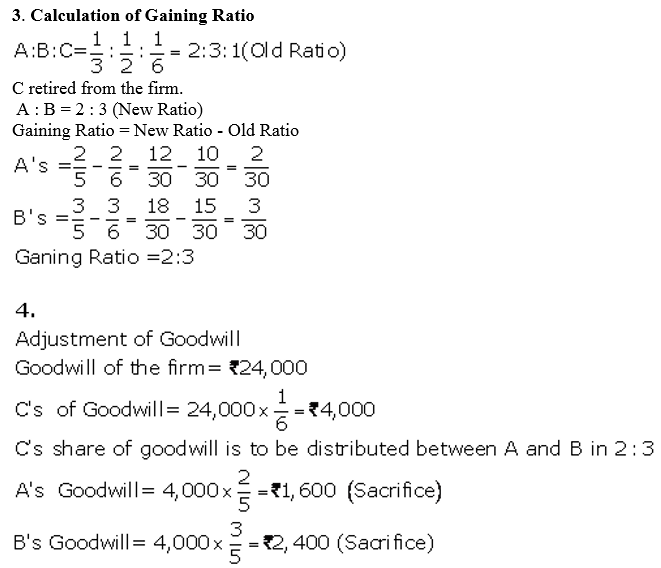

Question 38.

A, B and C are partners in a firm, sharing profits and losses as A 1/3, B 1/2 and C 1/6 respectively. The Balance Sheet of the firm as at 31st March, 2018 was:

C retires on 1st April, 2018 subject to the following adjustments:

(a) Goodwill of the firm be valued at ₹ 24,000. C’s share of goodwill be adjusted into the account of A and B who are going to share in future in the ratio of 3 : 2.

(b) Plant and Machinery to be depreciated by 10% and Furniture by 5%.

(c) Stock to be appreciated by 15% and Factory Building by 10%.

(d) Provision for Doubtful Debts to be raised to ₹ 2,000.

You are required to pass journal entries to record the above transactions in the books of the firm and show the Profit and Loss Adjustment Account, Capital Account of C and the Balance Sheet of the firm after C’s retirement.

Solution:

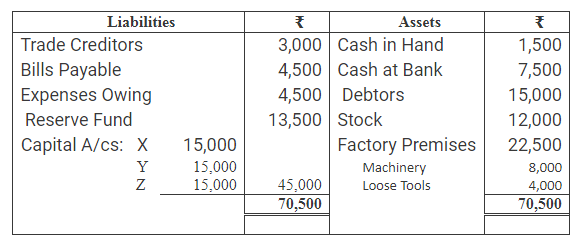

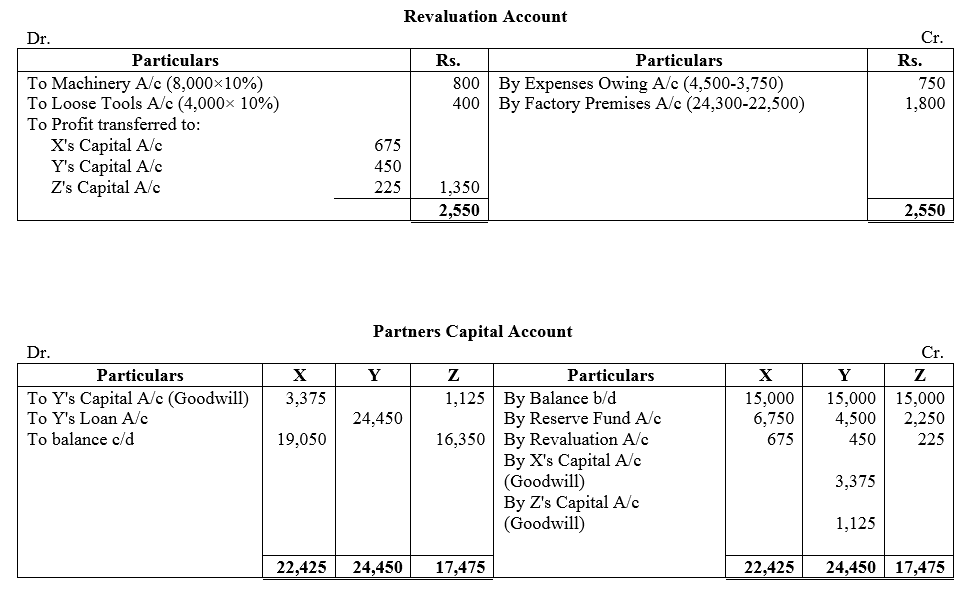

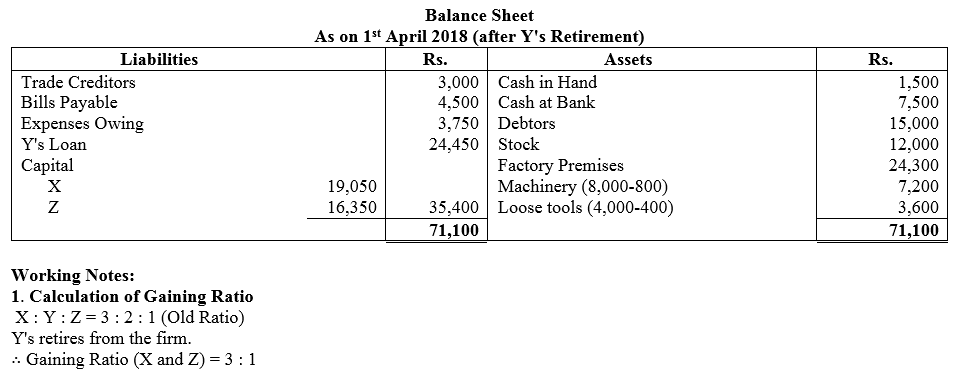

Question 39.

X, Y and Z were in partnership sharing profits and losses in the proportions of 3 : 2 : 1. On 1st April, 2018 Y retires from the firm. On that date, their Balance Sheet was:

The terms were:

(a) Goodwill of the firm was valued at ₹ 13,500 and adjustment in this respect was to be made in the continuing Partners Capital Accounts without raising Goodwill Account.

(b) Expenses Owing to be brought down to ₹ 3,750.

(c) Machinery and Loose Tools are to be valued @ 10% less than their book value.

(d) Factory Premises are to be revalued at ₹ 24,300.

Show Revaluation Account, Partners Capital Accounts and prepare the Balance Sheet of the firm after the retirement of Y.

Solution:

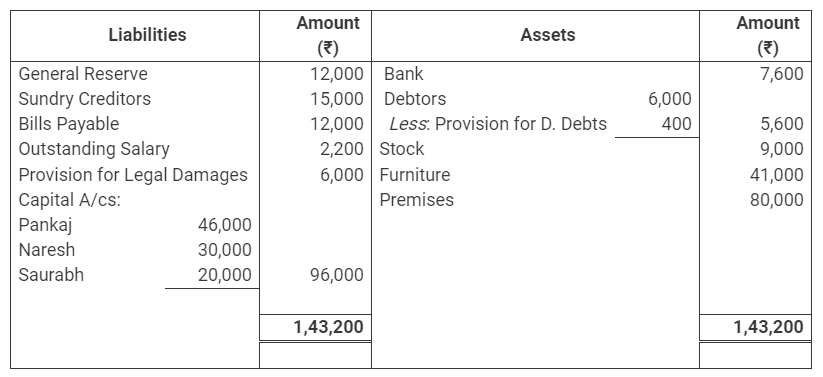

Question 40.

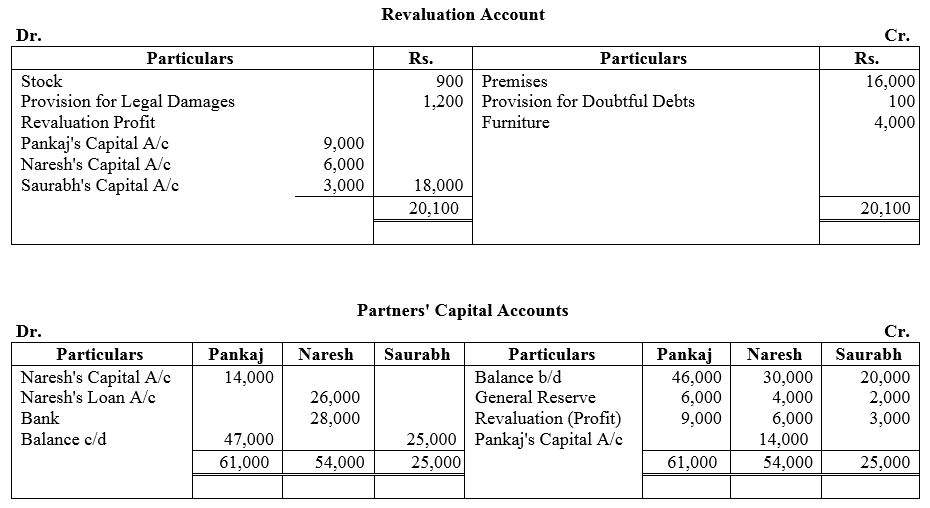

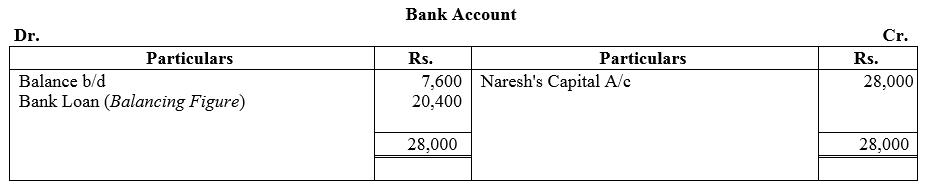

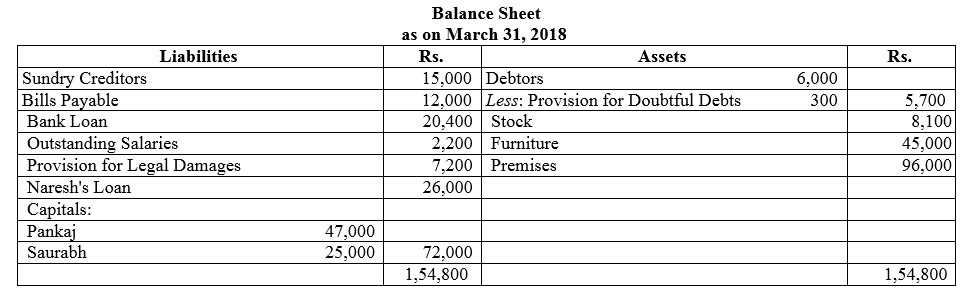

Pankaj, Naresh and Saurabh are partners sharing profits in the ratio of 3 : 2 : 1. On 31st March, 2018, Naresh retired from the firm due to his illness. On that date, Balance Sheet of the firm was as follows:

Additional Information:

(a) Premises have appreciated by 20%, stock depreciated by 10% and provision for doubtful debts was to be made 5% on debtors. Further provision for legal damages is to be made for ₹ 1,200 and furniture to be brought up to ₹ 45,000.

(b) Goodwill of the firm be valued at ₹ 42,000.

(c) ₹ 26,000 from Naresh’s Capital Account be transferred to his Loan Account and balance be paid through bank: if required, necessary loan may be obtained from bank.

(d) New profit-sharing ratio of Pankaj and Saurabh is decided to be 5 : 1.

Give the necessary Ledger Accounts and Balance Sheet of the firm after Naresh’s retirement.

Solution:

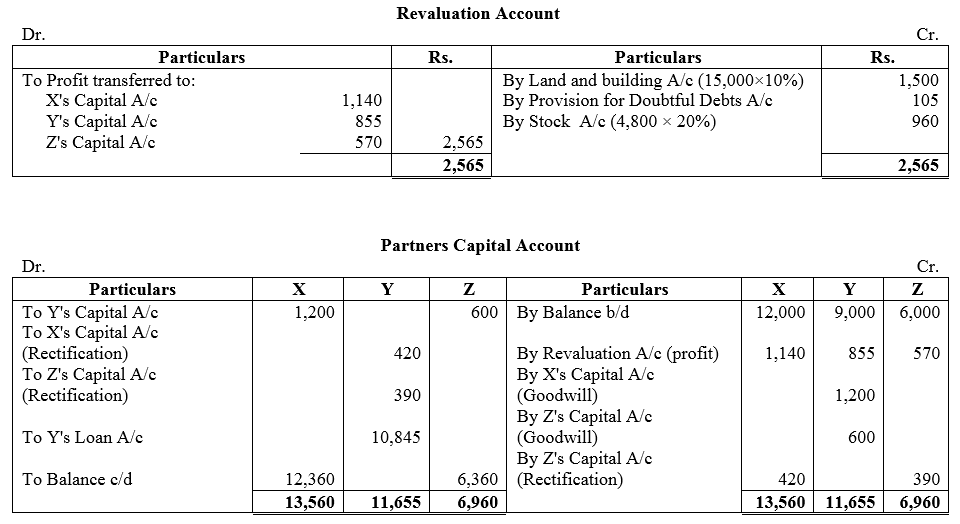

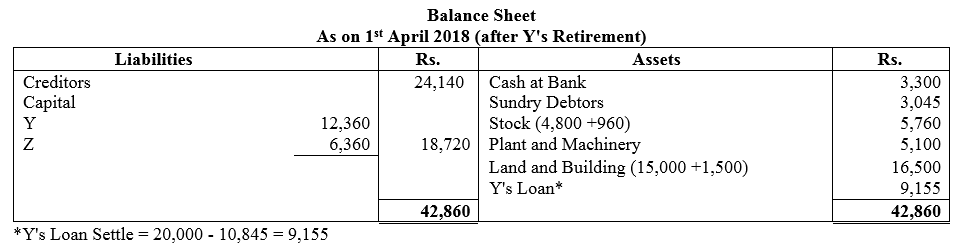

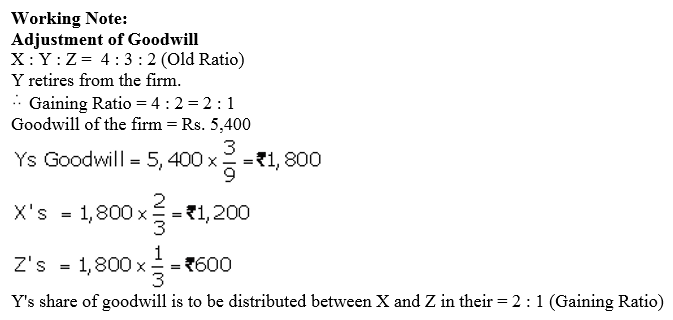

Question 41.

X, Y and Z are partners sharing profits in the ratio of 4 : 3 : 2. Their Balance Sheet as at 31st March, 2018 stood as follows:

Y having given notice to retire from the firm, the following adjustments in the books of the firm were agreed upon:

(a) That the Land and Building be appreciated by 10%.

(b) That the Provision for Doubtful Debts is no longer necessary since all the debtors are considered good.

(c) That the stock be appreciated by 20%.

(d) That the adjustment be made in the accounts to rectify a mistake previously committed whereby Y was credited in excess by ₹ 810, while X and Z were debited in excess of ₹ 420 and ₹ 390 respectively.

(e) Goodwill of the firm be fixed at ₹ 5,400 and Y’s share of the same be adjusted to that of X and Z who were going to share in the ratio of 2 : 1.

(f) It was decide by X and Y to settle Y’s account immediately on his retirement.

You are required to show:

(i) Revaluation Account

(ii) Partner’s Capital Accounts and

(iii) Balance Sheet of the firm after Y’s retirement.

Solution:

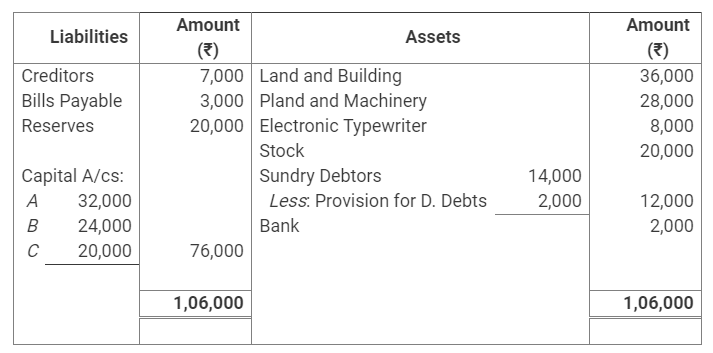

Question 42.

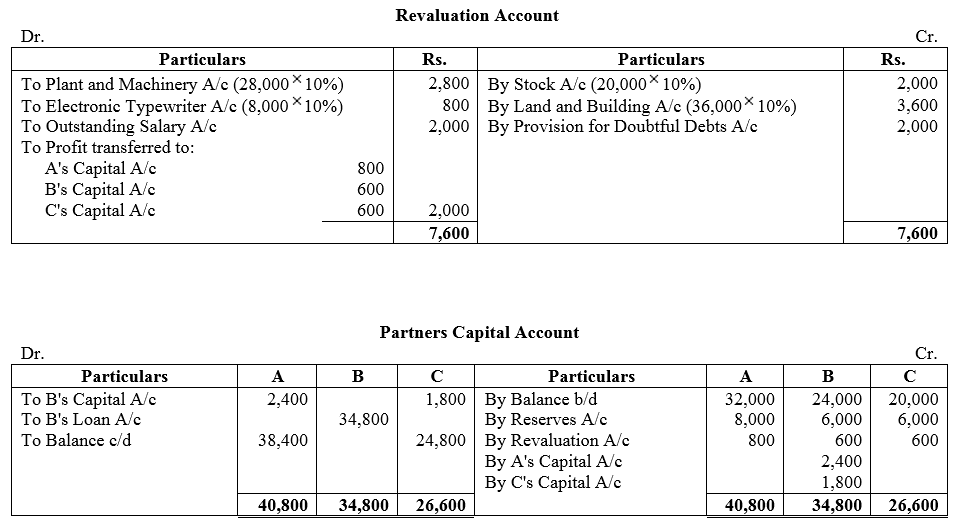

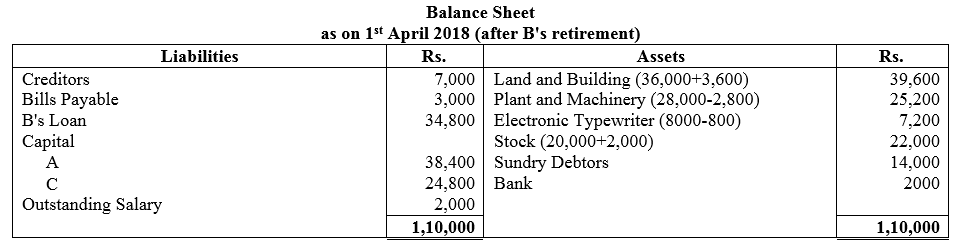

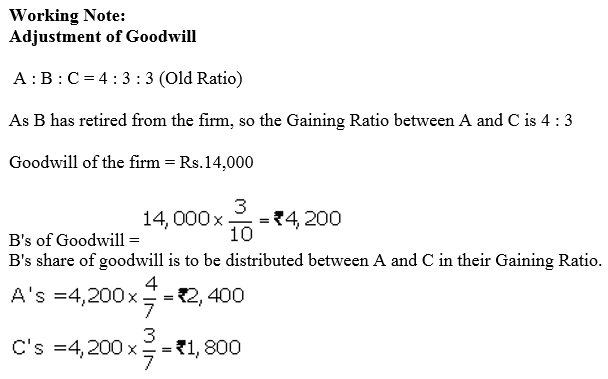

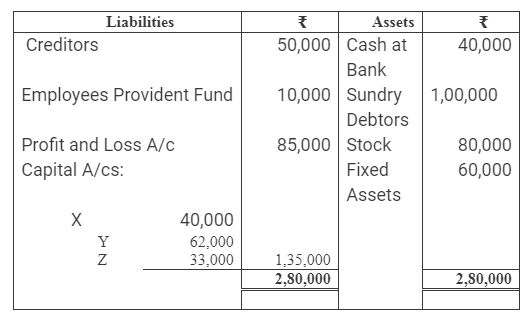

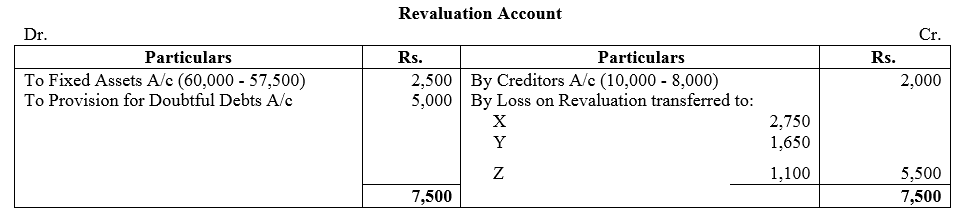

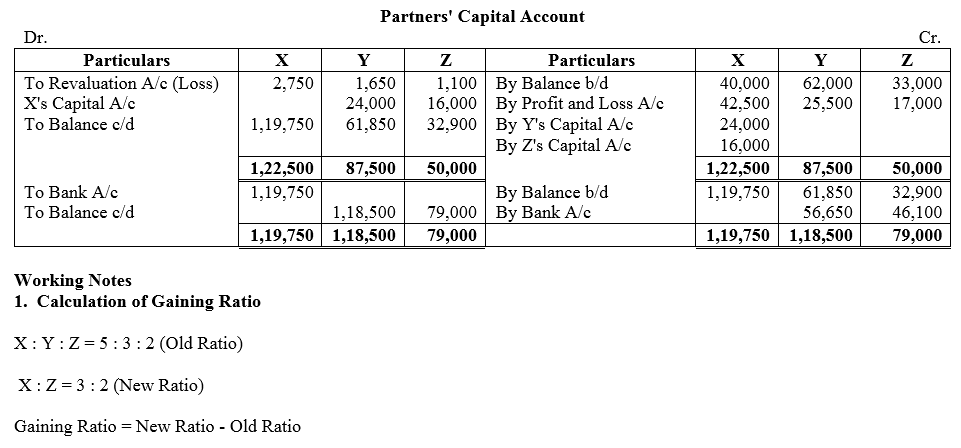

A, B and C are partners sharing profits and losses in the ratio of 4 : 3 : 3 respectively. Their Balance Sheet as at 31st March, 2018 is:

On 1st April, 2018, B retires from the firm on the following terms:

(a) Goodwill of the firm is to be valued at ₹ 14,000.

(b) Stock, Land and Building are to be appreciated by 10%.

(c) Plant and Machinery and Electronic Typewriter are to be depreciated by 10%.

(d) Sundry Debtors are considered to be good.

(e) There is a liability of ₹ 2,000 for the payment of outstanding salary to the employee of the firm. This liability has not been shown in the above Balance Sheet but the same is to be recorded now.

(f) Amount payable to B is to be transferred to his Loan Account.

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of A and C after B’s retirement.

Solution:

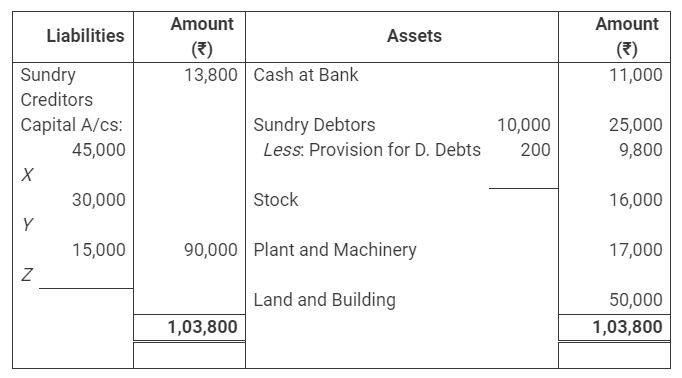

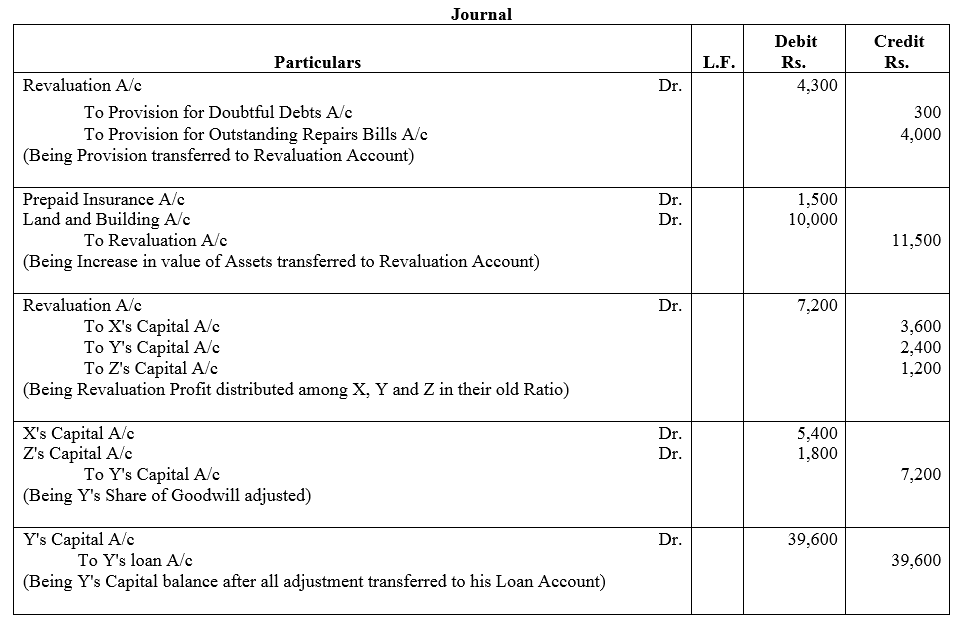

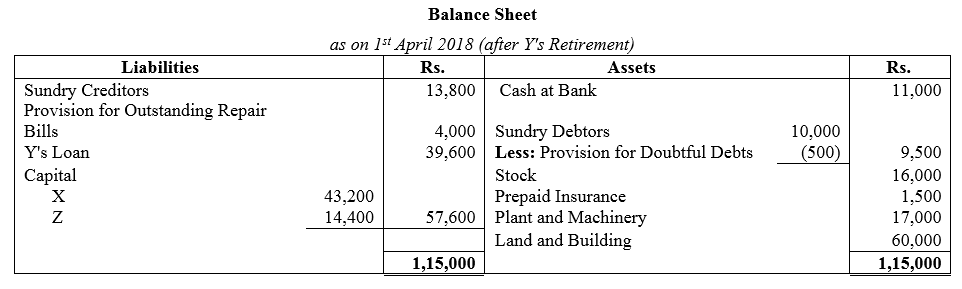

Question 43.

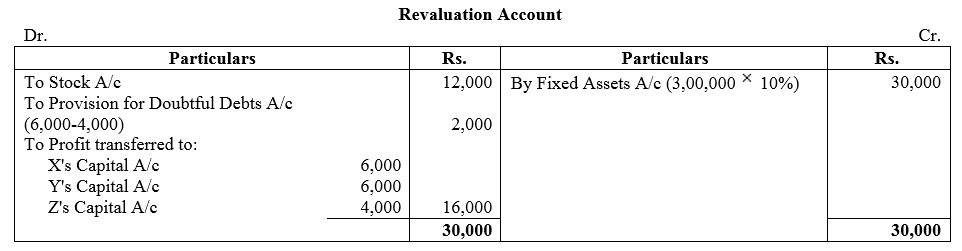

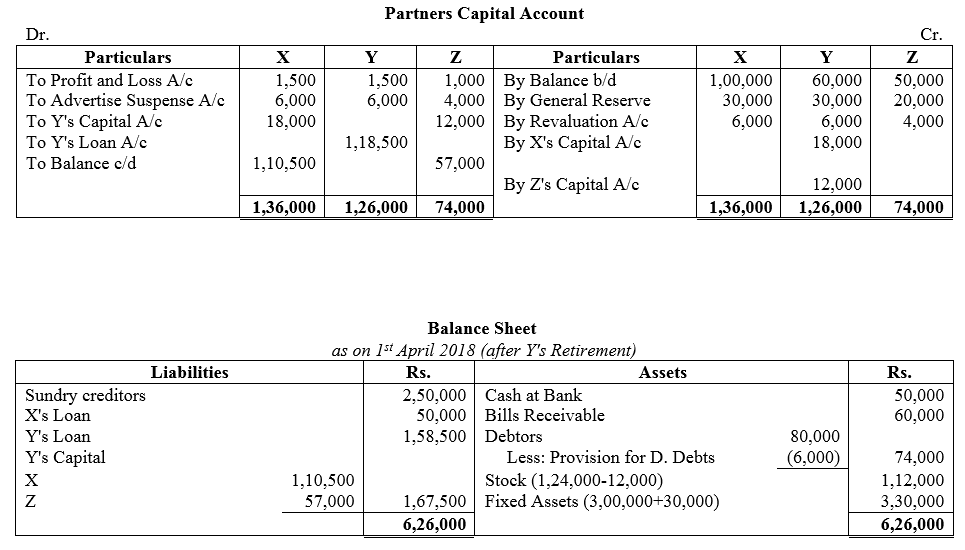

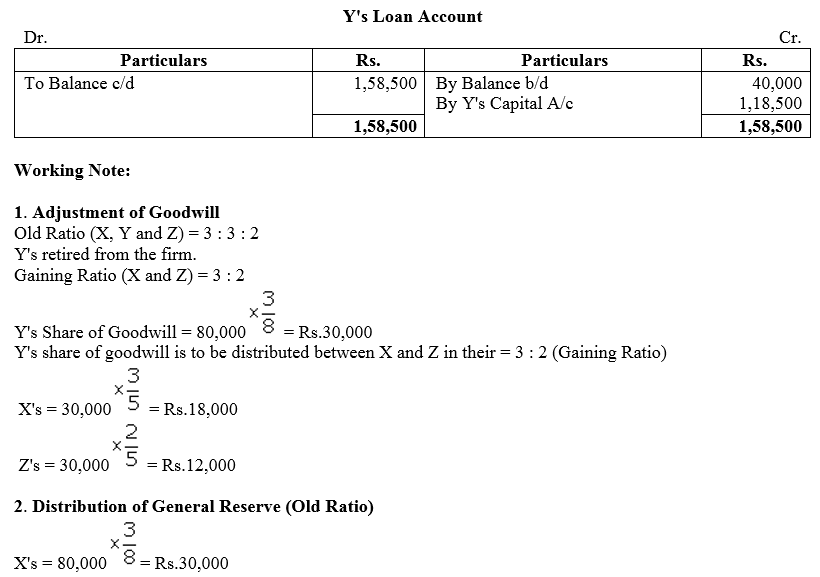

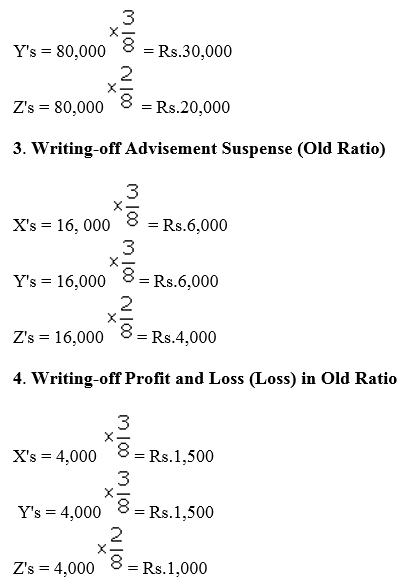

Following is the Balance Sheet of X, Y and Z as at 31st March, 2018. They shared profits in the ratio of 3 : 3 : 2.

On 1st April, 2018, Y decided to retire from the firm on the following terms:

(a) Stock to be depreciated by ₹ 12,000.

(b) Advertisements Suspense Account to be written off.

(c) Provision for Doubtful Debts to be increased to ₹ 6,000.

(d) Fixed Assets be appreciated by 10%.

(e) Goodwill of the firm, valued at ₹ 80,000 and the amount due to the retiring partners to be adjusted in X’s and Z’s Capital Accounts.

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet to give effect to the above.

Solution:

Question 44.

X, Y and Z are partners sharing profits and losses in the ratio of 3 : 2 : 1. The Balance Sheet of the firm as at 31st March, 2018 stood as follows:

Z retired on the above date on the following terms:

(a) Goodwill of the firm is to be valued at ₹ 34,800.

(b) Value of Patents is to be reduced by 20% and that of machinery to 90%.

(c) Provision for Doubtful Debts is to be created @ 6% on debtors.

(d) Z took over the investment at market value.

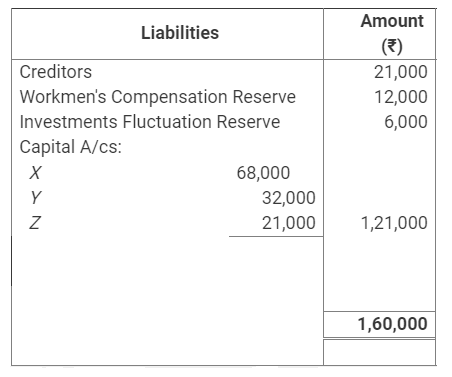

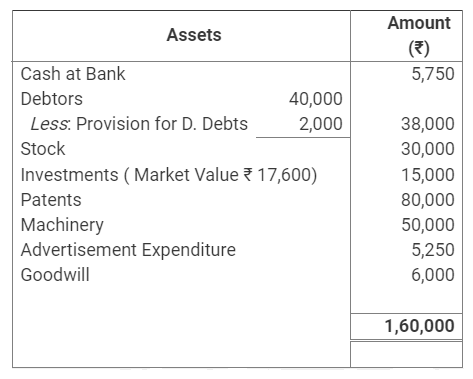

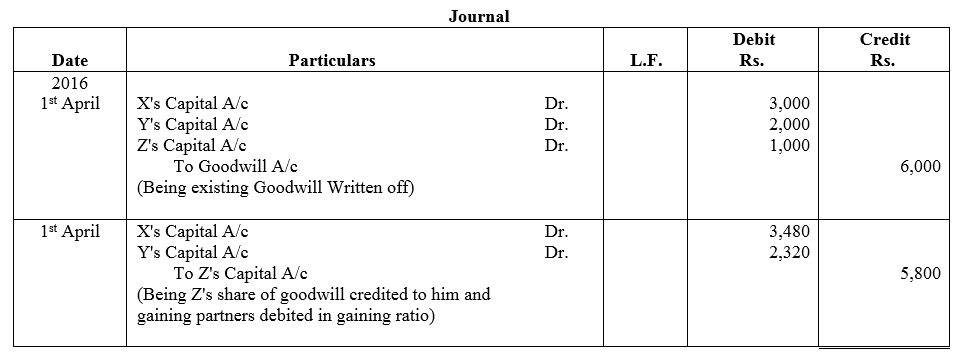

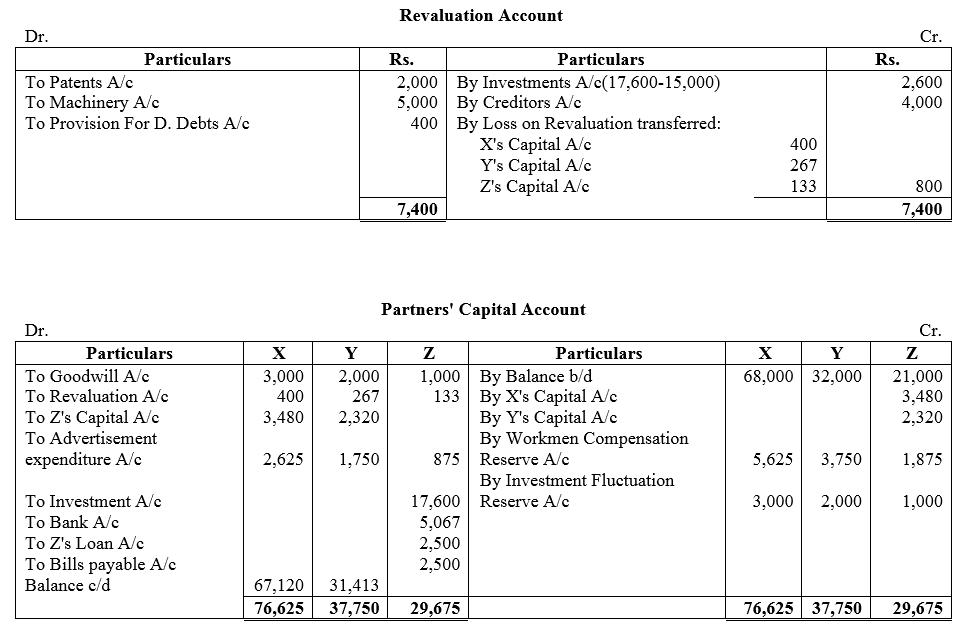

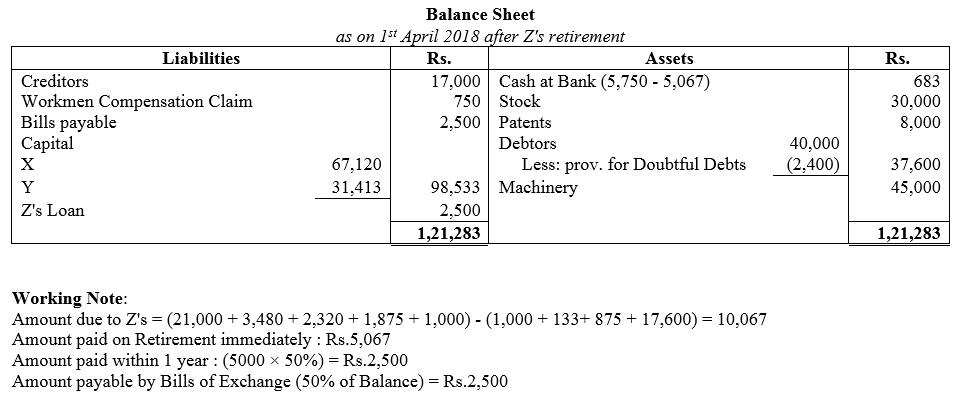

(e) Liability for Workmen Compensation to the extent of ₹ 750 is to be created.

(f) A liability of ₹ 4,000 included in creditors is not to be paid.

(g) Amount due to Z to be settled on the following basis:

₹ 5,067 to be paid immediately, 50% of the balance within one year and the balance by a Bill of Exchange (without interest) at 3 Months.

Give necessary journal entries for the treatment of goodwill, prepare Revaluation Account, Capital Accounts and the Balance Sheet of the new firm.

Solution:

Question 45.

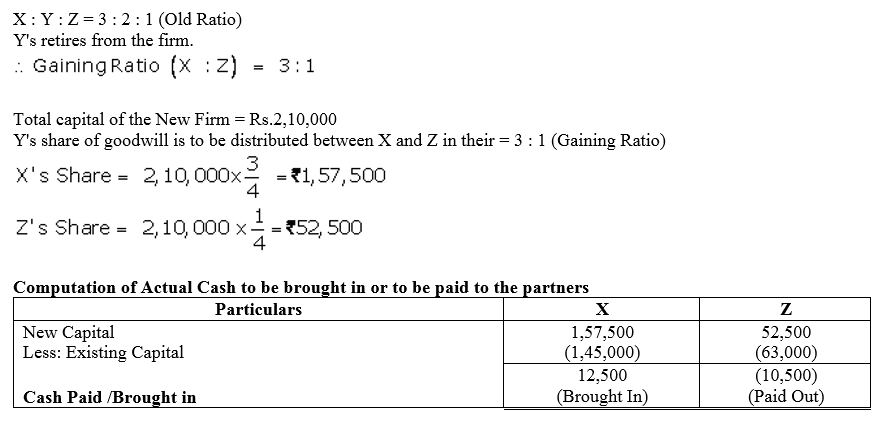

X, Y and Z are partners in a firm sharing profits in the ratio of 3 : 2 : 1. On 1st April, 2009, Y retires from the firm. X and Z agree that the capital of the new firm shall be fixed at ₹ 2,10,000 in the profit-sharing ratio. The Capital Accounts of X and Z after all adjustments on the date of retirement showed balance of ₹ 1,45,000 and ₹ 63,000 respectively. State the amount of actual cash to be brought in or to be paid to the partners.

Solution:

Question 46.

On 31st March, 2018 , The Balance Sheet of A, B and C who were sharing profits and losses in proportion to their capitals stood as:

B retires and following readjustments of assets and liabilities have been agreed upon before ascertainment of the amount payable to B:

(a) Out of the amount of insurance premium which was debited to Profit and Loss Account, ₹ 1,000 be carried forward for Unexpired insurance.

(b) Freehold Premises be appreciated by 10%.

(c) Provision for Doubtful Debts is brought up to 5% on Debtors.

(d) Machinery be depreciated by 5%.

(e) Liability for Workmen Compensation to the extent of ₹ 1,500 would be created.

(f) That the goodwill of the entire firm be fixed at ₹ 18,000 and B’s share of the same be adjusted into the accounts of A and C who are going to share future profits in the proportion of 3/4th and 1/4th respectively.

(g) Total capital of the firm as newly constituted be fixed at ₹ 60,000 between A and C in the proportion of 3/4th and 1/4th after passing entries in their accounts for adjustments, i.e., actual cash to be paid or to be brought in by continuing partners as the case may be.

(h) B be paid ₹ 5,000 in cash and the balance be transferred to his Loan Account.

Prepare Capital Accounts of Partners and the Balance Sheet of the firm of A and C.

Solution:

Question 47.

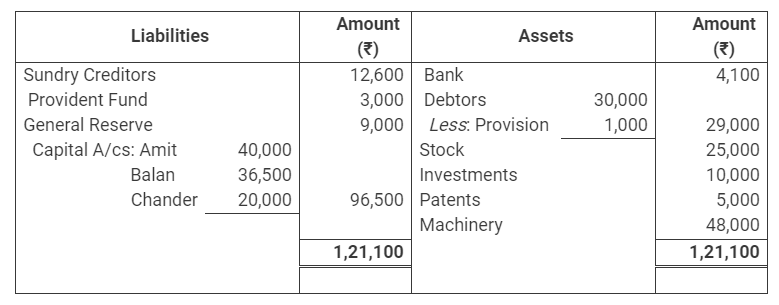

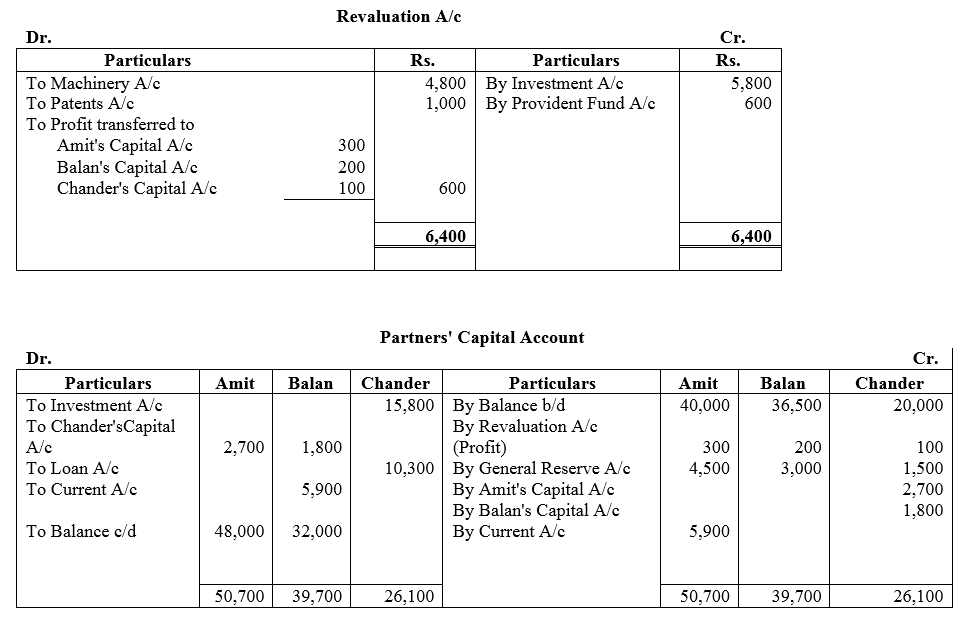

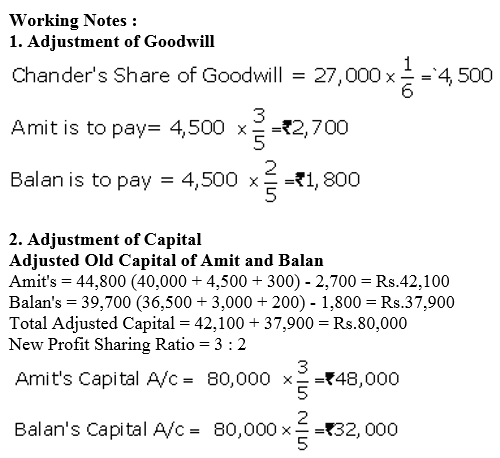

Amit, Balan and Chander were partners in a firm sharing profits in the proportion of 1/2, 1/3 and 1/6 respectively. Chander retired on 1st April, 2014. The Balance Sheet of the firm on the date of Chander’s retirement was as follows:

It was agreed that:

(i) Goodwill be valued at ₹ 27,000.

(ii) Depreciation of 10% was to be provided on Machinery.

(iii) Patents were to be reduced by 20%.

(iv) Liability on account of Provident Fund was estimated at ₹ 2,400.

(v) Chander took over Investments for ₹ 15,800.

(vi) Amit and Balan decided to adjust their capitals in proportion of their profit-sharing ratio by opening Current Accounts.

Prepare Revaluation Account and Partners Capital Accounts on Chander’s retirement.

Solution:

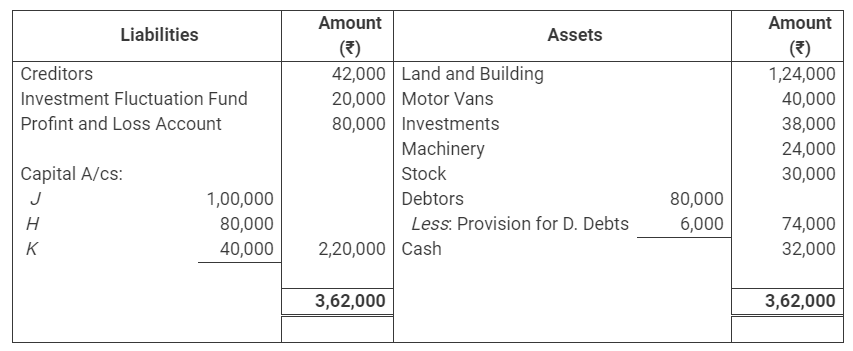

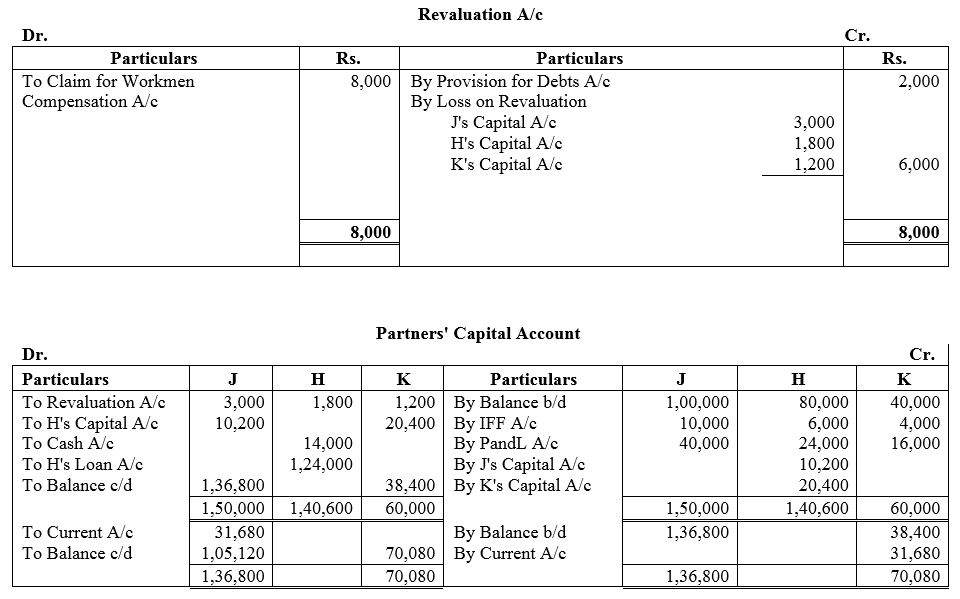

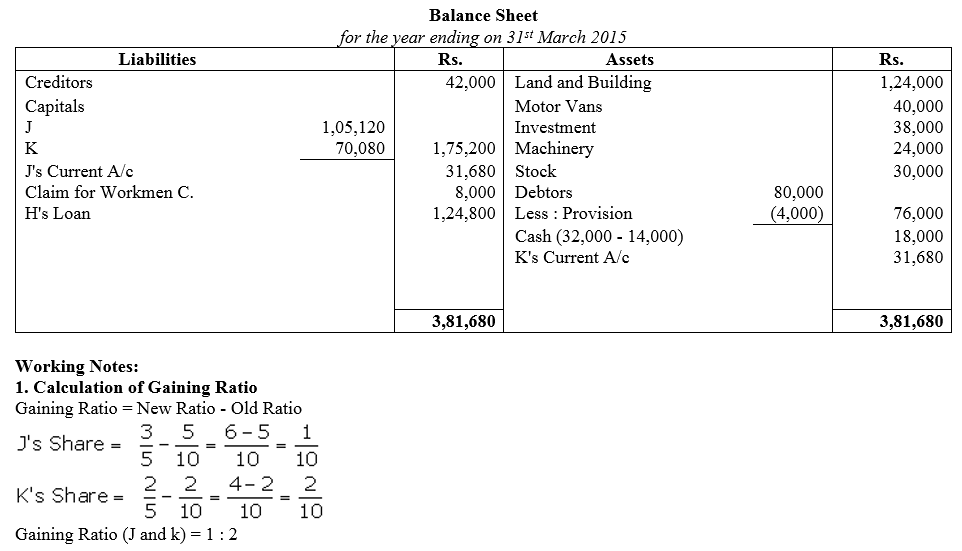

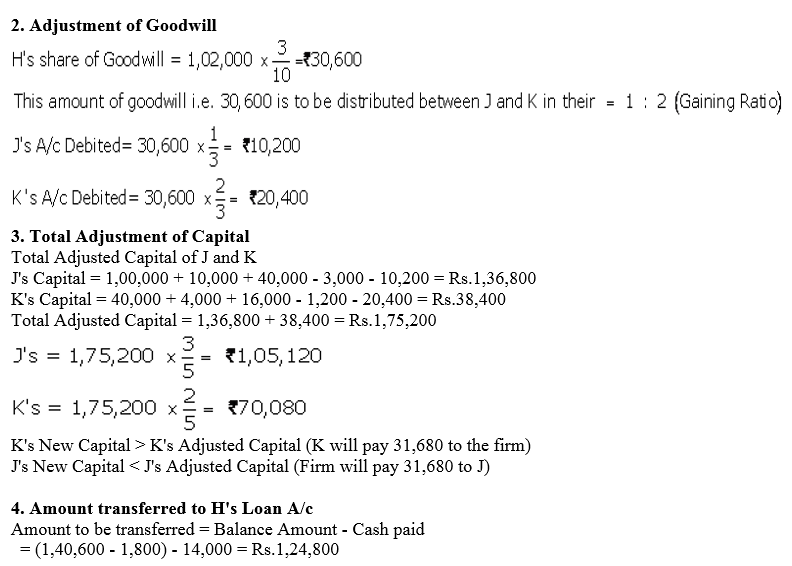

Question 48.

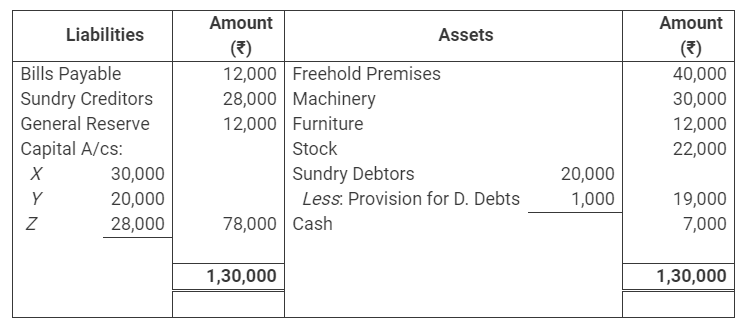

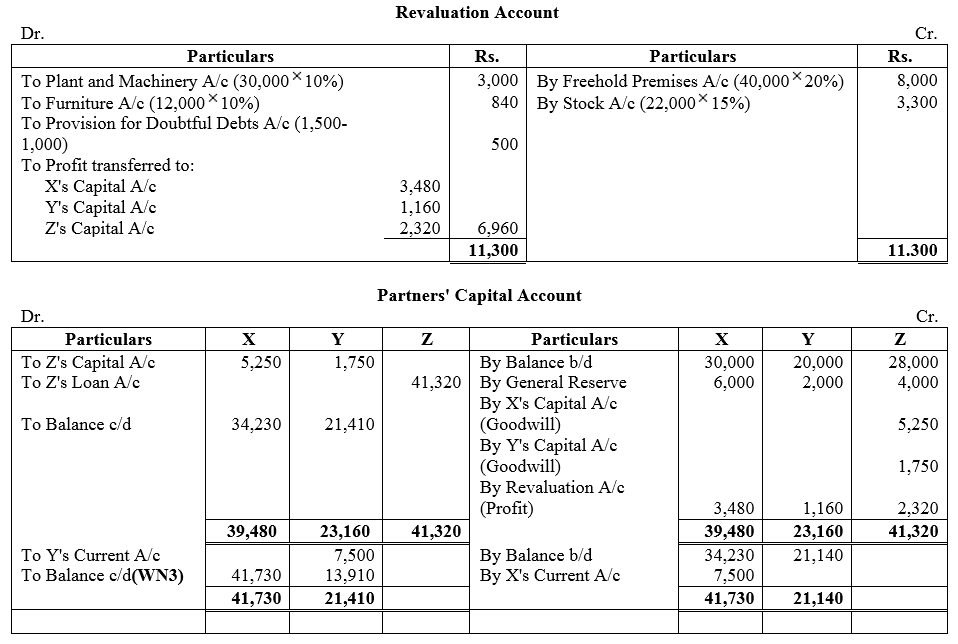

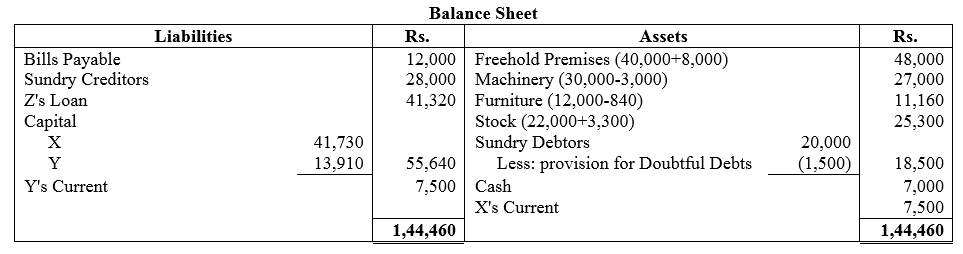

J, H and K were partners in a firm sharing profits in the ratio of 5 : 3 : 2. On 31st March, 2015, their Balance Sheet was as follows:

On the above date, H retired and J and K agreed to continue the business on the following terms:

(i) Goodwill of the firm was valued at ₹ 1,02,000.

(ii) There was a claim of ₹ 8,000 for workmen’s compensation.

(iii) Provision for bad debts was to be reduced by ₹ 2,000.

(iv) H will be paid ₹ 14,000 in cash and balance will be transferred in his Loan Account which will be paid in four equal yearly installments together with interest @ 10% p.a.

(v) The new profit-sharing ratio between J and K will be 3 : 2 and their capitals will be in their new profit-sharing ratio. The capital adjustments will be done by opening Current Accounts.

Prepare Revaluation Account, Partners Capital Accounts and Balance Sheet of the new firm.

Solution:

Question 49.

X, Y and Z are partners in a firm sharing profits in the ratio of 3 : 1 : 2. On 31st March, 2018, their Balance Sheet was:

Z retires from the business and the partners agree to the following:

(a) Freehold Premises and Stock are to be appreciated by 20% and 15% respectively.

(b) Machinery and Furniture are to be depreciated by 10% and 7% respectively.

(c) Provision for Doubtful Debts is to be increased to ₹ 1,500.

(d) Goodwill of the firm is valued at ₹ 21,000 on Z’s retirement.

(e) The continuing partners have decided to adjust their capitals in their new profit-sharing ratio after retirement of Z. Surplus/deficit, if any, in their Capital Accounts will be adjusted through Current Accounts.

Prepare necessary Ledger Accounts and draw the Balance Sheet of the reconstituted firm.

Solution:

Question 50.

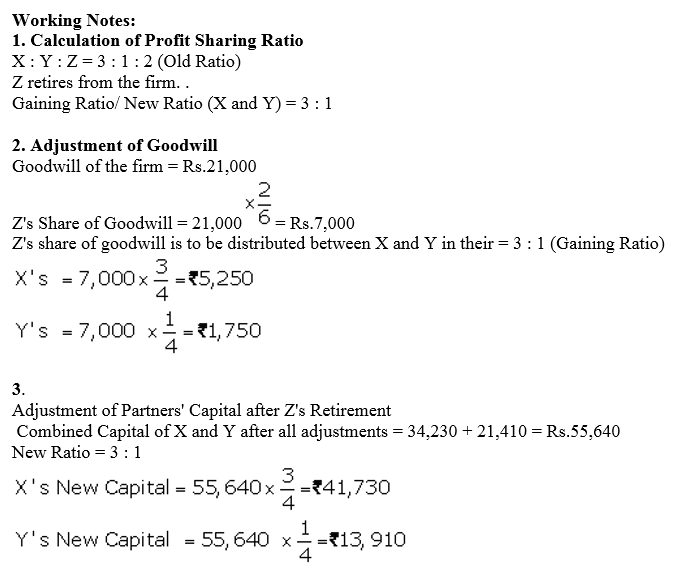

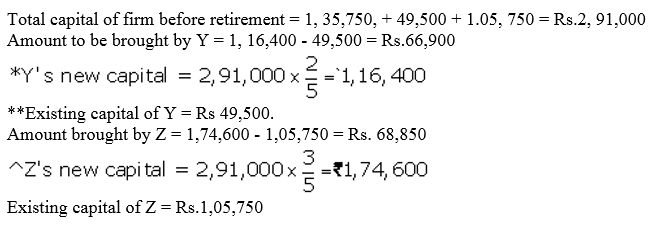

X, Y and Z are partners sharing profits in the ratio of 5 : 3 : 7. X retires from the firm. Y and Z decided to share future profits in the ratio of 2 : 3. The adjusted Capital Accounts of Y and Z showed balance of ₹ 49, 500 and ₹ 1,05,750 respectively. The total amount to be paid to X is ₹ 1,35,750. This amount is to be paid by Y and Z in such a way that their capitals become proportionate to their new profit-sharing ratio. Calculate the amount to be brought in or to be paid to partners.

Solution:

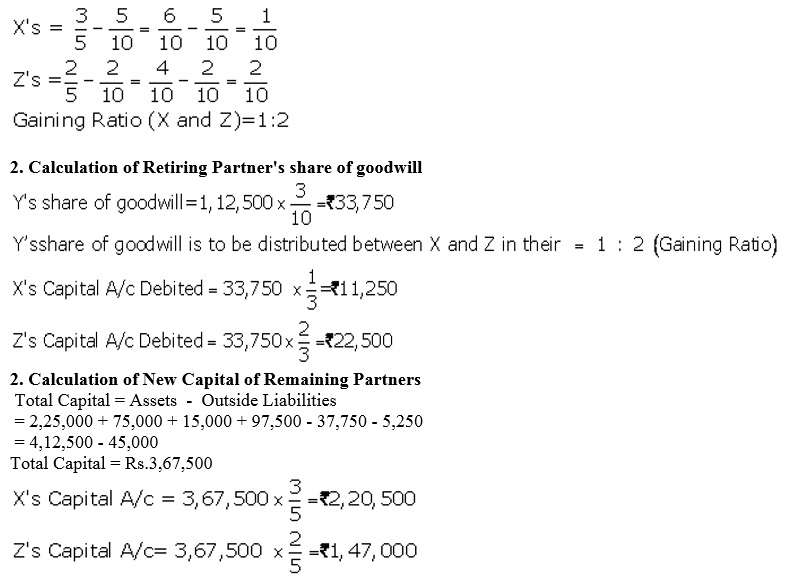

Question 51.

The Balance Sheet of X, Y and Z who shared profits in the ratio of 5 : 3 : 2 as on 31st March, 2018 was as follows:

Y retired on the above date and it was agreed that:

(i) Goodwill of the firm is valued at ₹ 1,12,500 and Y’s share of it be adjusted into the accounts of X and Z who are going to share future profits in the ratio of 3 : 2.

(ii) Fixed Assets be appreciated by 20%.

(iii) Stock be reduced to ₹ 75,000.

(iv) Y be paid amount brought in by X and Z in such a way as to make their capitals proportionate to their new profit-sharing ratio.

Prepare Revaluation Account, Capital Accounts of all partners and the Balance Sheet of the New Firm.

Solution:

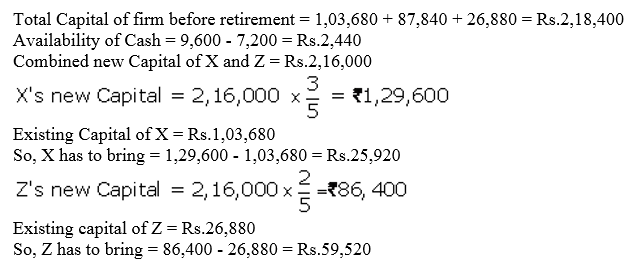

Question 52.

X, Y and Z are partners sharing profits in the ratio of 5 : 3 : 2. Y retires on 1st April, 2018 from the firm, on which date capitals of X, Y and Z after all adjustments are ₹ 1,03,680, ₹ 87,840 and ₹ 26,880 respectively. The Cash and Bank Balance on that date was ₹ 9,600. Y is to be paid through amount brought in by X and Z in such a way as to make their capitals proportionate to their new profit-sharing ratio which will be X 3/5 and Z 2/5. Calculate the amount to be paid or to be brought in by the continuing partners assuming that a minimum Cash and Bank Balance of ₹ 7,200 was to be maintained and pass the necessary journal entries.

Solution:

Question 53.

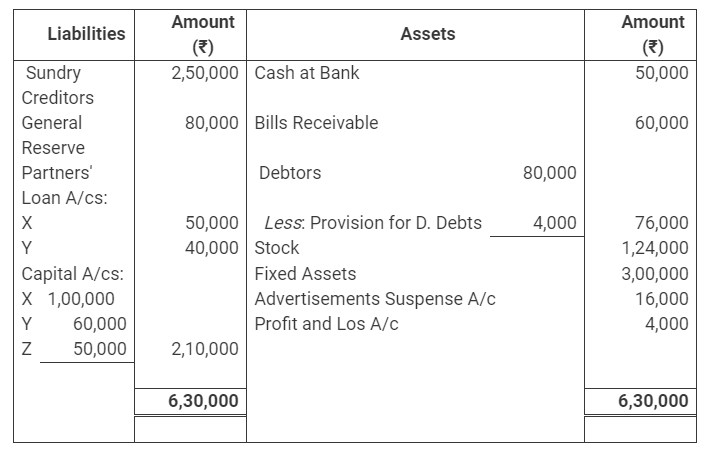

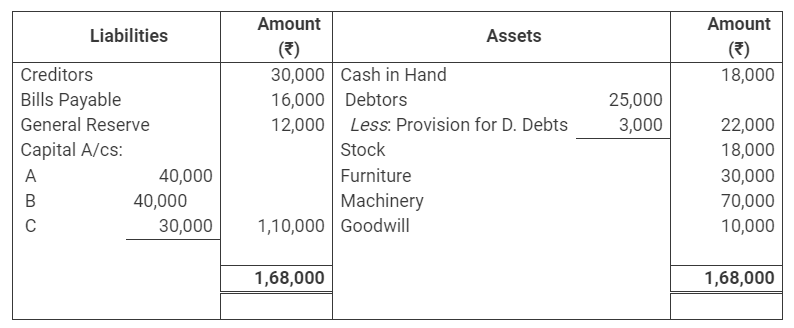

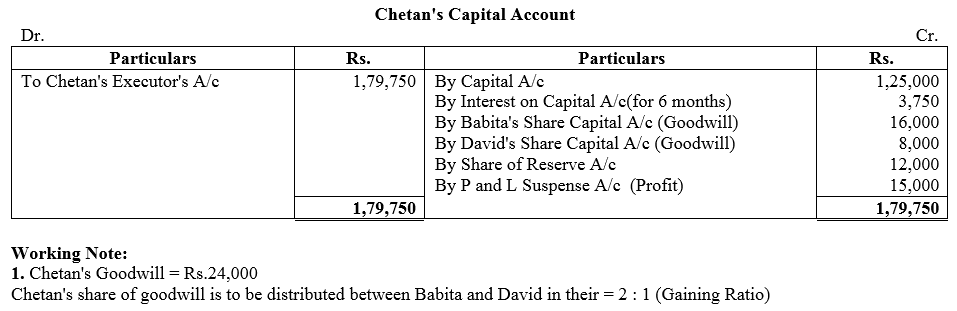

A, B and C are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Their Balance Sheet as at 31st March, 2018 is:

Z is admitted as a new partner on 1st April, 2018 on the following terms:

(a) Provision for doubtful debts is to be maintained at 5% on Debtors.

(b) Outstanding rent amounted to ₹ 15,000.

(c) An accrued income of ₹ 4,500 does not appear in the books of the firm. It is now to be recorded.

(d) X takes over the Investments at an agreed value of ₹ 18,000.

(e) New Profit-sharing Ratio of partners will be 4 : 3 : 2.

(f) Z will bring in ₹ 60,000 as his capital by cheque.

(g) Z is to pay an amount equal to his share in firm’s goodwill valued at twice the average profits of the last three years which were ₹ 90,000 ; ₹ 78,000 and ₹ 75,000 respectively.

(h) Half of the amount of the goodwill is to be withdrawn by X and Y.

You are required to pass journal entries, prepare Revaluation Account, Partners Capital and Current Accounts and the Balance Sheet of the new firm.

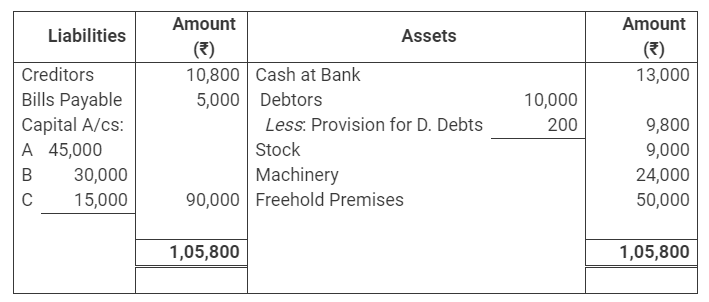

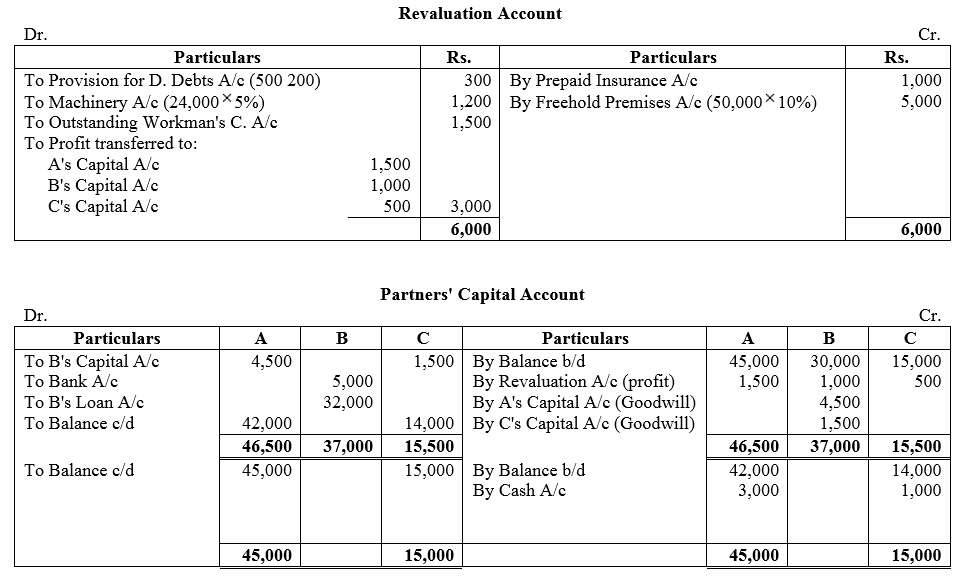

B retires on 1st April, 2018 on the following terms:

(a) Provision for Doubtful Debts be raised by ₹ 1,000.

(b) Stock to be depreciated by 10% and Furniture by 5%.

(c) Their is an outstanding claim of damages of ₹ 1,100 and it is to be provided for.

(d) Creditors will be written back by ₹ 6,000.

(e) Goodwill of the firm is valued at ₹ 22,000.

(f) Bills paid in full with the cash brought in by A and C in such a manner that their capitals are in proportion to their profit-sharing ratio and Cash in Hand remains at ₹ 10,000.

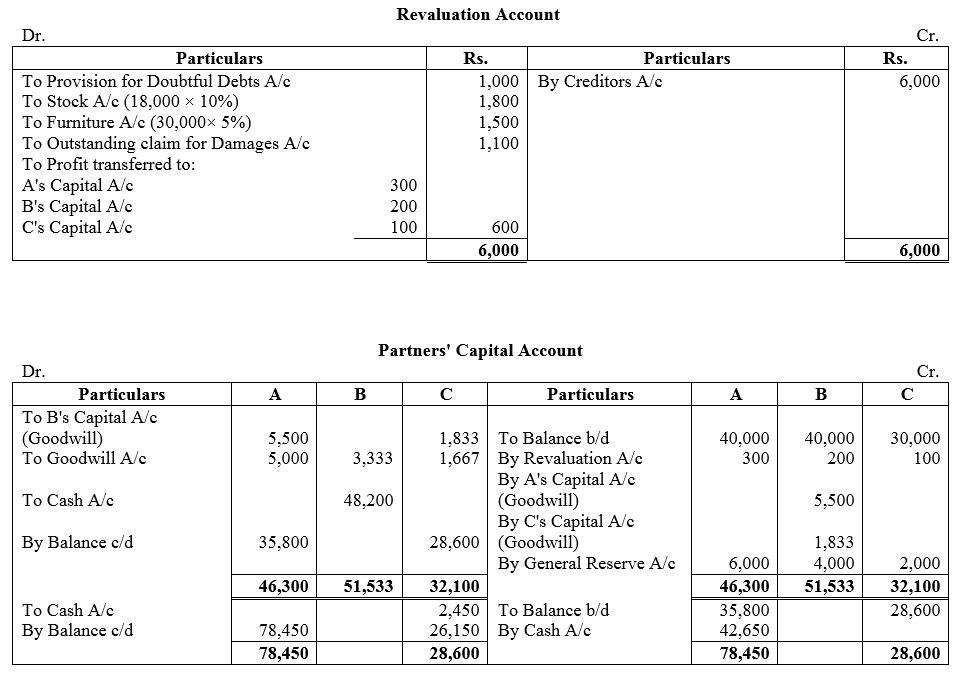

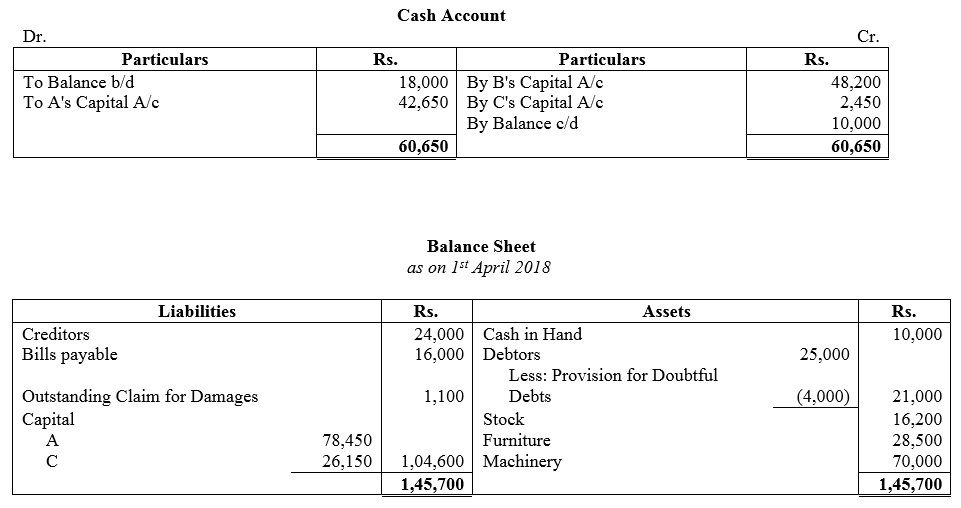

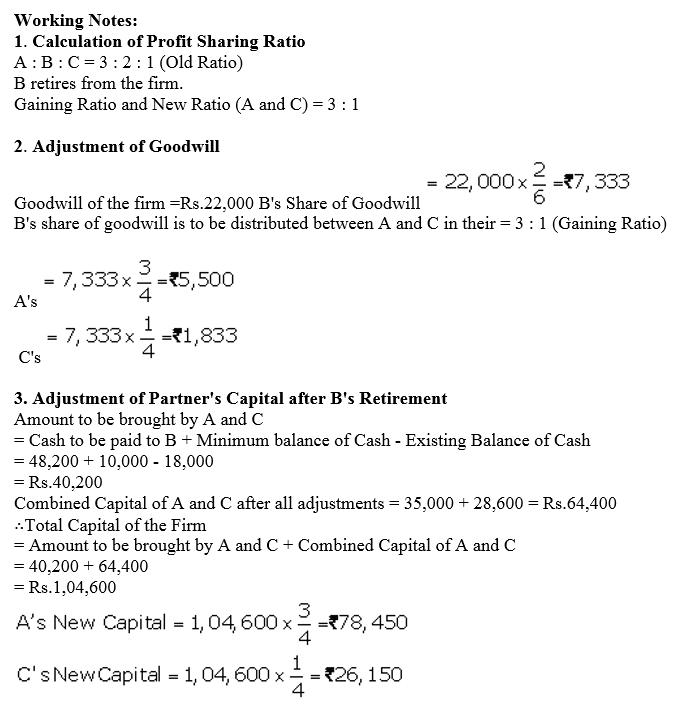

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of A and C.

Solution:

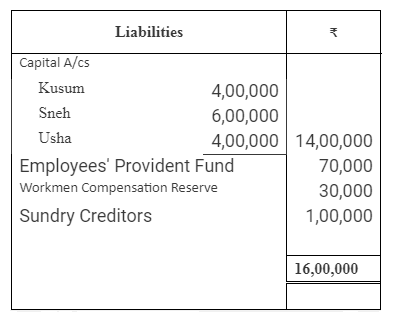

Question 54.

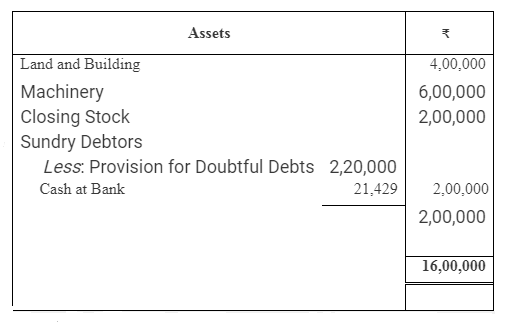

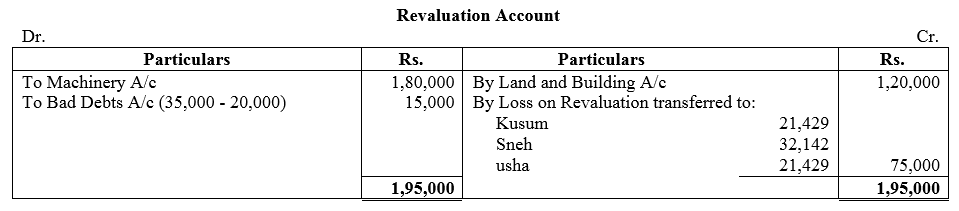

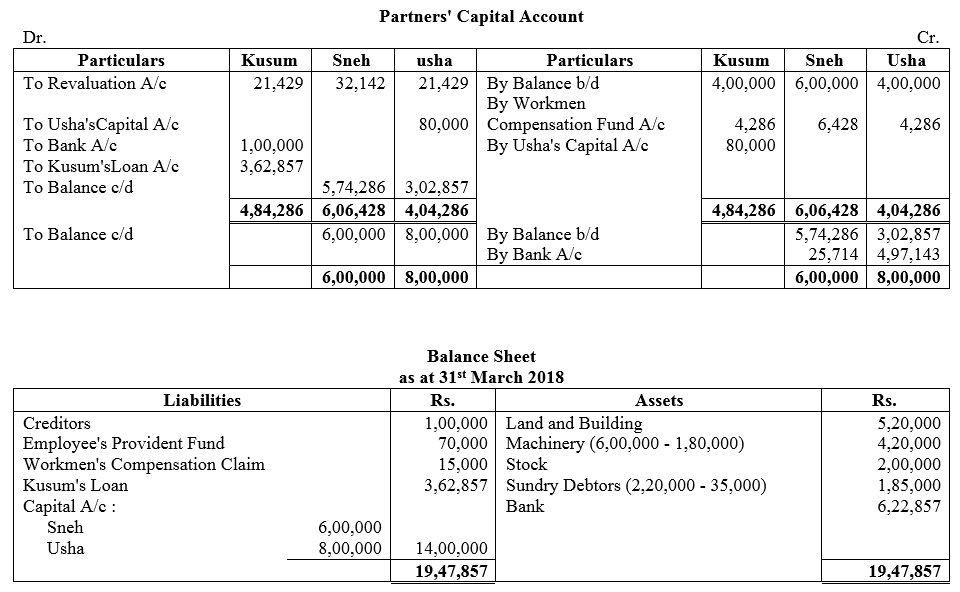

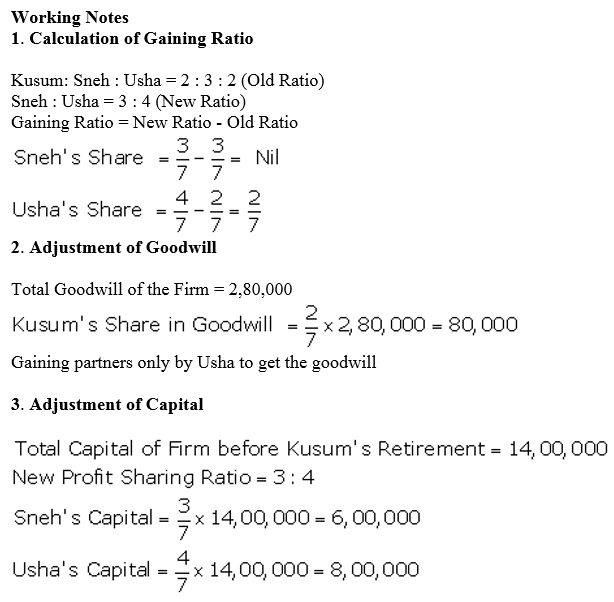

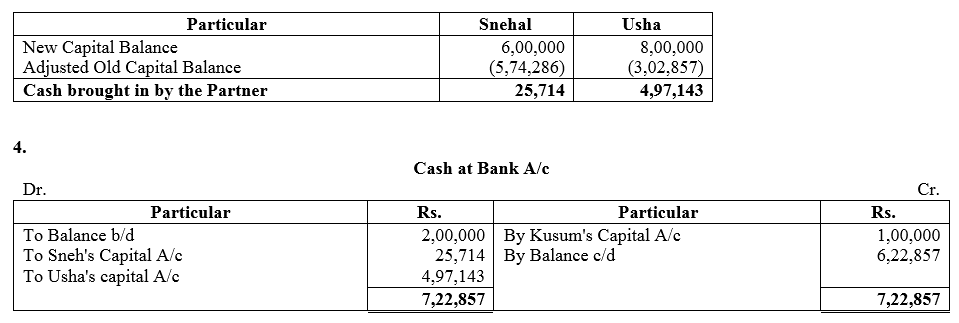

Following is the Balance Sheet of Kusum, Sneh and Usha as on 31st March, 2018, who have agreed to share profits and losses in proportion of their capitals:

On 31st March, 2018, Kusum retired from the firm and the remaining partners decided to carry on the business. It was agreed to revalue the assets and reassess the liabilities on that date, on the following basis:

(a) Land and Building be appreciated by 30%.

(b) Machinery be depreciated by 30%.

(c) There were Bad Debts of ₹ 35,000.

(d) The claim against Workmen Compensation Reserve was estimated at ₹ 15,000.

(e) Goodwill of the firm was valued at ₹ 2,80,000 and Kusum’s share of goodwill was adjusted against the Capital Accounts of the continuing partners Sneh and Usha who have decided to share future profits in the ratio of 3 : 4 respectively.

(f) Capital of the new firm in total will be the same as before the retirement of Kusum and will be in the new profit-sharing ratio of the continuing partners.

(g) Amount due to Kusum be settled by paying ₹ 1,00,000 in cash and balance by transferring to her Loan Account which will be paid later on.

Prepare Revaluation Account, Capital Accounts of Partners and Balance Sheet of the new firm after Kusum’s retirement.

Solution:

Question 55.

The Balance Sheet of X, Y and Z who were sharing profits in the ratio of 5 : 3 : 2 as at 31st March, 2018 is as follows:

X retired on 31st March, 2018 and Y and Z decided to share profits in future in the ratio of 3 : 2 respectively.

The other terms on retirement were:

(a) Goodwill of the firm is to be valued at ₹ 80,000.

(b) Fixed Assets are to be depreciated to ₹ 57,500.

(c) Make a Provision for Doubtful Debts at 5% on Debtors.

(d) A liability for claim, included in Creditors for ₹ 10,000 is settled at ₹ 8,000.

The amount to be paid to X by Y and Z in such a way that their Capitals are proportionate to their profit-sharing ratio and leave a balance of ₹ 15,000 in the Bank Account.

Prepare Profit and Loss Adjustment Account and Partners Capital Accounts.

Solution:

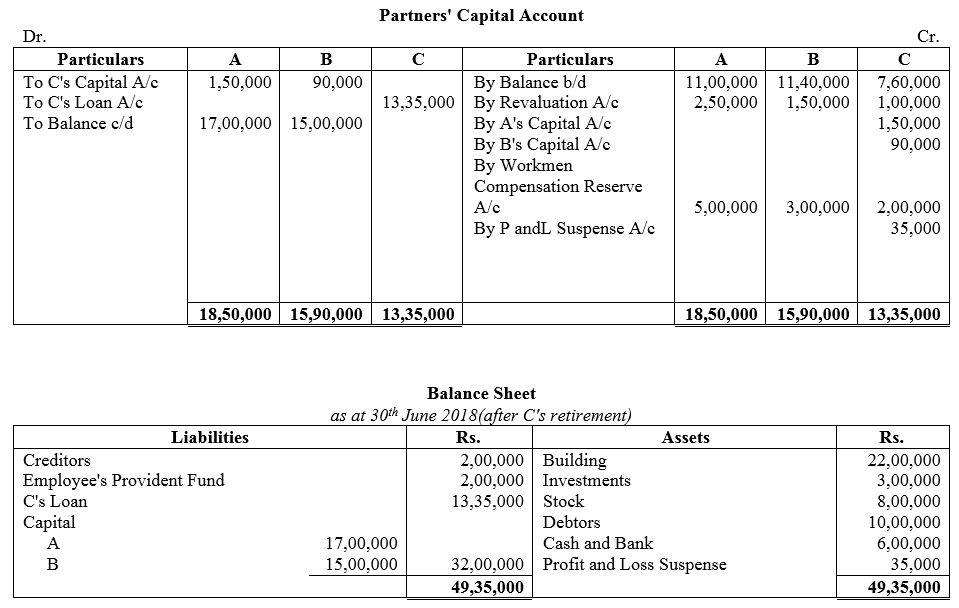

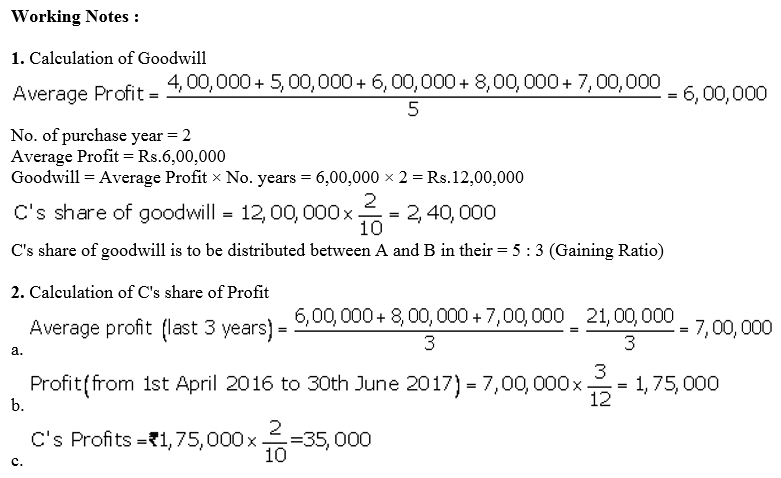

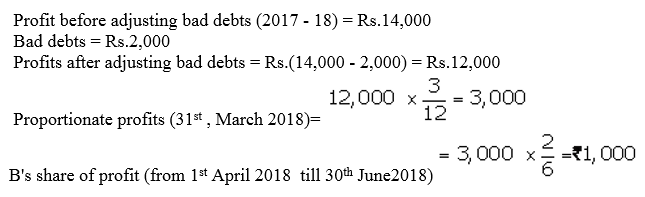

Question 56.

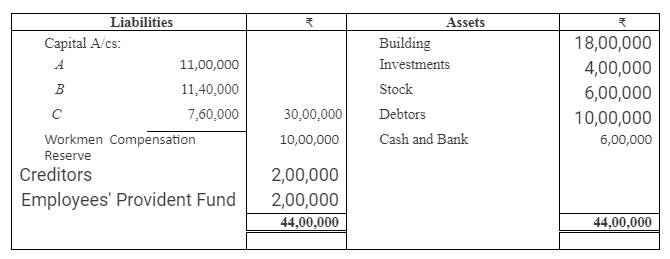

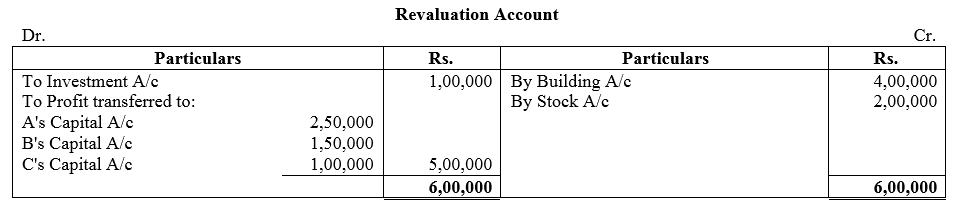

A, B and C are partners sharing profits in the ratio of 5 : 3 : 2. Their Balance Sheet as on 31st March, 2018 is given below:

C retires on 30th June, 2018 and it was mutually agreed that:

(a) Building be valued at ₹ 22,00,000.

(b) Investments to be valued at ₹ 3,00,000.

(c) Stock be taken at ₹ 8,00,000.

(d) Goodwill of the firm be valued at two years purchase of the average profit of the past five years.

(e) C’s share of profits up to the date of retirement be calculated on the basis of average profit of the preceding three years.

The profits of the preceding five years were as under:

(f) Amount payable to C to be transferred to his Loan Account carrying interest @ 10% p.a.

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet as at 30th June, 2018.

Solution:

Question 57.

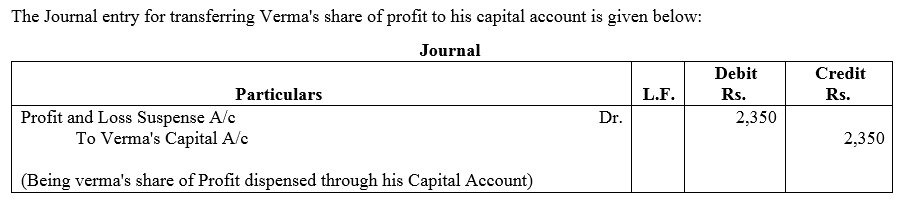

Kumar,Verma and Naresh were partners in a firm sharing profits and Loss in the ratio of 3 : 2 : 2. On 23rd January, 2015 Verma died. Verma’s share of profit till the date of his death was calculated at ₹ 2,350. Pass necessary journal entry for the same in the books of the firm.

Solution:

Question 58.

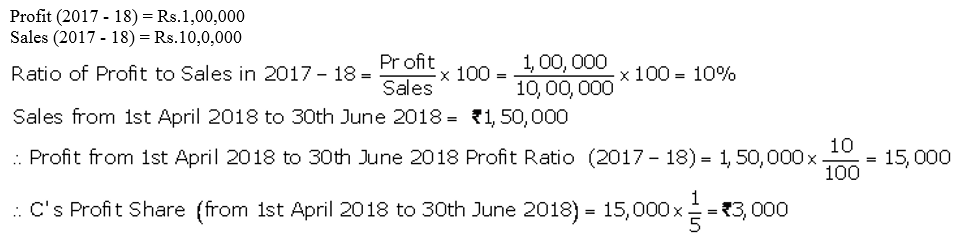

A, B and C were partners sharing profits and losses in the ratio of 2 : 2 : 1. C died on 30th June, 2018. Profit and Sales for the year ended 31st March, 2018 were ₹ 1,00,000 and ₹ 10,00,000 respectively. Sales during April to June, 2018 were ₹ 1,50,000. You are required to calculate share of profit of C up to the date of his death.

Solution:

Question 59.

A, B and C are partners sharing profits and losses in the ratio of 3 : 2 : 1. B died on 30th June, 2018. For the year ended 31st March, 2019, proportionate profit of 2018 is to be taken into consideration. During the year ended 31st March, 2018, bad debts of ₹ 2,000 had to be adjusted. The profit for the year ended 31st March, 2018 was ₹ 14,000 before adjustment of bad debts. Calculate B’s share of profit till the date of his death.

Solution:

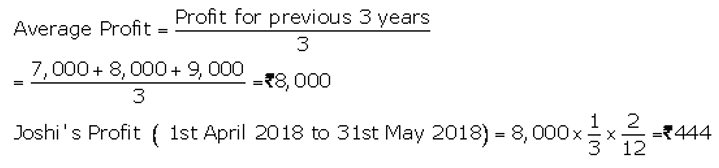

Question 60.

Ram, Manohar and Joshi were partners in a firm. Joshi died on 31st May, 2018. His share of profit from the closure of the last accounting year till the date of death was to be calculated on the basis of the average of three completed years of profits before death. Profits for the years ended 31st March, 2016, 2017 and 2018 were ₹ 7,000; ₹ 8,000 and ₹ 9,000 respectively. Calculate Joshi’s share of profit till the date of his death and pass necessary journal entry for the same.

Solution:

Question 61.

X, Y and Z were partners sharing profits and losses in the ratio of 3 : 2 : 1 respectively. Y died on 30th June, 2018. The Profit from 1st April, 2018 to 30th June, 2018 amounted to ₹ 3,60,000. X and Z decided to share the future profits in the ratio of 3 : 2 respectively with effect from 1st July, 2018. Pass the necessary journal entries to record Y’s share of profit up to the date of death.

Solution:

Question 62.

X, Y and Z were partners in a firm. Z died on 31st May, 2018. His share of profit from the closure of the last accounting year till the date of death was to be calculated on the basis of the average of three completed ₹ 19,000 and ₹ 17,000 respectively.

Calculate Z’s share of profit till his death and pass necessary journal entry for the same assuming:

(a) there is no change in profit-sharing ratio of remaining partners, and

(b) there is change in profit-sharing ratio of remaining partners, new ratio being 3 : 2.

Solution:

Question 63.

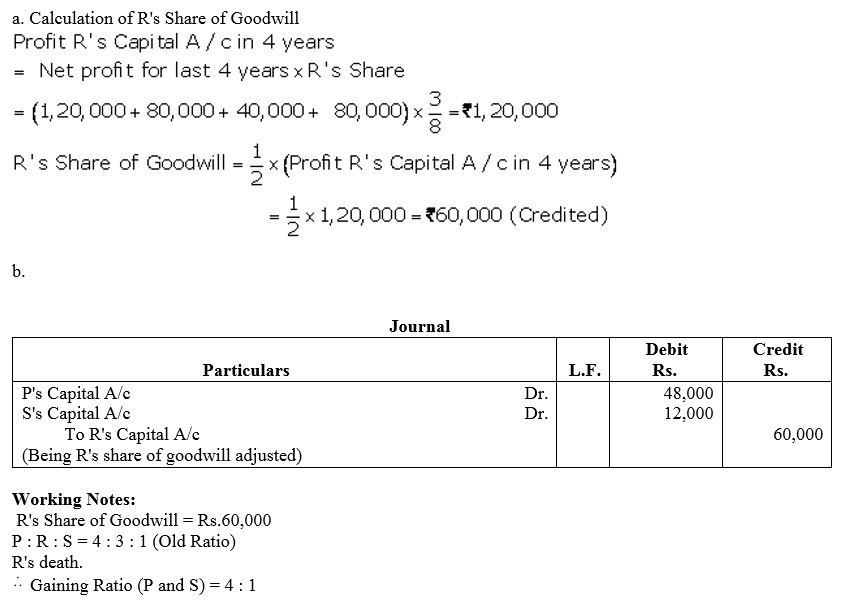

P, R and S are in partnership sharing profits 4/8, 3/8 and 1/8 respectively. It is provided in the Partnership Deed that on the death of any partner his share of goodwill is to be valued at one-half of the net profit credited to his account during the last four completed years.

R died on 1st January, 2018. The firm’s profits for the last four years ended 31st December, were as:

2014 – ₹ 1,20,000; 2015 – ₹ 80,000; 2016 – ₹ 40,000; 2017 – ₹ 80,000.

(a) Determine the amount that should be credited to R in respect of his share of Goodwill.

(b) Pass journal entry without raising Goodwill Account for its adjustment.

Solution:

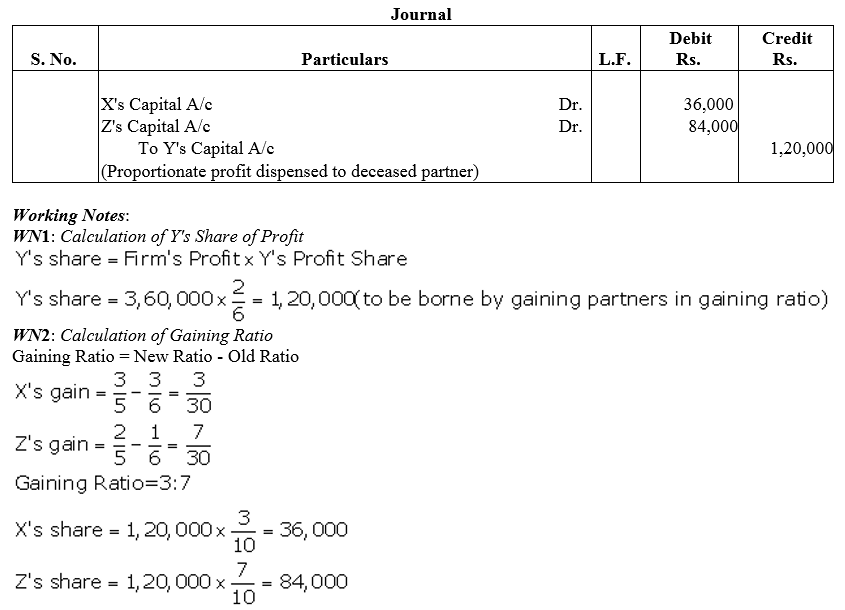

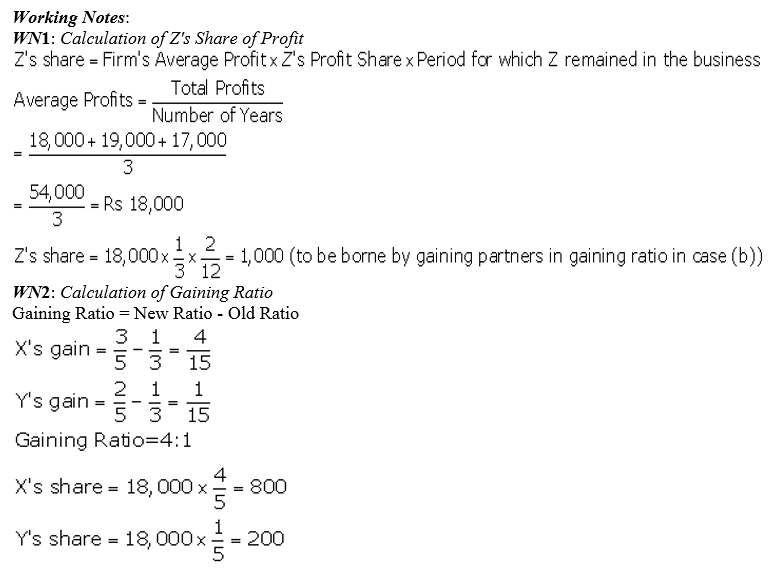

Question 64.

X, Y and Z were partners in a firm sharing profit in 3 : 2 : 1 ratio. The firm closes its books on 31st March every year. Y died on 30th June, 2018. On Y’s death the goodwill of the firm was valued at ₹60,000. Y’s share in the profits of the firm till the time of his death was to be calculated on the basis of previous year’s profit which was ₹ 1,50,000.

Pass necessary journal entries for the treatment of goodwill and Y’s share of profit at the time of his death.

Solution:

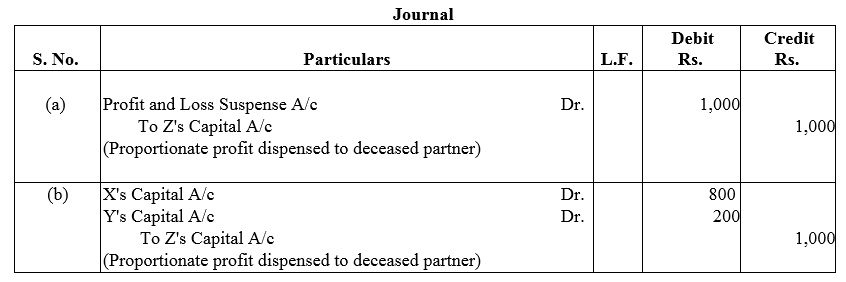

Question 65.

X, Y and Z were partners in a firm sharing profits in the ratio of 4 : 3 : 1. The firm closes its books on 31st March every year. On 1st February 2018, Y died and it was decided that the new profit-sharing ratio between X and Z will be equal. Partnership Deed provided for the following on the death of a partner:

(a) His share of goodwill be calculated on the basis of half of the profits credited to his account during the previous four completed years. The firm’s profits for the last four years were:

(b) His share of profit in the year of his death was to be computed on the basis of average profit of past two years.

Pass necessary journal entries realting to goodwill and profit to be transferred to Y’s Capital Account.

Solution:

Question 66.

X and Y are partners. The Partnership Deed provides inter alia:

(a) That the Accounts be balanced on 31st March every year.

(b) That the profits be divided as : X one-half, Y one-third and carried to a Reserve one-sixth.

(c) That in the event of the death of a partner, his Executors be entitled to be paid out:

(i) The Capital to his credit till the date of death.

(ii) His proportion of profits till the date of death based on the average profits of the last three completed years.

(iii) By way of Goodwill, his proportion of the total profits for the three preceding years.

(d)

The Profits for three years were : 2015-16 : ₹ 4,200; 2016-17 : ₹ 3,900; 2017-18 : ₹ 4,500. Y died on 1st August, 2018. Prepare necessary accounts.

Solution:

Question 67.

P, Q and R were partners in a firm sharing profits in 2 : 2 : 1 ratio. The Partnership Deed provided that on the death of a partner his executors will be entitled to the following:

(a) Interest on Capital @ 12% p.a.

(b) Interest on Drawings @ 18% p.a.

(c) Salary of ₹ 12,000 p.a.

(d) Share in the profit of the firm(up to the date of death) on the basis of previous year’s profit.

P died on 31st May, 2108. His capital was ₹ 80,000. He had withdrawn ₹ 15,000 and interest on his drawings was calculated as ₹ 1,200. Profit of the firm for the previous year ended 31st March, 2018 was ₹ 30,000.

Prepare P’s Capital Account to be rendered to his executors.

Solution:

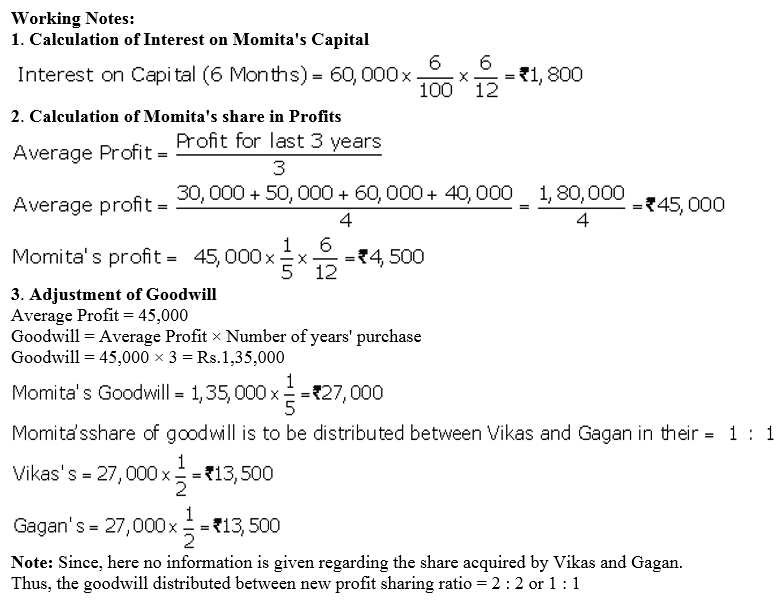

Question 68.

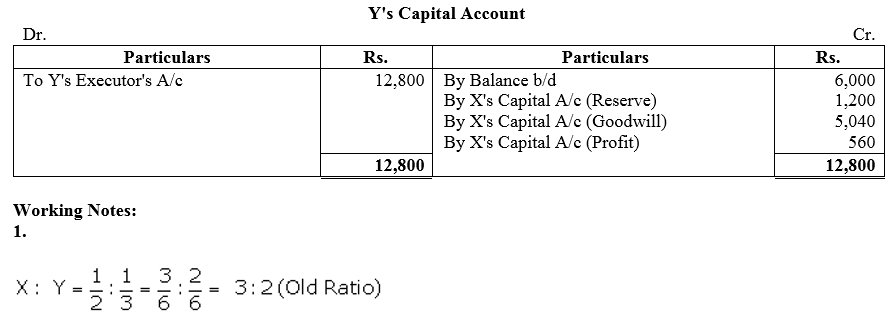

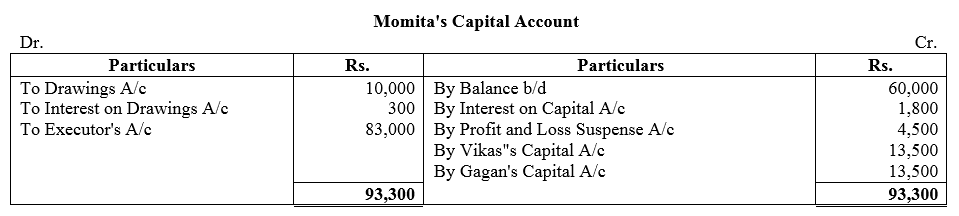

Vikas, Gagan and Momita were partners in a firm sharing profits in the ratio of 2 : 2 : 1. The firm closes its books on 31st March every year. On 30th September, 2014 Momita died. According to the provisions of Partnership Deed the legal representatives of a deceased partner are entitled for the following in the event of his/her death:

(a) Capital as per the last Balance Sheet.

(b) Interest on capital at 6% per annum till the date of her death.

(c) Her share of profit to the date of death calculated on the basis of average profit of last four years.

(d) Her share of goodwill to be determined on the basis of three years purchase of the average profit of last four years. The profits of last four years were:

The balance in Momita’s Capital Account on 13st March, 2014 was ₹ 60,000 and she had withdrawn ₹ 10,000 till date of her death. Interest on her drawings was ₹ 300.

Prepare Momita’s Capital Account to be presented to her executors.

Solution:

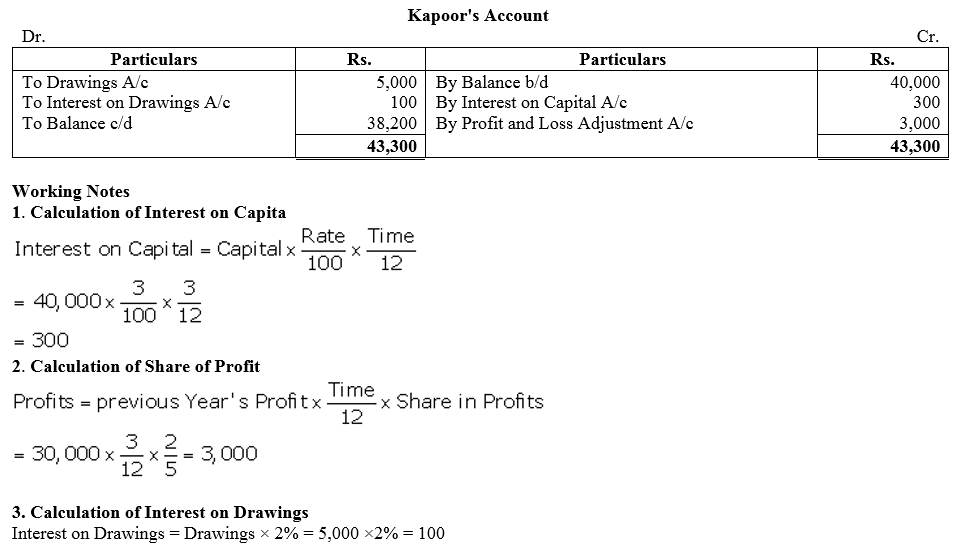

Question 69.

Iqbal and Kapoor are in partnership sharing profits and losses in 3 : 2. Kapoor died three months after the date of the last Balance Sheet. According to the Partnership Deed, the legal personal representatives of Kapoor are entitled to the following payments:

(a) His capital as per the last Balance Sheet.

(b) Interest on above capital @ 3% p.a. till the date of death.

(c) His share of profits till the date of death calculated on the basis of last year’s profits.

His drawings are to bear interest at an average rate of 2% on the amount irrespective of the period. The net profits for the last three years, after charging insurance premium, were ₹ 20,000; ₹ 25,000 and ₹ 30,000 respectively. Kapoor’s capital as per Balance Sheet was ₹ 40,000 and his drawings till the date of death were ₹ 5,000.

Draw Kapoor’s Capital Account to be rendered to his representatives.

Solution:

Question 70.

A, B and C were partners in a firm sharing profits in the ratio of 5 : 3 : 2. On 31st March, 2017, their Balance Sheet was as follows:

A died on 1st October, 2017. It was agreed among his executors and the remaining partners that:

(i) Goodwill to be valued at 2\(\frac { 1 }{ 2 }\) years purchase of the average profit of the previous 4 years, which were 2013-14: ₹ 13,000; 2014-15: ₹ 12,000; 2015-16: ₹ 20,000 and 2016-17: ₹ 15,000.

(ii) Patents be valued at ₹ 8,000; Machinery at ₹ 28,000; and Building at ₹ 25,000.

(iii) Profits for the year 2017-18 be taken as having accrued at the same rate as that of the previous year.

(iv) Interest on capital be provided @ 10% p.a.

(v) Half of the amount due to A to be paid immediately to the executors and the balance transferred to his (Executors) Loan Account.

Prepare A’s Capital Account and A’s Executors Account as on 1st October, 2017.

Solution:

Question 71.

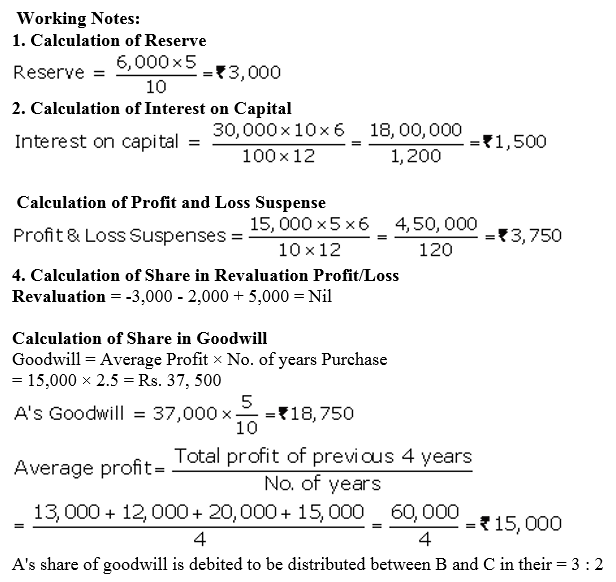

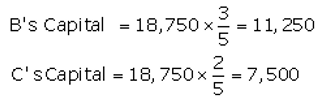

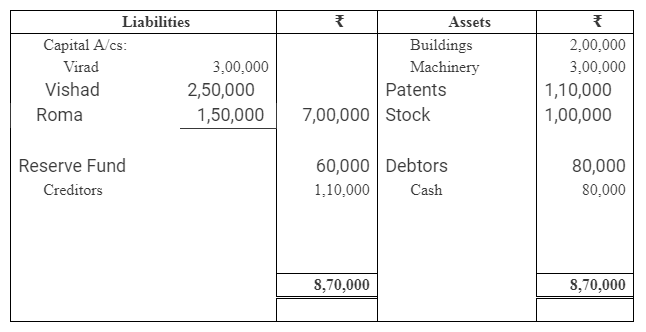

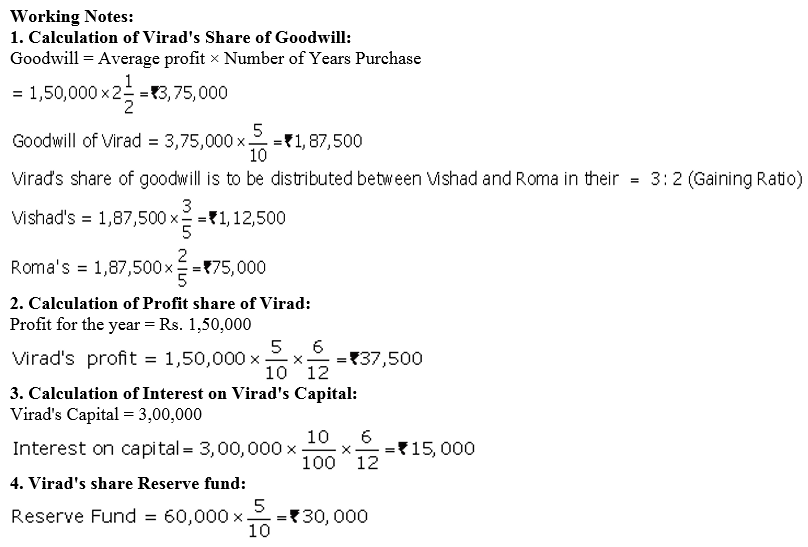

Virad, Vishad and Roma were partners in a firm sharing profits in the ratio of 5 : 3 : 2 respectively. On 31st March, 2103, their Balance Sheet was as under:

Virad died on 1st October, 2013. It was agreed between his executors and the remaining partners that:

(i) Goodwill of the firm be valued at 2\(\frac { 1 }{ 2 }\) years purchase of average profits for the last three years. The average profits were ₹ 1,50,000.

(ii) Interest on capital be provided at 10% p.a.

(iii) Profits for the 2013-14 be taken as having accrued at the same rate as that of the previous year which was ₹ 1,50,000.

Prepare Virad’s Capital Account to be presented to his Executors as on 1st October, 2013.

Solution:

Question 72.

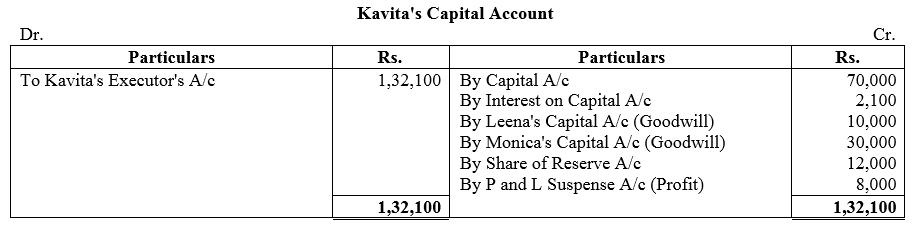

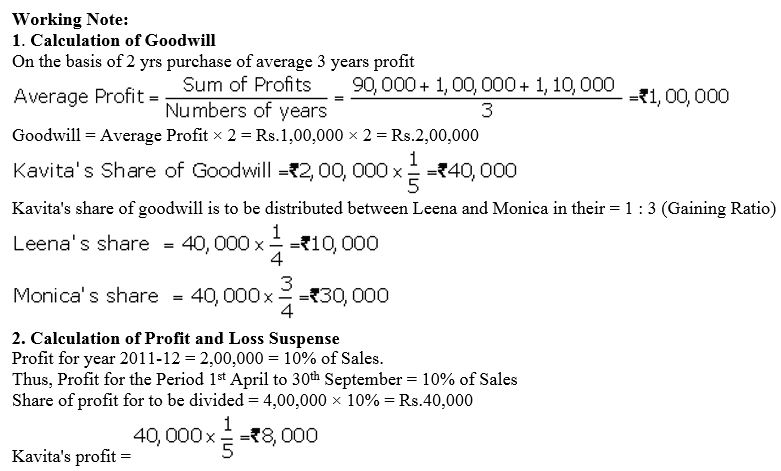

Kavita, Leena and Monica are partners in firm sharing profits in the ratio of 1 : 1 : 3 respectively. Their Capital Accounts showed the following balanceson 31st March, 2012: Kavita ₹ 70,000; Leena ₹ 65,000 and Monica ₹ 2,10,000. Firm closes its accounts every year on 31st March. Kavita died on 30th September, 2012. In the event of death of any partner, the Partnership Deed provides for the following:

(a) Interest on capital will be calculated at the rate of 6% p.a.

(b) The deceased partner’s share in the goodwill of the firm will be calculated on the basis of 2 years purchase of the average profit of last three years. The profits of the firms for the last three years were ₹ 90,000; ₹ 1,00,000 and ₹ 1,10,000 respectively.

(c) Her share in the Reserve Fund of the firm will be paid. The Reserve Fund of the firm was ₹ 60,000 at the time of Kavita’s death.

(d) Her share of profit till the date of death will be calculated on the basis of sales. It is also specified that the sales during the year 2011-12 were ₹ 20,00,000. The sales from 1st April, 2012 to 30th September, 2012 were ₹ 4,00,000. The profit of the firm for the year ending 31st March, 2012 was ₹ 2,00,000.

Prepare Kavita’s Capital Account to be presented to his legal representative.

Solution:

Question 73.

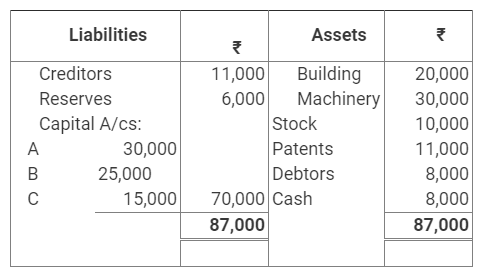

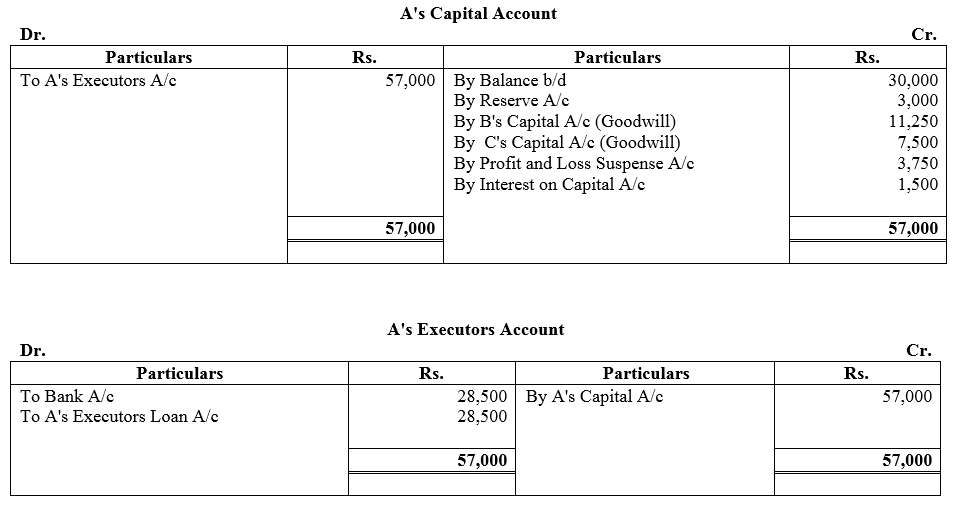

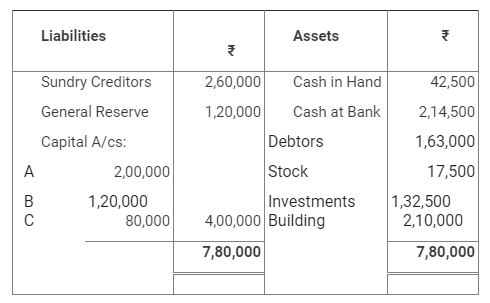

A, B and C are partners in a firm sharing profits in the proportion of 3 : 2 : 1. Their Balance Sheet as at 31st March, 2018 stood as follows:

B died on 30th June, 2018 and according to the deed of the said partnership his executors are entitled to be paid as under:

(a) The capital to his credit at the time of his death and interest thereon @ 10% per annum.

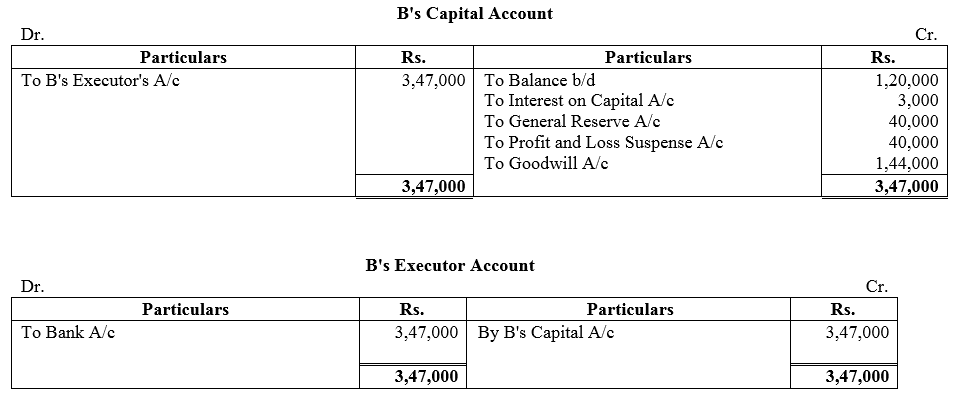

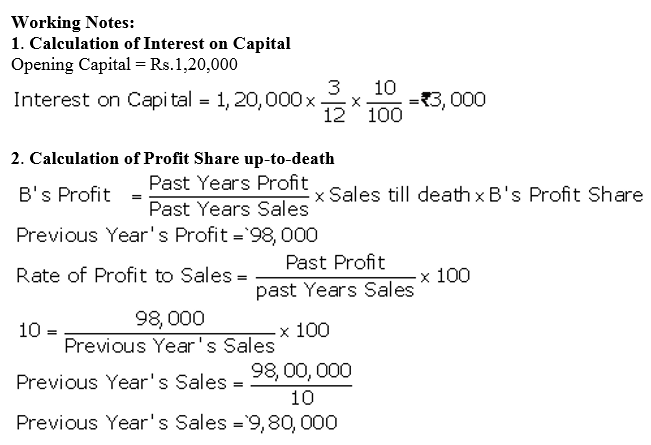

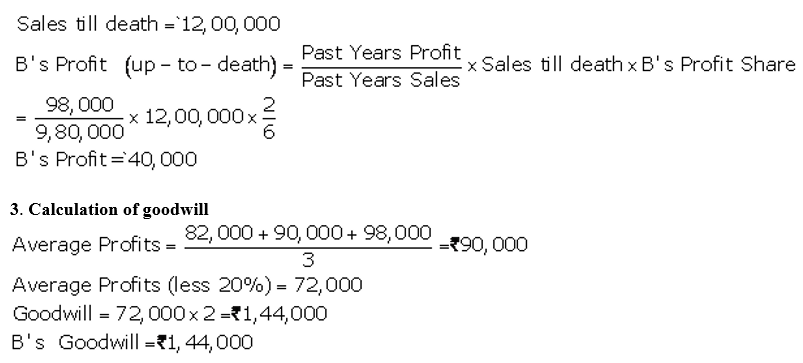

(b) His proportionate share of General Reserve.

(c) His share of profits from the intervening period will be based on the sales during that period. Sales from 1st April, 2018 to 30th June, 2018 were as ₹ 12,00,000. The rate of profit during past three years had been 10% on sales.

(d) Goodwill according to his share of profit to be calculated by taking twice the amount of profits of the last three years less 20%. The profit of the previous three years were: 1st Year: ₹ 82,000; 2nd year: ₹ 90,000; 3rd year: ₹ 98,000.

(e) The investments were sold at par and his executors were paid out in full.

Prepare B’s Capital Account and his Executors Account.

Solution:

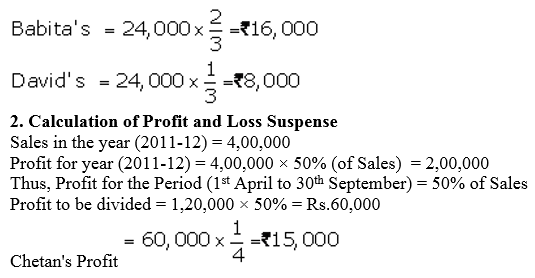

Question 74.

Babita, Chetan and David are partners in a firm sharing profits in the ratio of 2 : 1 : 1 respectively. Firm closes its accounts on 31st March every year. Chetan died on 30th September, 2012. There was a balance of ₹ 1,25,000 in Chetan’s Capital Account in the beginning of the year. In the event of Death of any partner, the Partnership Deed provides for the following:

(a) Interest on capital will be calculated at the rate of 6% p.a.

(b) The executor of deceased partner shall be paid ₹ 24,000 for his share of goodwill.

(c) His share of Reserve Fund of ₹ 12,000, shall be paid to his executor.

(d) His share of profit till the date of death will be calculated on the basis of sales. It is also specified that the sales during the year 2011-12 were ₹ 4,00,000. The sales from 1st April, 2012 to 30th September, 2012 were ₹ 1,20,000. The profit of the firm for the year ending 31st March, 2012 was ₹ 2,00,000.

Prepare Chetan’s Capital Account to be presented to his executor.

Solution:

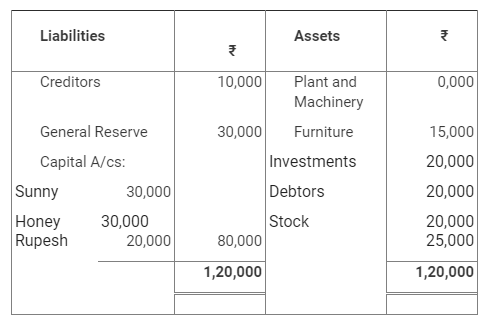

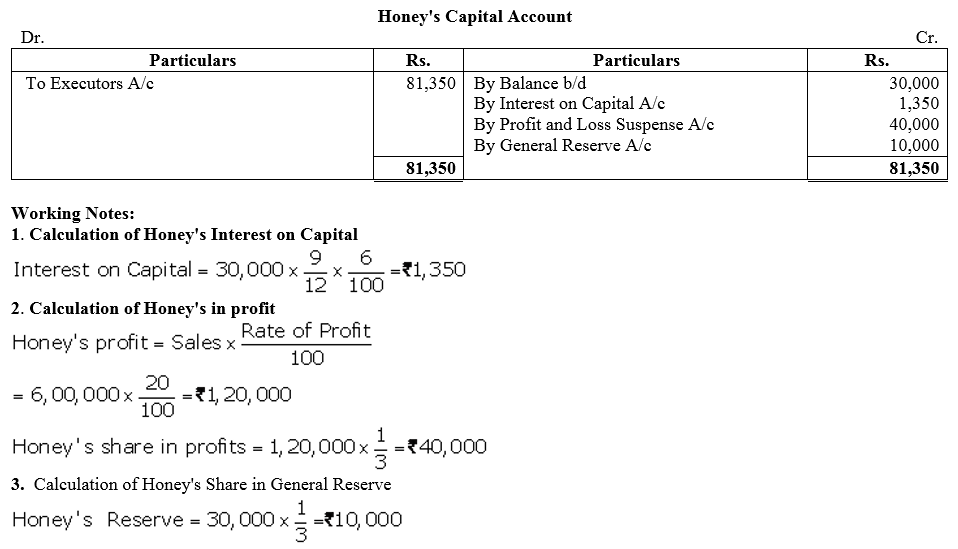

Question 75.

Sunny, Honey and Rupesh were partners in a firm. On 31st March, 2014, their Balance Sheet was as follows:

Honey died on 31st December, 2014. The Partnership Deed provided that the representative of the deceased partner shall be entitled to:

(a) Balance in the Capital Account of the deceased partner.

(b) Interest on Capital @ 6% per annum up to the date of his death.

(c) His share in the undistributed profits or losses as per the Balance Sheet.

(d) His share in the profits of the firm till the date of his death, calculated on the basis of rate of net profit on sales of the previous year. The rate of net profit on sales of previous year was 20%. Sales of the firm during the year till 31st December, 2014 was ₹ 6,00,000.

Prepare Honey’s Capital Account to be presented to his executors.

Solution:

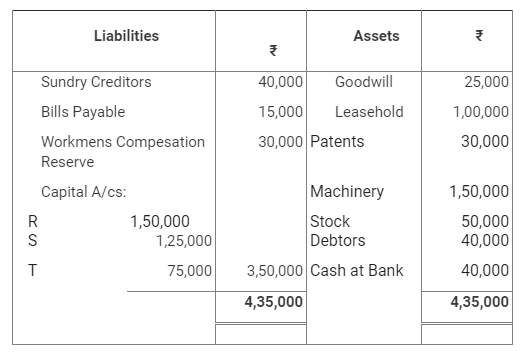

Question 76.

R, S and T were partners sharing profits and losses in the ratio of 5 : 3 : 2 respectively. On 31st March, 2018, Their Balance Sheet stood as:

T died on 1st August, 2018. It was agreed that:

(a) Goodwill be valued at 2\(\frac { 1 }{ 2 }\) years purchase of average of last 4 years profits which were:

2014-15: ₹ 60,000; 2016-17: ₹ 80,000 and 2017-18: ₹ 75,000.

(b) Machinery be valued at ₹ 1,40,000; Patents be valued at ₹ 40,000; Leasehold be valued at ₹ 1,25,000 on 1st August, 2018.

(c) For the purpose of calculating T’s share in the profits of 2018-19, the profits in 2018-19 should be taken to have accrued on the same scale as in 2017-18.

(d) A sum of ₹ 21,000 to be paid immediately to the Executors of T and the balance to be paid in four equal half-yearly installments together with interest @ 10% p.a.

Pass necessary journal entries to record the above transactions and T’s Executors Account.

Solution:

Question 77.

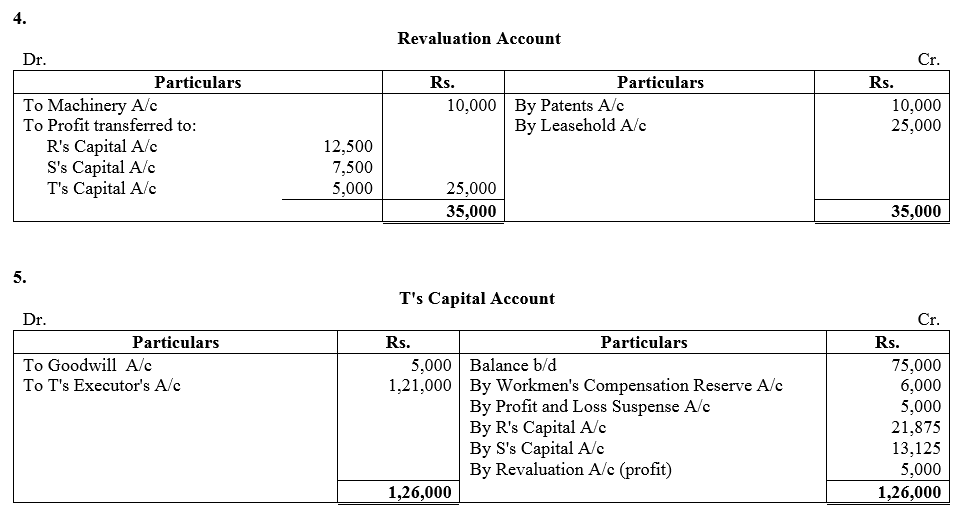

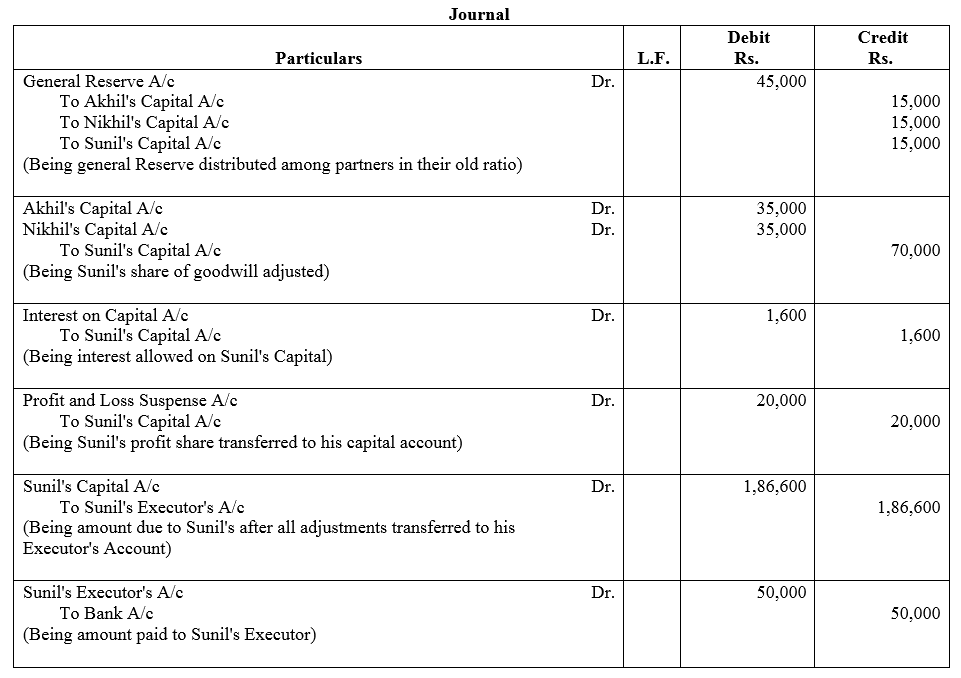

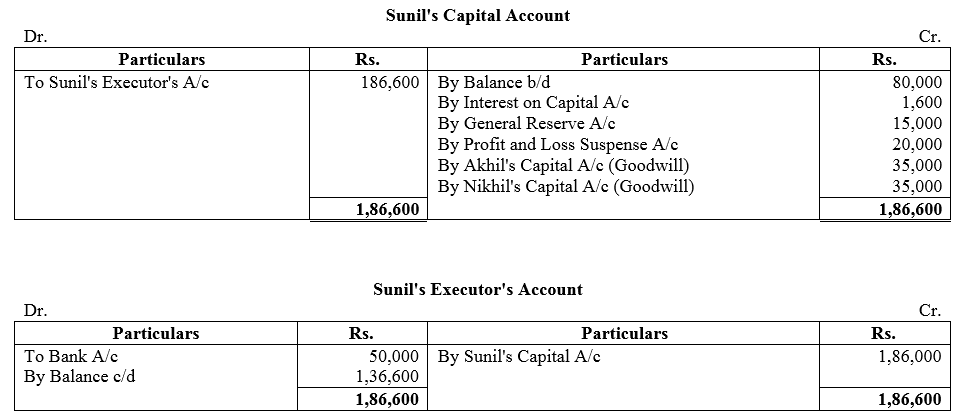

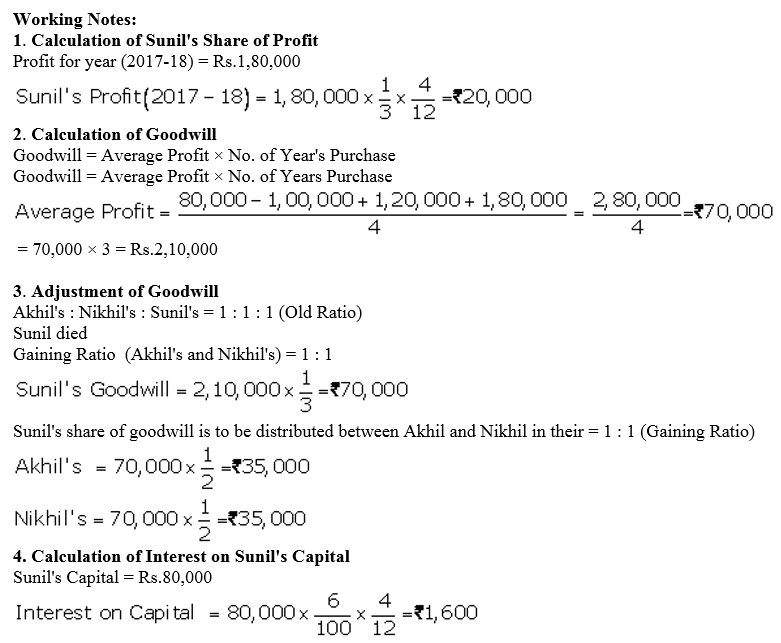

Akhil, Nikhil and Sunil were partners sharing profits and losses equally. Following was their Balance Sheet as at 31st March, 2018:

Sunil died on 1st August, 2018. The Partnership Deed provided that the executor of a deceased partner was entitled to:

(a) Balance of Partners Capital Account and his share of accumulated reserve.

(b) Share of profits from the closure of the last accounting year till the date of death on the basis of the profit of the preceding completed year before death.

(c) Share of goodwill calculated on the basis of three times the average profit of the last four years.

(d) Interest on deceased partner’s capital @ 6% p.a.

(e) ₹ 50,000 to be paid to deceased executor immediately and the balance to remain in his Loan Account.

Profits and Losses for the preceding years were: 2014-15: ₹ 80,000 Profit ; 2015-16: ₹ 1,00,000 Loss; 2016-17: ₹ 1,20,000 Profit; 2017-18: ₹ 1,80,000 Profit.

Pass necessary journal entries and prepare Sunil’s Capital Account and Sunil’s Executor Account.

Solution:

Question 78.

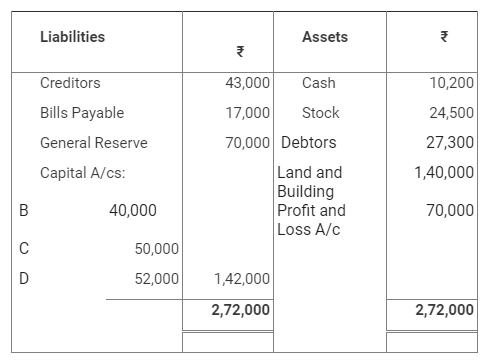

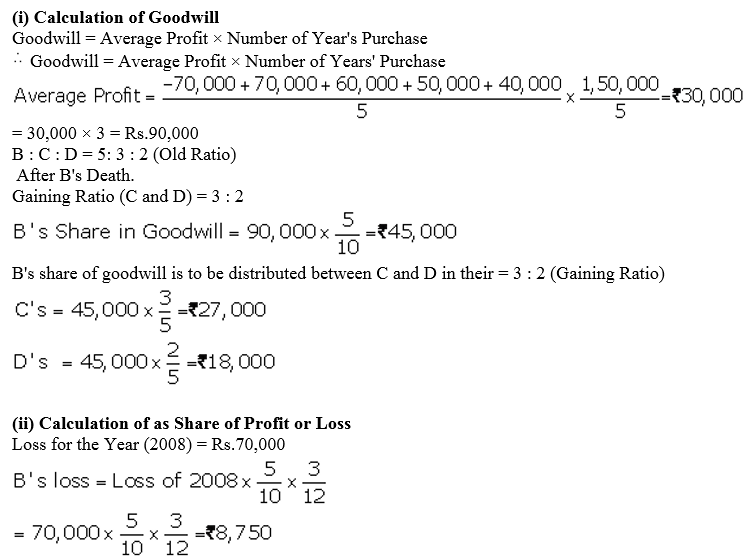

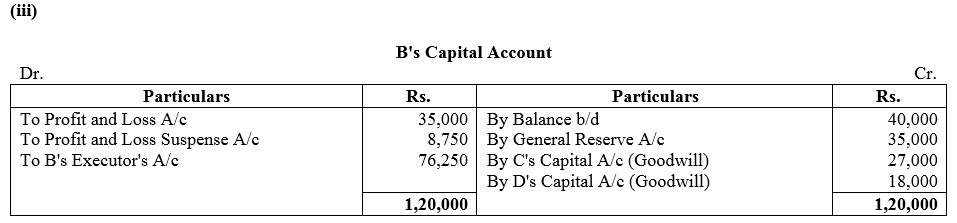

B, C and D were partners in a firm sharing profits in the ratio of 5 : 3 : 2. On 31st December, 2008, their Balance Sheet was as follows:

B died on 31st March, 2009. The Partnership Deed provided for the following on the death of a partner:

(a) Goodwill of the firm was to be valued at 3 years purchase of the average profit of last 5 years. The profits for the years ended 31st December, 2007, 31st December 2006, 31st December 2005 and 31st December 2004 were ₹ 70,000 ; ₹ 60,000 and ₹ 40,000 respectively.

(b) B’s share of profit and loss till the date of his death was to be calculated on the basis of the profit and loss for the year ended 31st December, 2008.

You are required to calculate the following :

(i) Goodwill of the firm and B’s share of goodwill at the time of his death.

(ii) B’s share in the profit or loss of the firm till the date of his death.

(iii) Prepare B’s Capital Account at the time of his death to be presented to his Executors.

Solution:

Question 79.

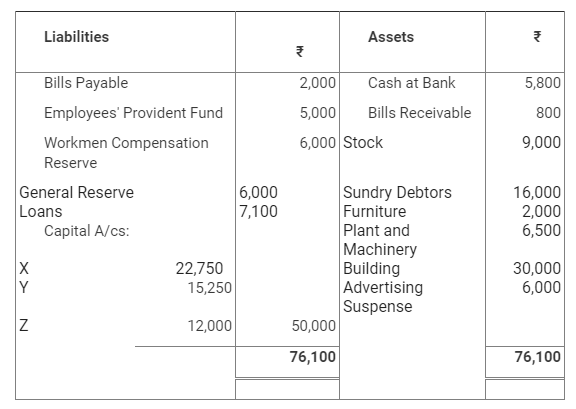

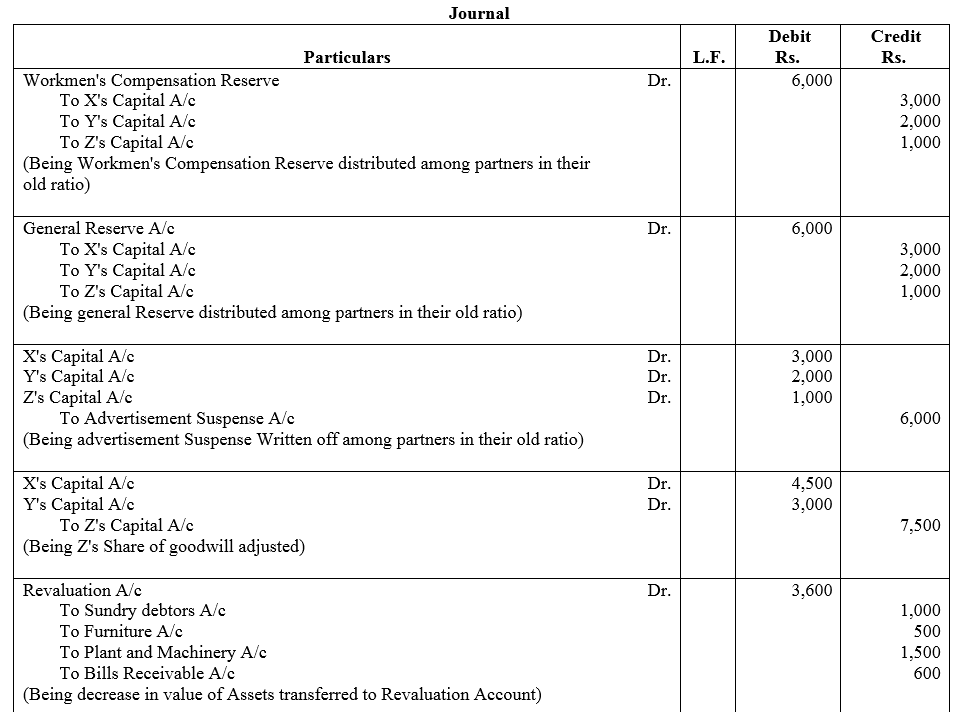

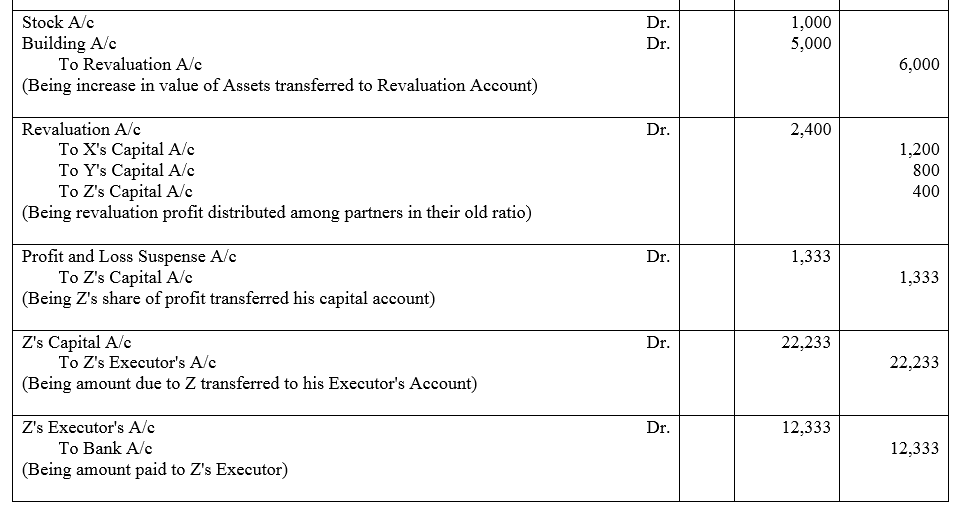

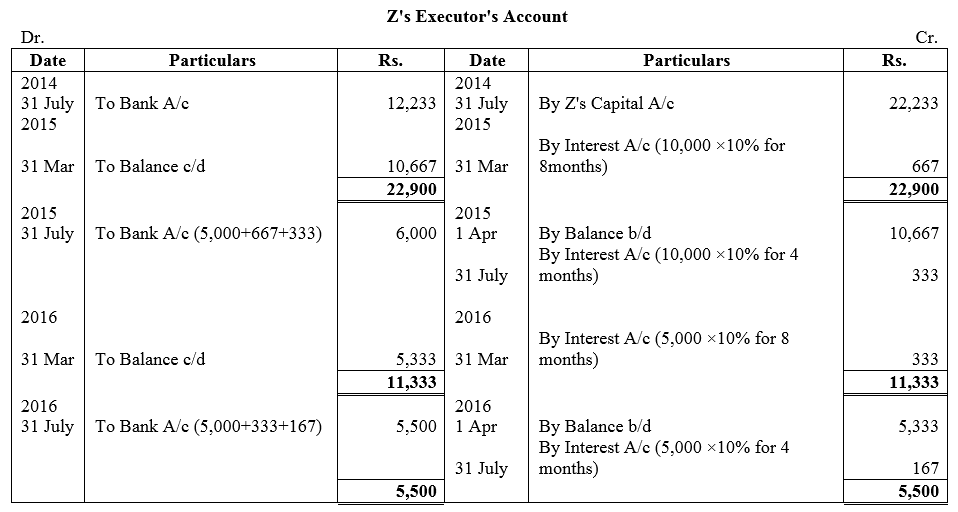

The Balance Sheet of X, Y and Z as at 31st March, 2018 was:

The profit-sharing ratio was 3 : 2 : 1. Z died on 31st July, 2018. The Partnership Deed provides that:

(a) Goodwill is to be calculated on the basis of three years purchase of the five years average profit. The profits were : 2017-18: ₹ 24,000; 2016-15: ₹ 20,000; 2014-15: ₹ 10,000 and 2013-14: ₹ 5,000.

(b) The deceased partner to be given share of profits till the date of death on the basis of profits for the previous year.

(c) The Assets have been revalued as: Stock – ₹ 10,000; Debtors – ₹ 15,000; Furniture – ₹ 1,500; Plant and Machinery – ₹ 5,000; Building – ₹ 35,000. A Bill Receivable for ₹ 600 was found worthless.

(d) A Sum of ₹ 12,233 was paid immediately to Z’s Executors and the balance to be paid in two equal annual installments together with interest @ 10% p.a. on the amount outstanding.

Give journal entries and show the Z’s Executors Account till it is finally settled.

Solution:

Question 80.

X, Y and Z were partners in a firm sharing profits and losses in the 5 : 4 : 3. Their Balance Sheet on 31st March, 2018 was as follows:

X died on 1st October, 2018 and Y and Z decide to share future profits in the ratio of 7 : 5. It was agreed between his executors and the remaining partners that:

(i) Goodwill of the firm be valued at 2\(\frac { 1 }{ 2 }\) years purchase of average of four completed years profit which were:

(ii) X’s share of profit from the closure of last accounting year till date of death be calculated on the basis of last years profit.

(iii) Building undervalued by ₹ 2,00,000; Machinery overvalued by ₹ 1,50,000 and Furniture overvalued by ₹ 46,000.

(iv) A provision of 5% be created on Debtors for Doubtful Debts.

(v) Interest on Capital be provided at 10% p.a.

(vi) Half of the net amount payable to X’s executor was paid immediately and the balance was transferred to his loan account which was to be paid later.

Prepare Revaluation Account, X’s Capital Account and X’s Executors Account as on 1st October, 2018.

Solution:

Question 81.

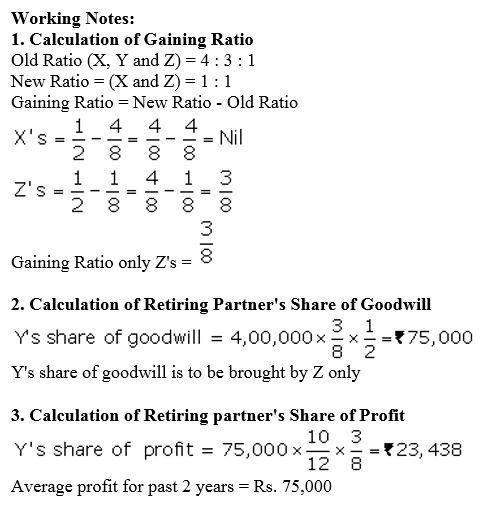

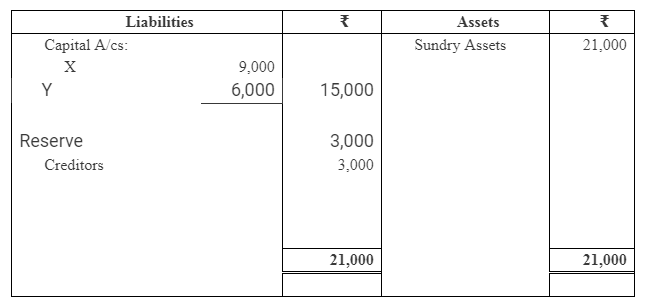

X, Y and Z were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Z died on 30th June, 2018. The Balance Sheet of the firm as at that 31st March, 2018 is as follows:

The following decisions were taken by the remaining partners:

(a) A Provision for Doubtful Debts is to be raised at 5% on Debtors.

(b) While Machinery to be decreased by 10%, Furniture and Stock are to be appreciated by 5% and 10% respectively.

(c) Advertising Expenses ₹ 4,200 are to be carried forward to the next accounting year and therefore, it is to be adjusted through the Revaluation Account.

(d) Goodwill of the firm is valued at ₹ 60,000.

(e) X and Y are to share profits and losses equally in future.

(f) Profit for the year ended 31st March, 2018 was ₹ 16,000 and Z’s share of profit till the date of death is to be determined on the basis of profit for the year ended 31st March, 2018.

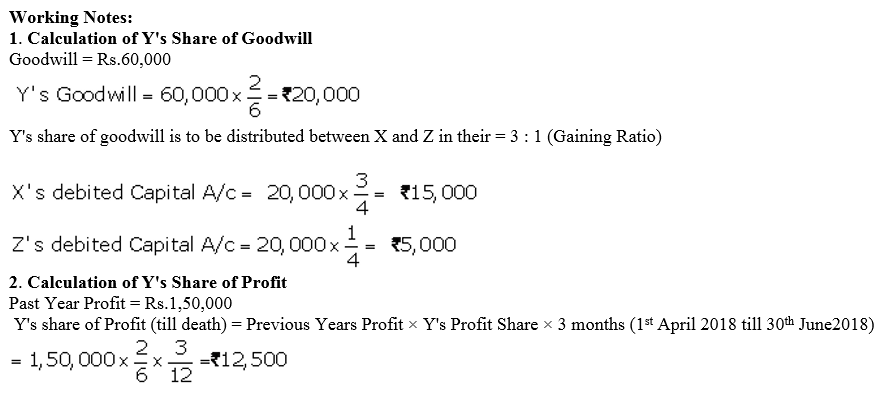

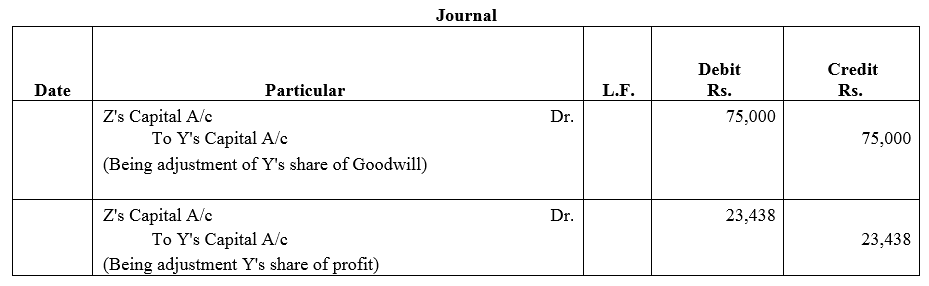

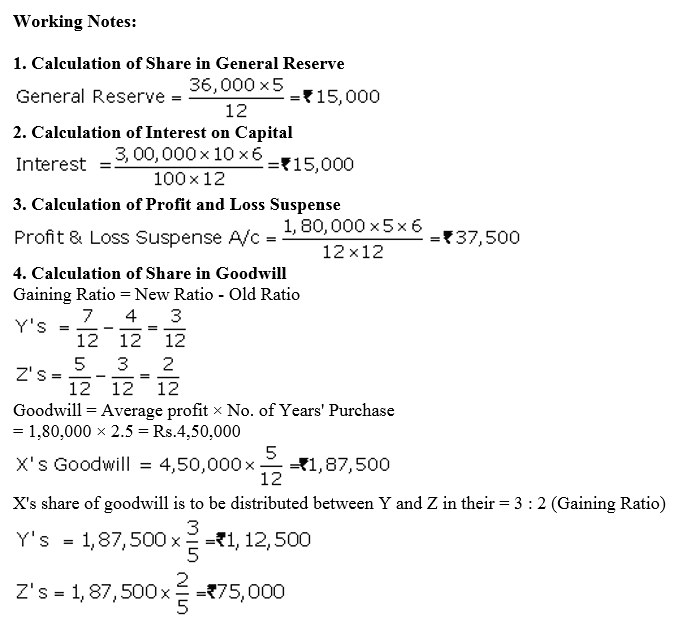

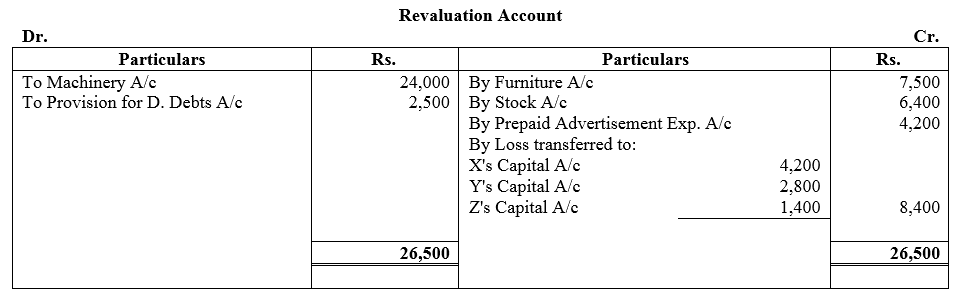

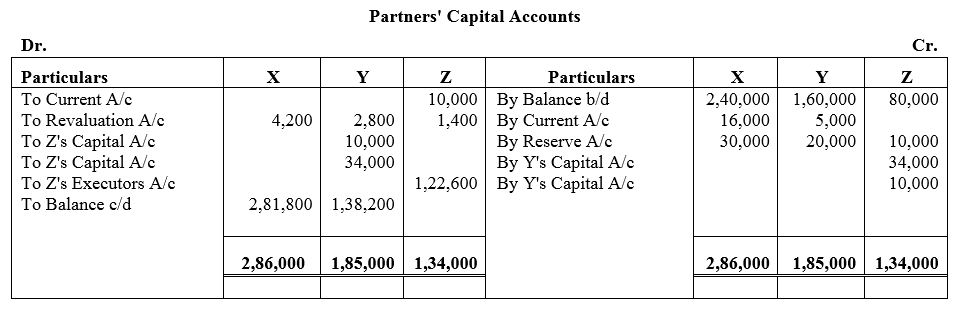

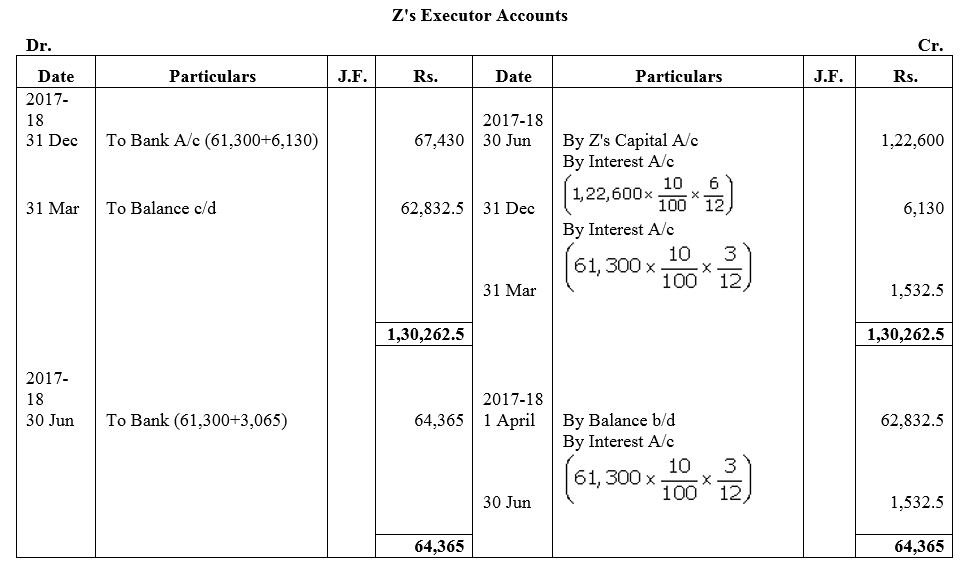

(g) The Fixed Capital Method is to be converted into the Fluctuating Capital Method by transferring the Current Account balances to the respective Partners Capital Accounts.

Prepare the Revaluation Account, Partners Capital Accounts and prepare C’s Executors’s Account to show that C’s Executors were paid in two half-yearly installments plus interest of 10% p.a. on the unpaid balance. The first installments was paid on 31st December, 2018.

Solution:

Question 82.

X, Y and Z are partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. Their Balance Sheet as at 31st March, 2018 was as follows:

Z died on 1st April, 2018, X and Y decide to share future profits and losses in ratio of 3 : 5. It was agreed that:

(i) Goodwill of the firm be valued 2\(\frac { 1 }{ 2 }\) years purchase of average of four completed years profits which were : 2014-15 – ₹ 1,00,000; 2015-16 – ₹ 80,000; 2016-17 – ₹ 82,000.

(ii) Stock undervalued by ₹ 14,000 and machinery overvalued by ₹ 13,600.

All debtors are good. A debtor whose dues of ₹ 400 were written off as bad debts paid 50% in full settlement.

Out of the amount of insurance premium which was debited entirely to Profit and Loss Account ₹ 2,200 be carried forward as an unexpired insurance premium.

₹ 1,000 included in Sundry Creditors is not likely to arise.

A claim of ₹ 1,000 on account of Workmen Compensation to be provided for.

(iii) Investment be sold for ₹ 8,200 and a sum of ₹ 11,200 be paid to execution of Z immediately. The balance to be paid in four equal half-yearly installments together with interest @ 8% p.a. at half year rest.

Show Reavaluation Account, Capital Accounts of Partners and the Balance Sheet of the new firm.

Solution:

Question 83.

X, Y and Z were partners in a firm sharing profits in the ratio of 2 : 2 : 1. On 31st March, 2018 their Balance Sheet was as follows:

Y died on 30th June, 2018. The Partnership Deed provided for the following on the death of a partner:

(i) Goodwill of the business was to be calculated on the basis of 2 times the average profit of the past 5 years. The profits for the years ended 31st March, 2018, 31st March, 2017, 31st March, 2016, 31st March, 2015 and 31st March, 2014 were ₹ 3,20,000 (Loss) ; ₹ 1,00,000; ₹ 1,60,000; ₹ 2,20,000 and ₹ 4,40,000 respectively.

(ii) Y’s share of profit or loss from 1st April, 2018 till his death was to be calculated on the basis of the profit or loss for the year ended 31st March, 2018.

You are required to calculate the following:

(a) Goodwill of the firm and Y’s share of goodwill at the time of his death.

(b) Y’s share in the profit or loss of the firm till the date of his death.

(c) Prepare Y’s Capital Account at the time of his death to be presented to his executors.

Solution:

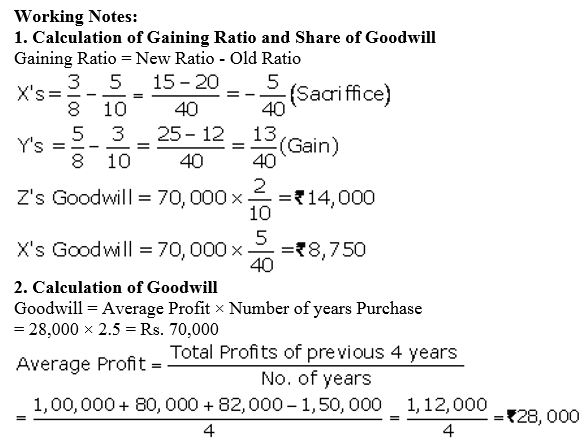

We hope the TS Grewal Accountancy Class 12 Solutions Chapter 5 Retirement/ Death of a Partner help you. If you have any query regarding TS Grewal Accountancy Class 12 Solutions Chapter 5 Retirement/ Death of a Partner, drop a comment below and we will get back to you at the earliest.